Patterson-UTI President and CEO Andy Hendricks and NexTier Oilfield Solutions CEO Robert Drummond discussed the companies’ planned $5.4 billion merger in a Hart Energy exclusive interview. (Source: Hart Energy)

On June 15, Patterson-UTI Energy and NexTier Oilfield Solutions agreed to a combination that will create the largest U.S. shale drilling and completions pure-play company in the energy sector.

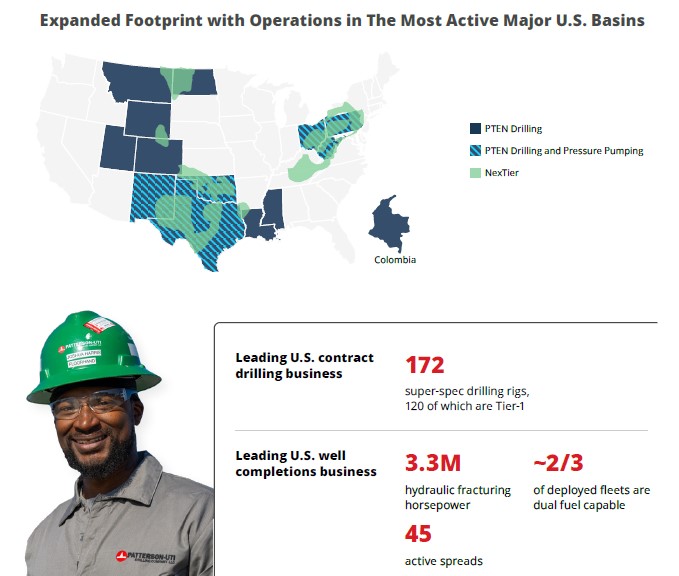

The deal, an all-stock merger of near-equals, will result in a new Patterson-UTI with a combined value of $5.4 billion and operations in the Lower 48’s most active shale basins. Patterson-UTI shareholders will own a 55% stake in the expanded company.

The combined company will have a fleet of 172 super-spec drilling rigs, 45 active frac fleets (33 NexTier, 12 Patterson-UTI) and directional drilling services.

Patterson-UTI President and CEO Andy Hendricks, who will remain CEO, and NexTier CEO Robert Drummond, who will become vice chair, joined Hart Energy for an exclusive discussion delving into how deal talks started, their rationale behind the merger and the steps ahead to integrate the company.

Hart Energy: Could you give us some background on looking for a combination or strategic alternative and some of the driving factors behind this merger?

Robert Drummond: We had a unique opportunity to name the company when we merged [Keane Group] and [C&J Energy Services]. We went into a pretty detailed process, very difficult, and finally realized a great name would be NexTier—because we’re going to be constantly looking to take the company to the next tier.

So our employees have been accustomed to us doing M&A. We’ve been engaged with advisers for a long time. And with a very healthy balance sheet, we were always able to be a potential second party for a lot of different transactions.

Over the last couple of years, we’ve always looked at Patterson as being a company with a similar culture, a similar mindset about how to invest capital and how to deploy technology, and focused on execution.

[Andy Hendricks] and I talked about it loosely for over a year but never really engaged completely. We felt like, having been in M&A a lot, you can do a small deal and bolt it on, or you can do something that’s transformational like this one.

Being able to choose a partner that was such a good fit with strong leadership, we felt comfortable that we would be a lot stronger together than we would be separately. So really it was a pretty easy decision for me.

Our board was quick to say the same thing, our advisors were able to put it together and show us that it was a very good deal for our shareholders. I’m just really happy that we were able to bring it together.

Andy Hendricks: Like Robert said, we talked off and on for a while—not seriously, but to discuss, ‘What’s the potential? Could it work? Could it fit?’

For us, it wasn’t quite the right time. We were in the process of ramping up activity real quick. Our own team was kind of reorganizing on the pressure pumping side to improve what they were doing. We had to have the right time for us as a company, and it really had nothing to do with the market timing.

Some people are seeing this as, ‘Oh, well the market’s kind of soft so two companies are getting together.” We’d be doing this right now if the market was ramping up. It was really more about where we were in our journey, where they were in their journey, and when was the right time to put the two companies together.

HE: I was curious if you can elaborate much on just how challenging it was to come up with the 55/45 split?

AH: The 55/45 was really based on the companies’ market caps, and so that was kind of straightforward math there. It was really more of a discussion, okay, what is the governance look like? What is management going to look like going forward? And trying to find some balance in the system on a merger of equals. That’s where we had a lot of discussions.

Then, is this really going to be beneficial for shareholders? At the end of the day, we decided it is. I mean you look at how the combination of the two companies — with the synergies and all the free cash flow — we're going to be one of the highest free cash flow yielding companies in all of oilfield services.

RD: A lot of our investors had been telling us that our market cap was almost a little bit too small to be able to get the size investment they wanted to put in the company. This is the biggest pure-play shale play company.

If you’re going to make an investment in shale, the combined $5.5 billion enterprise value company is twice as big as anything else out there that gives investors the opportunity to take a large position in [the company]. That was also a driver for our board.

HE: In that vein, what’s most important? Is it building that overall scale or is it also balancing out the drilling and completion strengths?

AH: Drilling, there’s a few things. We have a strong franchise, 45-year-old franchise in drilling. NexTier’s built a really good franchise in pressure pumping. Our Universal name dates back to 1980. So putting our completions and their completions together is going to be a powerful force.

We’ve had to manage ours a little different because we have multiple segments. Where they were really focused on well completions. They built out wire line, they built out power systems, they built out logistics to support all this.

You take our 12 active spreads and then you layer in everything that they’ve done on the well completion side, and that only enhances what our 12 active spreads do.

RD: Patterson-UTI had built a strong digital operating system, not unlike our NexHub [Digital Center]. Our NexHub has been focused on completions and all the logistics around completions. And of course Andy's is focused on mostly on the drilling side.

And I think there's a lot of synergies that we're yet to realize there what the potential really can be. So I'd say technology has got a big play here that will materialize over time.

HE: Are you expecting more services consolidation? Do you see a wave potentially happening? If so, would PTEN look to continue to be a consolidator?

AH: Well, I'm not sure if we see a wave. I mean, Robert and I have been talking off and on for over a year. So this is not like we woke up and said ‘let’s put the companies together. ‘

That’s how a lot of these things happen. When we did the deal and acquired Seventy Seven Energy [in 2017], that was over a few years as well. So these things don't happen right away, and I don't think it necessarily triggers a wave.

If you look at some of the other companies that are out there, I think they're going to have more challenges trying to figure out who they're going to partner with.

I'm really excited that Robert and I were able to land this the way we did and we could pick who we partner with. We didn't get forced into something. And the others, if they want to do something, it may not be their partner of choice. So I don't anticipate a wave. As to whether we do any more M&A, both of our companies have a history of M&A, so it's hard to say we're never going to do anymore, but we'll keep you posted as we continue to look at things. But right now we've just been focused on this one.

HE: How do you expect the whole integration process to go?

RD: I think that process is something that we both have good playbooks on and a very good track record of being able to deliver. Capturing some of the synergies associated with it, but also culturally bringing the two companies together so that you have the blend of the best of the talent for both. I think that when it comes to the completion side of the business, Andy described it very well. The well site integration strategy that NexTier had has been core to our performance and it's very easy to scale that around additional frack fleets.

That was what we did with the Alamo acquisition we got a couple years ago. And the same thing with the C&J-Keane merger before that.

I would also point out that one of the things that brought us together, from my perspective, was that we both had been moving towards natural gas a power source. A better economics around the fuel costs, as well as a smaller environmental footprint. And that was very attractive from a person running a frac business because the Universal fleet will be about 75% natural gas fueled at the end of the year, and ours is about the same.

HE: You beat me to my next question: I was going to ask how important emissions reductions were in this?

RD: I appreciate that question because they are important, especially when it's the right thing to do, and that the economics around it create value. With a frack fleet, you burn… as much as $50 million a year in fuel.

If you go to natural gas, you can capture an arbitrage of up to $10 [million], maybe even $15 million dollars annually per fleet in savings. So we've been reinvesting that kind of value to continue to convert diesel-powered pumps to dual-fuel pumps that allow us to do that. Then emissions just come right along with it.

So it’s a win-win, really: Customers win, we win and environment wins.

AH: Patterson-UTI for years has had a leadership position across multiple service lines, especially in drilling where we have 100% natural gas engines. We do high line power, we have the EcoCell lithium battery hybrid solution.

We’re real excited about bringing NexTier together with our completions because we've been running a lot of dual fuel and they've been running a lot of dual fuel. They’re looking at electric frac. We’ve been looking at turbine direct drive. So we’ve all been working on technologies and putting all those efforts together is going to be big across all our platforms. We have a lot of expertise.

HE: Obviously equipment can move and does, but does geography factor into this merger much at all? I know there’s a Latin American component as well.

AH: Latin America, for us, is drilling. We have the rigs in Colombia, we may end up with a rig in Ecuador. I won't say that we're going to rush to put pumping down in Latin America right now.

When you look at the geographical overlap in the U.S. that we have, there's some real opportunities to consolidate some facilities or reorganize how we do things in different basins. Maybe we concentrate pumps in one facility, blenders in another, electronics in another, things like that to be more efficient on how we do things—especially in the Permian where we’re all going to be so large.

But we’re all still busy, too. There's been a little bit of a softening in the rig market, but you look at our rig count. We're down from 132 … to 125. That's not actually a big drop for us. And pumping follows all our rigs. Even if there's a little bit of white space in the calendar on the pumping side, we're all still busy.

RD: That’s a good point. All the frac fleets are fully deployed between both companies.

HE: What were some of the considerations that made this deal make sense now versus when you first started talking about it? What has changed in the market, or more broadly for the sector?

AH: Like I said, this is not market driven but more of a where we are as companies on our journeys. I think one of the things is we both started looking at new technology. There's a big opportunity to make sure that we're not overlapping each other and spending more than we need to spend, and instead we can pull those efforts together.

RD: We believe there’s going to be a path to helping our customers make tier-two wells into tier-one wells over time. Technology has continued to do that over time. Some of the drilling things that Patterson’s doing with U-shaped wells and being able to get right up against the boundary lines or lease line to get more of a drainage of the reservoir.

This is how big data and data analytics are going to come into play over time. The two of us together, technically, it's going to be really strong. We’re going to be in the core of helping the E&Ps get to where they want to go.

AH: You’ve heard a number of E&Ps say we want to get more productivity out of wells when we drill them—a higher percentage of recoverable. Combining our efforts and what we do on engineering, not just equipment but engineering, that we look at on the subsurface, it helps put us in a leadership position to be able to help E&Ps improve their recovery.

HE: How does consolidation in the E&P space impact your outlook for the combined company?

RD: There’s a lot of different kind of players. There's big market cap guys, there's [international oil companies] even, and there's smaller independents. Some are proving up plays to be able to sell to the bigger guys. But it’s all kind of consolidating toward the end user who is going to be the one that has to go get the molecules out of the ground.

As things are consolidated towards the bigger — the guy who knows he's going to be the one developing the reservoir fully becomes more and more a technology play … using the technology to make sure you get maximum recovery from the well and the maximum return.

This plays to the strength of companies like NexTier and Patterson for the reasons we were referring to earlier. We have all different kinds of customers in our portfolio, but the big parts of it are for customers who are going to be doing the development, ultimately.

AH: When you look at some of the announcements that we’ve seen this year, a lot of them are pretty small, private equity-backed E&Ps that just drill a few wells and try to prove up their acreage. Then, that acreage gets in the hands of a larger player that wants to do a full on development, and that’s what we do.

We're not out there with SCR [silicon-controlled rectifier] rigs or mechanical rigs just doing some horizontals to prove up acreage. We're operating high spec, super spec rigs and high performing frac equipment for people doing development work.

It really plays into our strengths I think, because that acreage lands with those entities that really are doing the development, as Robert said. And if you’re following E&P, there’s always some spinoffs of property. There’s always a restart with some of these to do it again, and it just keeps happening.

HE: You all drill and complete wells almost every day and have really good insights into what’s happening on the ground. What is your outlook for the longevity of the Permian, and when is this expected plateau that we could see?

RD: I’ve got a strong opinion about this one. In fact, so strong that I got both of my daughters into the industry who are working in this arena as professionals.

I think it’s going to be for a lifetime. Tier-one’s being consumed a bit more, maybe a bit faster than they thought. It’s always tier-two moving to tier-one, and tier-three moving to tier-two. If you quit betting on technology and the capabilities, you’d be wrong every single time up until now.

So personally, as a petroleum engineer … in this thing nearly 40 years, I completely believe that we will be doing this from now on.

AH: When you look at the Permian, the Permian geologically is the gift that keeps on giving. Technology is going to continue to enhance what we do in the Permian. And when you look at the risk profiles of places to invest around the world, the Permian is still one of the best risk profiles for an E&P that looks around the world.

There’s just so many positives about the Permian, and technology will continue to influence how we get production out of there.

Yes, the IEA [International Energy Agency] is forecasting by the end of the decade that we’re going to reach a peak in oil, but it doesn't come off after that. If you actually look at the IEA’s chart, it gets to a peak and then it's flat on demand until 2050. Well that's a long time. So the world still needs oil and gas.

For the United States, the Permian is a huge geological structure that still contains a lot of oil and we're still learning how to get it out. When I started the industry, a well in the Permian produced 2.5 bbl/d, and look where we are today. Technology will keep moving that needle.

Recommended Reading

BKV CEO Chris Kalnin says ‘Forgotten’ Barnett Ripe for Refracs

2024-04-02 - The Barnett Shale is “ripe for fracs” and offers opportunities to boost natural gas production to historic levels, BKV Corp. CEO and Founder Chris Kalnin said at the DUG GAS+ Conference and Expo.

How Diversified Already Surpassed its 2030 Emissions Goals

2024-04-12 - Through Diversified Energy’s “aggressive” voluntary leak detection and repair program, the company has already hit its 2030 emission goal and is en route to 2040 targets, the company says.