While onshore activity is set to decline due to the weakness in oil prices, it looks as though the pace of deceleration may slow down in the coming months, according to Rystad Energy experts. (Source: Shutterstock.com)

While onshore activity is set to decline due to the weakness in oil prices, it looks as though the pace of deceleration may slow down in the coming months, according to Rystad Energy experts.

Due to current market conditions and the recent drop in rig and frac fleet counts, horizontal drilling is set to decline by 2%, while completions increase by 3% year-over-year in 2023.

Spot market service prices are expected to fall across all U.S. basins. Due to the decline in activity last quarter, rig rates for 1,500 horsepower AC rigs have fallen. Current spot rig rates for 1,500 horsepower AC range between $27,000 per day and $30,000 per day. Rig counts across the country are down by 35 from June, 67 from the second quarter and by more than 90 since the beginning of 2023. Additionally, over the course of second quarter 2023, active frac fleets dropped from 282 to 265 in those three months.

In order to improve oil and gas supply in the face of this depleting market, some service companies have moved their rigs and equipment from gas to more liquid-rich basins. This move has improved supply and impacted prices in those liquid-rich basins. Deactivation occurred across various companies, with gas basins being the most heavily impacted. The weakness in the market has caused frac prices to be adjusted downward.

As a result, E&P companies are targeting single digit production growth to earn healthy margins, conserve cash and ultimately boost shareholder returns. Capex increases for 2023 are being driven by cost expansions from contracts locked in during the final quarter of 2022, rather than production growth. U.S. capex is expected to grow by 10% in 2023, according to Rystad Energy, with well costs beginning to decline from third quarter onward.

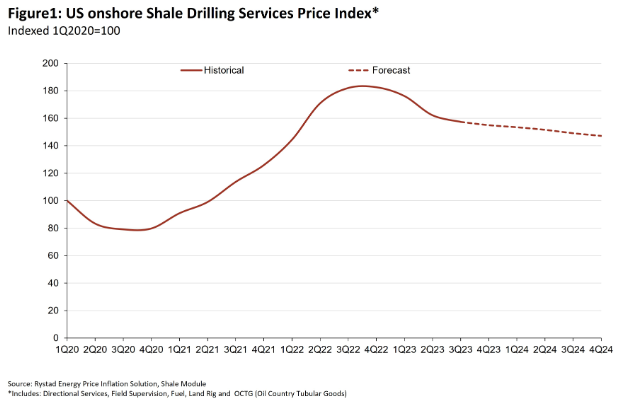

Rystad also predicts drilling service prices will fall across all U.S. basins, with an average decline of more than 10% from fourth quarter 2022 levels. Drilling rig rates peaked in January at around $35,000 per day, but has since come down to less than $30,000 per day. Prices for pipes, casings and other oil country tubular goods dropped by over 17% since January, with further declines expected. Among other declining rates are the directional drilling rates, with service companies searching for new homes for their crew. Diesel prices in the U.S. are also down from their second quarter 2022 peak, but prices are expected to rebound as the summer driving season progresses.

Overall, market supply and demand fundamentals still look strong, but prospects of a global economic slowdown are weighing on prices. The slowdown has put steady pressure on Nymex WTI futures, further dampening the activity outlook. Rystad Energy expects an uptick in activity in the fourth quarter 2023 as service costs become more attractive for operators and energy prices stabilize due to tightening supply.

Recommended Reading

SM Energy Targets Prolific Dean in New Northern Midland Play

2024-05-08 - KeyBanc Capital Markets reports SM Energy’s wells “measure up well to anything being drilled in the Midland Basin by anybody today.”

Vår Selling Norne Assets to DNO

2024-05-08 - In exchange for Vår’s producing assets in the Norwegian Sea, DNO is paying $51 million and transferring to Vår its 22.6% interest in the Ringhorne East unit in the North Sea.

Crescent Energy: Bigger Uinta Frac Now Making 60% More Boe

2024-05-08 - Crescent Energy also reported companywide growth in D&C speeds, while well costs have declined 10%.

SLB OneSubsea JV to Kickstart North Sea Development

2024-05-07 - SLB OneSubsea, a joint venture including SLB and Subsea7, have been awarded a contract by OKEA that will develop the Bestla Project offshore Norway.

Chevron, Total’s Anchor Up and (Almost) Running

2024-05-07 - During the Offshore Technology Conference 2024, project managers for Chevron’s Anchor Deepwater Project discussed the progress the project has made on its journey to reach first oil by mid-2024.