[Editor's note: A version of this story appears in the September 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Both companies faced financial challenges.

Eclipse Resources Corp., a Wall Street star when it IPOed in 2014, made headlines with its successful drilling of super laterals in the Utica Shale, exceeding 19,000 feet last year. Yet it struggled from a persistent depressed share price—having fallen by 94% in the four years after going public—as public markets abandoned the oil and gas space, and particularly gassy names. As the stock continued to plunge, earlier this year the New York Stock Exchange put the company on notice of delisting.

Blue Ridge Mountain Resources Inc. was the resurrection of Magnum Hunter Resources Corp., another Marcellus/Utica operator that emerged from bankruptcy in January 2017 with new management and a new name. John Reinhart, coming out of Appalachian start-up Ascent Resources, took over the CEO role. During the next two years he would sell off Bakken assets and others to core up as a Utica and Marcellus pure player and further knock down debt.

The two companies found their match where their acreage touched in Ohio. Eclipse and Blue Ridge closed their combination in February, forming Montage Resources Corp. The majority of the surviving management team came from Blue Ridge, with Reinhart as CEO. Making the integration easier, five out of six of Montage’s new management team worked together previously at Chesapeake Energy Corp. in its Appalachia division.

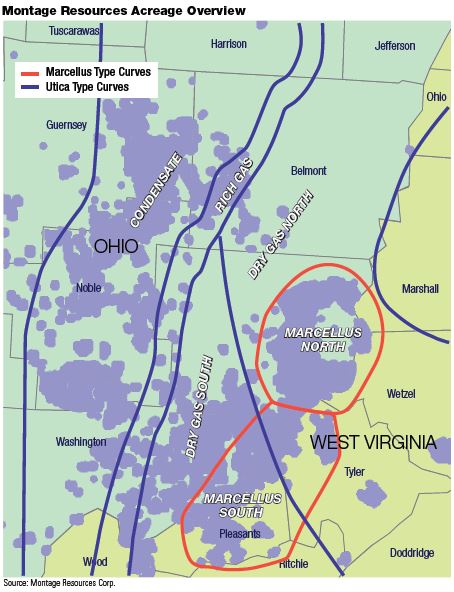

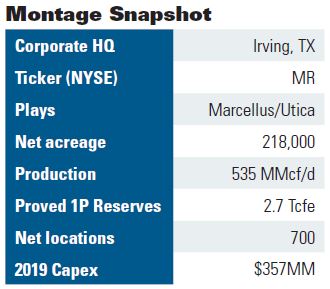

Montage now holds some 220,000 net acres prospective for the Utica and Marcellus shales in Ohio, West Virginia and north-central Pennsylvania with production of approximately 535 million cubic feet per day. Its new mission: balance cash-flow generation with consistent growth while focused on efficiencies. While perceived by many as a natural gas-focused company, some 40% of Montage’s revenues are derived from liquids production. Notably, its blended debt-to-EBITDA is 1.7 times, well below its peer group average of 2.1 times, giving it ample margin on the balance sheet.

Reinhart, a mechanical engineer from West Virginia University, began his career at Schlumberger Ltd., and worked as vice president of operations for Chesapeake’s East Division, COO for Ascent Resources LLC and CEO of Blue Ridge Mountain Resources before assuming leadership of Montage. He was also a sergeant in the Army, serving in Operation Just Cause in Panama and Operation Desert Storm in Iraq. Oil and Gas Investor spoke with him regarding his plans for Montage.

Investor: What motivated the merger with Eclipse?

Reinhart: Our two companies sat side by side, so our acreage position was very contiguous. Production in the basin has grown over the past 10 years, and we saw a lot of synergies between the companies from the asset perspective, but also with the team; a lot of us had worked together in prior lives.

And knowing that scale does matter. That motivated both of us. Ben [Hulburt, former Eclipse CEO] and I just started having a conversation and said, “Hey, these two companies are pretty good companies. We have great staff and great assets. Let’s see if we can do something a little special here.”

Investor: What is the Focus Five strategy?

Reinhart: It’s having disciplined growth and protecting the balance sheet. It’s making sure that your hedge portfolio protects the downside on the cash. It’s making sure that you’re not overcommitted on any kind of volume commitments or long haul pipe. It’s making sure that you can toggle between gas and condensate and maximize profitability.

In this low commodity cycle, we’re all very sensitive to generating cash flow and keeping the business healthy. We have all come from a history of various companies that had some levels of distress and are very sensitive on making sure that we keep the company healthy with plenty of liquidity and a good leverage ratio. If that means growing 5% instead of 15%, that’s what you do to protect that balance sheet. And when we come out of this cycle, we want to be strategically placed to have a lot of options that may be attractive inorganically for the company.

Investor: Even following the merger, Montage is still a small-cap company, and public market investors have indicated they prefer larger-scale companies. Why do you then prioritize free-cash-flow neutrality over a more aggressive production growth model?

Reinhart: We understand we have to grow. Growth is extremely important to us now. We’re growing this year at 23%, so that’s a pretty chunky growth profile as we continue to navigate these low commodity cycles. We have the ability to drill some wells right now in very high-quality rock very efficiently.

But it’s not so much a focus on free cash flow, so to speak. It’s more about a focus on keeping a prudent balance sheet and a healthy company. That means being mindful of your cash inflows and outflows. So whether that growth is 5%, 10% or 20%, we are going to be mindful to toggle that level of growth to be sure that we protect the company and keep it healthy. No one can predict commodity prices.

I personally believe that as we navigate the next few years, the landscape is going to look a lot different in Appalachia. There are companies that won’t be here, and a lot of private companies are looking for an exit. So keeping the company in a healthy position while effecting growth we feel puts us in a much better position as we navigate this environment right now to come out of this with some opportunities that perhaps some other people may not have because of their leverage or commitments that they’re saddled with. If you start stressing the balance sheet, your options to do things strategically, whenever it does recover, are very hamstrung.

Investor: Are additional mergers or acquisitions part of your growth strategy?

Reinhart: We’re very focused on the fundamentals of the business and growth through the drillbit. Having said that, I think it’s not a stretch to see a company of our size with a clean balance sheet, liquidity and attractive leverage ratios, if an opportunity comes up, to look at how that impacts the company. To the point that those materialize and are accretive I would say—absolutely—we’re going to take a strong look at that. We stay plugged in and we are very open to accretive opportunities to grow scale at a much more accelerated pace.

Investor: Natural gas and NGL prices have swooned since the merger. How are you adapting to weaker commodity prices this year?

Reinhart: It’s a wonderful thing to have half your assets in areas very high in condensate with NGL exposure as well as natural gas. For us it’s about what the commodity prices are allowing us for growth from a cash flow perspective. We look at it as more of an allocation, and you can do that if you don’t have a lot of commitments driving your business. We don’t have a lot of HBP issues, or MVCs [minimum volume commitments] or FTs [firm transportation agreements]. We sell in basin at a premium to people who are long on unutilized firm transportation.

One of the big benefits of the merger is our combined asset base contains about a 50% mix of condensate and a 50% mix of dry gas, so that was very attractive. The combined asset base of the company is 70% to 75% held long term, either HBP or long-term leases, which gives us some flexibility. It allows us to make decisions based on true economics.

Is gas in the Utica attractive right now? Yes. You’re talking 40% returns. Is condensate more returns driven? Yes. The Marcellus in Ohio, that’s certainly where we focus a third of our capital this year—that provides even better returns. We manage commodities by looking at the strip, we look at the cash flow outputs, and we just toggle between the Marcellus and Utica dry gas and condensate windows. And that’s what we go drill.

Investor: What is your primary goal in your operational plan this year?

Reinhart: We’re focused on cycle time improvements, removing dead time in the operation.

From an Eclipse standpoint, last year vs. this year, we’ve reduced our cycle times by over 30% year-over-year. That gets us down into that 150-day spread between spending capital and turning revenue. That means you can turn your cash faster, you can grow and be more prudent and get to cash flow neutral, cash flow positive, at a much quicker pace than what you would do if you were to stretch those cycle times out.

We mobilize rigs on a 24-hour basis now versus 12. We’ve been very pleased with our Marcellus cycle times on the drilling side. We just finished a pad where we averaged nine days a well on a three- to four-well Marcellus pad last month.

Why is that important? If you can shave down two or three days per hole and you can skid over a rig on a pad in about eight to 10 hours, those days add up and you’re adding wells toward the end of the year that you would normally otherwise not have.

Every day you shave off a drilling rig is $100,000 to $125,000 a day. Every day you shave off on your frack cycle times is $40,000 a day you save. So we work pretty hard at taking advantage of being active when some operators aren’t as active.

On the pricing side, which is cyclical in nature, right now we’re looking at utilizing our activity that we have planned to lock in prices over the next 12 months and take advantage of this very attractive environment from a service capacity side. We’ve been able to do that on the completion side and on the drilling side and we’ll continue to push.

Investor: Pre-merger, Eclipse made news in the past two years for its super-extended laterals. Why have you decided to decrease average lateral lengths?

Reinhart: This strategy is formed around a return on capital. We want to make sure that, from a financial standpoint, it accretes value to the company. That may sound pretty common sense, but that’s not always what you find with some of these bigger companies.

This team historically had drilled super-long laterals, which were technological accomplishments. But we’re now focusing that execution prowess on being more efficient and reducing cycle times, increasing cash turns and making more money. So the lateral lengths were a pretty big shift.

We shifted from drilling 14,000- to 20,000-foot laterals down to 10,000- to 12,000-foot lateral lengths, which by the way are still some of the longest laterals. Practically, that dramatically reduces your cycle time of drilling, completion and turning these wells online.

If you drill five 20,000-foot laterals, that’s probably $85- to $95 million you’re floating. Your cycle time on that is going to be almost a year. I would rather drill three to four 12,000-foot laterals, spend half the money and make my cycle time about 150 to 160 days. You can imagine what that does to a small company’s cash turns and balance sheet. It changes the production profile, changes your cash-flow profile, and you’re getting revenues sooner.

Also, as you get back into this 10,000- to 12,000-foot lateral range, it really de-risks the development plan’s operational exposure. The longer you go out, there’s always more exposure to wellbore instability, potential issues and capital overruns. The shorter laterals also minimize your production and reserve concentrations in one lateral, which is very beneficial looking at the long-term outlook and having assurance of a low-risk production profile.

Investor: Does shortening the lateral impact the productivity or the results of the well?

Reinhart: It certainly doesn’t impact it negatively. Eclipse had historically looked at a metric of dollars per foot of lateral. They took the approach that these longer laterals minimized their cost per foot. Naturally, if you drill a longer lateral, you spend more money and you want more production out of that to make a decent return. Eclipse was aggressively opening up their production on these long laterals.

We produce the wells similar to other established operators, with restricted choke practices for pressure drawdown management. Generally speaking, our Utica dry gas wells are choked back at a 22- to 26 million cubic feet a day range. These prolific wells will produce at those rates for eight to 15 months depending on the lateral lengths. Almost without exception, in many plays where the choke is restricted, it actually improves the overall EUR. And it certainly de-risks any potential damage and productivity as well.

However, if you followed that pressure management choke on a 20,000-foot lateral, your returns would be substantially hindered because of the slower claw back of the increased sunk capital.

Investor: How do you think about your development plan going forward?

Reinhart: That’s another big part of the strategy shift. These pads were built for stacked pay and for six to 12 to sometimes 14 wells per pad. But we didn’t want to drill out six or seven wells per pad, initially.

By taking an approach where we now initially drill three to four wells on the pad, that shrinks cycle times significantly from the point where you’re spending cash and making money. We mobilize and we go drill the next and we go drill the next. At some point in the future we’re constructing these pads whereby we don’t have to shut in those volumes, so we actually come back at a later date and we can continue to drill.

Investor: Are you concerned about parent-child well issues?

Reinhart: We really want to stay out of the parent-child relationships and issues that some of these companies are seeing by not executing on a more full development plan.

Think about a pad, you have let’s say three southeast wells and three northwest wells. We like to drill out the southeast wells so you don’t get into any kind of development issues in the future, then move onto the next pad and drill out the southeast wells. At some point you come back and drill your northwest wells. This way you don’t have downtime and you don’t have parent-child issues. You fully develop your offset wells as you move.

We do these in tranches where we mow down the southeast wells and then come back and do the northwest wells. It’s not exposing us to parent-child issues where we’re drilling offset laterals in a row, and we’re constructing these pads whereby we don’t have to shut in those volumes in the future.

But the important part is our return on capital is dramatically improved because we’re spending money and collecting revenue in a much shorter cycle time, which moves the needle for return on capital.

Investor: Why did you drop one of your two rigs this summer?

Reinhart: We were looking at a growth rate of 23%, and we continue to outperform production expectations. Do we want to take a more cautious approach with regards to spending $30 million more in drilling right now? Commodities are low. We don’t need the extra growth right now. Let’s have the option at the end of the year to pick up based on what commodity prices are doing in Q4.

Investor: Where will your drilling plan and capex be focused on through year-end and into 2020?

Reinhart: We shifted drilling into core areas. Because of how the commodity prices have moved over the year we’ve shifted toward more condensate development. About 50% of our development this year is in the condensate window of the Marcellus and Utica, which has preferential returns right now vs. the dry gas area. Think half liquids, half gas for probably at least the first three quarters of 2020.

Investor: Blue Ridge Mountain had its challenges at that time you took the CEO role, having just come out of bankruptcy. And it was your first turn at CEO. What did you see in the opportunity in that moment?

Reinhart: You know, I’m an old Army guy, and where there’s chaos and a lot of noise, I generally run to that where most people probably shy away from it. Where there’s distress, I fundamentally do believe there’s opportunity. So when I looked at this opportunity, I saw a company that had really good Marcellus and Utica assets, but they did not have the execution, the staff, the liquidity, the corporate structure or the strategy to be able to exploit some of the high-quality assets that they owned.

So the assets brought me here. Also, I was ready to take on a leadership role of a company. But let there be no mistake: There was a lot of work to do to sell off noncore businesses, to get the strategy very focused, to staff with people who had the experience and the operational prowess.

Investor: You spent a lot of years at Chesapeake and started up its Appalachia division. As Chesapeake discovered the Utica Shale, did you discover the Utica as part of that divisional start-up?

Reinhart: A guy named Matt Weinreich, a young geologist for Chesapeake, is the guy who pitched it to Aubrey [McClendon, Chesapeake CEO at the time]. I was in the room. There were a lot of Knox penetrations up there, and they always had gas shows from this pesky zone called the Utica. And I remember in the meeting, we said, “Well let’s go drill one.” And we drilled the Buell well in Harrison County, and that was an outstanding well. It changed the tide of what we were doing.

It was pretty fascinating to watch a play be discovered and then subsequently go out and drill it. I don’t know how many people get to see that in their career, but it was pretty amazing to be a part of it.

Investor: What is your vision for Montage over the next five years?

Reinhart: It’s just to grow a prudent, attractive, value-driven company and continue to grow it as the market dictates, while also being mindful that there are going to be some inorganic opportunities. And the companies that keep a healthy balance sheet are going to be the ones that can have a pretty good shot at transacting on something.

Investor: What is your most memorable experience while serving in the Army, and what did you learn from it?

Reinhart: It was Dec. 19, 1989. I was on my second deployment to Panama. That particular date was my birthday and when the actual Panama invasion happened. I was part of that.

We were at a joint Panamanian/U.S. Army base and there were Special Forces from the Panamanian division on that base. We were tasked to secure the front gate and to stop the supporting troops from exiting as the invasion started. We got into a firefight as troops were trying to leave and we ran out of ammunition—we weren’t fully geared up because we didn’t want to tip them off.

We had secured two Panamanian gate guards with cuffs, and they got caught in the crossfire. In the middle of the firefight, as we ran out of ammo, my buddy and I pulled those guys back under cover. I was awarded an Army Commendation Medal with “V” device for valor in combat. It’s the lowest valor in combat medal awarded, but I was extremely proud of it.

What I learned from it is I don’t like bullets flying at me. And I learned that there’s probably another career option for me down the road vs. doing that.

Recommended Reading

TGS, SLB to Conduct Engagement Phase 5 in GoM

2024-02-05 - TGS and SLB’s seventh program within the joint venture involves the acquisition of 157 Outer Continental Shelf blocks.

2023-2025 Subsea Tieback Round-Up

2024-02-06 - Here's a look at subsea tieback projects across the globe. The first in a two-part series, this report highlights some of the subsea tiebacks scheduled to be online by 2025.

StimStixx, Hunting Titan Partner on Well Perforation, Acidizing

2024-02-07 - The strategic partnership between StimStixx Technologies and Hunting Titan will increase well treatments and reduce costs, the companies said.

Tech Trends: QYSEA’s Artificially Intelligent Underwater Additions

2024-02-13 - Using their AI underwater image filtering algorithm, the QYSEA AI Diver Tracking allows the FIFISH ROV to identify a diver's movements and conducts real-time automatic analysis.

Subsea Tieback Round-Up, 2026 and Beyond

2024-02-13 - The second in a two-part series, this report on subsea tiebacks looks at some of the projects around the world scheduled to come online in 2026 or later.