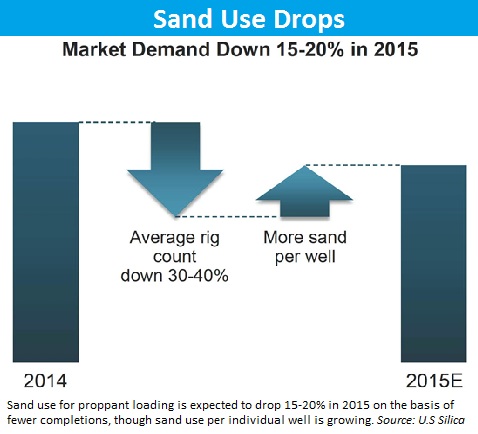

Although sand use per well is up sequentially, total industry sand use is down 40% to 50% in regional markets, reflecting the current decline in the volume of well completions.

Service providers expect demand for sand, which has become an integral component in high intensity completions, to stabilize by mid-year and remain flat for the balance of 2015, according to participants in Hart Energy’s Heard in the Field market intelligence series.

One reason for stabilization in sand use is that operators appear to be settling on standardized completion designs in the current low price environment with fewer tweaks to downhole technique. Over the last two years operators have steadily increased the volume of proppant per lateral foot.

This has led to uplifts in production in areas such as Delaware Basin in Texas and New Mexico, the Eagle Ford Shale, and the Cana Woodford/Scoop area of the Midcontinent. Similarly, the advent of high volume slickwater fracks in the Bakken has altered completion techniques and increased demand for bulk commodity sand on a per well basis.

In isolated situations, operators are pumping up to 15 million pounds of sand down a single extended lateral, or the equivalent of a 100-car trainload of sand.

However the steep drop in drilling, which is down 50% from peak as of press time, has produced a corresponding drop in well completion activity creating a dichotomy where sand use per well is up 40%, but total sand demand is down overall across the industry.

Pricing for bulk commodity sand is following suit, with declines ranging from 20% to 30% in some areas up to 50% in other areas, depending on local market conditions.

In the Bakken, the delivered price of sand to location was 12 to 14 cents per pound at peak in 2014. Pricing for sand was as low as 6 cents per pound at the end of the first quarter 2015.

Ceramics, which had occupied a niche market in the Bakken, have not yet witnessed price discounts in a lower demand proppant market and are seeing market share erode. Previously ceramics were twice the cost of sand although operators were willing to use ceramics because of demonstrated performance improvements in well yield over time. In the current market ceramics are now five to six times the cost of bulk commodity sand and are rapidly losing consideration in well completion as operators emphasize strategies that boost net present value and drilling payout and forego strategies that expand estimated ultimate recoveries (EUR).

Ceramics, which had occupied a niche market in the Bakken, have not yet witnessed price discounts in a lower demand proppant market and are seeing market share erode. Previously ceramics were twice the cost of sand although operators were willing to use ceramics because of demonstrated performance improvements in well yield over time. In the current market ceramics are now five to six times the cost of bulk commodity sand and are rapidly losing consideration in well completion as operators emphasize strategies that boost net present value and drilling payout and forego strategies that expand estimated ultimate recoveries (EUR).

“When sand at location was 14 cents and ceramics were 30 cents, (per pound) we had many operators using ceramics,” a mid-tier Bakken service provider told Hart Energy. “We now have few operators willing to bear that price differential in this market.”

Service providers say pricing is near bottom, although transportation costs could decline further, bringing incremental decrease beyond current pricing levels.

The backlogs in rail, trucking and mining that plagued the sand market one year ago have now evaporated in the current depressed drilling and completions market. There are currently no obstacles or bottlenecks preventing the timely delivery of sand supplies and service providers said the supply of sand is currently in excess of demand.

“Even with the winter issues that often cause backlogs and delays, 2015 has had few logistic issues because demand is down so low,” a Bakken area service provider said in regards to sand market.

Similarly, a Midcontinent service provider noted the potential for further price reductions.

“We have sand costs down 40% to 50% from 2015, but trucking is still high,” the mid-tier service provider said. “We are aggressively working on finding truckers who will help lower the lost of trucking and get the price down a little further.”

Contact the author, Richard Mason, at rmason@hartenergy.com.

Recommended Reading

Renewed US Sanctions to Complicate Venezuelan Oil Sales, Not Stop Them

2024-04-19 - Venezuela’s oil exports to world markets will not stop, despite reimposed sanctions by Washington, and will likely continue to flow with the help of Iran—as well as China and Russia.

US Interior Department Releases Offshore Wind Lease Schedule

2024-04-24 - The U.S. Interior Department’s schedule includes up to a dozen lease sales through 2028 for offshore wind, compared to three for oil and gas lease sales through 2029.

Guyana’s Stabroek Boosts Production as Chevron Watches, Waits

2024-04-25 - Chevron Corp.’s planned $53 billion acquisition of Hess Corp. could potentially close in 2025, but in the meantime, the California-based energy giant is in a “read only” mode as an Exxon Mobil-led consortium boosts Guyana production.

Everywhere All at Once: Woodside CEO Touts Current Global Portfolio

2024-03-05 - Meg O’Neill, the CEO of Australian energy giant Woodside Energy, is overseeing the “next wave” of growth projects around the globe, including developments in the Gulf of Mexico, offshore Senegal and further LNG expansion.

New BOEM Regulations Raise Industry Decommissioning Obligations by $6.9B

2024-04-15 - Under new regulations, the Bureau of Ocean Energy Management estimates the oil and gas industry will be required to provide an additional $6.9 billion in new financial assurances to cover industry decommissioning costs.