Equitrans Midstream Corp. built onto its position April 10 in the Appalachian Basin, where the Pittsburgh-based company is already one of the largest natural gas gatherers in the U.S., through acquisitions totally more than $1 billion.

The acquisitions comprise of stakes in two gas gathering systems in Appalachia, Eureka Midstream Holdings LLC and Hornet Midstream Holdings LLC.

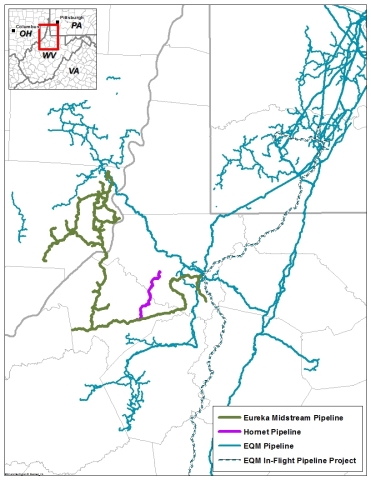

Eureka Midstream is a 190-mile gathering header pipeline system in Ohio and West Virginia that services both dry Utica and wet Marcellus production. Hornet Midstream is a 15-mile, high-pressure gathering system in West Virginia that connects to the Eureka system.

Eureka And Hornet Pipeline Assets

(Source: Business Wire)

Combined, the assets averaged about 1.6 billion cubic feet per day of gathered volume during fourth-quarter 2018 with a volume mix of 67% dry gas and 22% wet gas. The systems are supported by roughly 200,000 acres dedicated in core Marcellus and Utica.

Equitrans said its affiliate, EQM Midstream Partners LP, completed the acquisition of a 60% interest in Eureka Midstream and a 100% interest in Hornet Midstream. The transaction had originally been announced March 14.

Diana M. Charletta, COO of EQM Midstream, said the company will begin integrating the Eureka and Hornet systems into its existing assets.

Throughout the Marcellus and Utica regions of Appalachia, EQM Midstream owns about 950 miles of FERC-regulated interstate pipelines and also owns and/or operates roughly 2,405 miles of high- and low-pressure gathering lines, according to the company press release.

“We are relentless in our pursuit of becoming the low-cost provider and partner of choice across all aspects of our business,” Charletta said in a statement April 10. “These value-enhancing assets will diversify our producer customer mix and increase exposure to wet Marcellus acreage; expand our supply hub and create additional commercial opportunities; reduce unit operating costs through increased scale; and accelerate opportunities for our water services business.”

Total consideration for the acquisition of $1.03 billion, consisted of about $860 million in cash and roughly $170 million of assumed pro-rata debt.

Concurrently, EQM Midstream closed the private placement of $1.2 billion of newly issued series A perpetual convertible preferred units. A portion of the net proceeds from the private placement was allocated to the cash purchase price of the acquisition, with the remainder to be used for general purposes.

Citi and Guggenheim Securities LLC were financial advisers to Equitrans and EQM Midstream for the transaction. Latham & Watkins was the companies’ legal adviser. Citi and Guggenheim Securities also acted as joint placement agents for the convertible preferred units issuance.

The convertible preferred units were sold to lead investors consisting of funds managed by BlackRock, GSO Capital Partners and Magnetar Capital as well as supporting investors The Carlyle Group and Foundation Infrastructure Partners in connection with Neuberger Berman Private Credit.

Emily Patsy can be reached at epatsy@hartenergy.com.

Recommended Reading

Defeating the ‘Four Horsemen’ of Flow Assurance

2024-04-18 - Service companies combine processes and techniques to mitigate the impact of paraffin, asphaltenes, hydrates and scale on production—and keep the cash flowing.

Tech Trends: AI Increasing Data Center Demand for Energy

2024-04-16 - In this month’s Tech Trends, new technologies equipped with artificial intelligence take the forefront, as they assist with safety and seismic fault detection. Also, independent contractor Stena Drilling begins upgrades for their Evolution drillship.

AVEVA: Immersive Tech, Augmented Reality and What’s New in the Cloud

2024-04-15 - Rob McGreevy, AVEVA’s chief product officer, talks about technology advancements that give employees on the job training without any of the risks.

Lift-off: How AI is Boosting Field and Employee Productivity

2024-04-12 - From data extraction to well optimization, the oil and gas industry embraces AI.

AI Poised to Break Out of its Oilfield Niche

2024-04-11 - At the AI in Oil & Gas Conference in Houston, experts talked up the benefits artificial intelligence can provide to the downstream, midstream and upstream sectors, while assuring the audience humans will still run the show.