EQT Corp.’s $5.5 billion all-stock deal to buy Equitrans Midstream will try to thread the needle with investors as EQT executives make the pitch for creating the U.S.’ lowest cost natural gas producer—while adding a mountain of debt.

The initial tradeoff? EQT will sacrifice some free cash flow to pay off Equitrans’ debt of between $7.6 billion and $8 billion. EQT will also sell assets to reduce borrowings. Including equity and debt, the deal is valued at roughly $13 billion.

The deal could also face regulatory hurdles.

Investors reacted to the March 11 transaction announcement with a selloff, sending EQT shares down by 7.76% at closing.

The acquisition brings long-term synergies for EQT but also near term overhang, Gabriele Sorbara, Siebert Williams Shank managing director, said in a March 11 report.

“While there is clear industrial logic and long-term benefit from the ETRN [Equitrans] acquisition, it is a mostly dilutive transaction that significantly increases pro forma debt and leverage and carries substantial regulatory uncertainty which we believe will drive continued weakness,” Sorbara said.

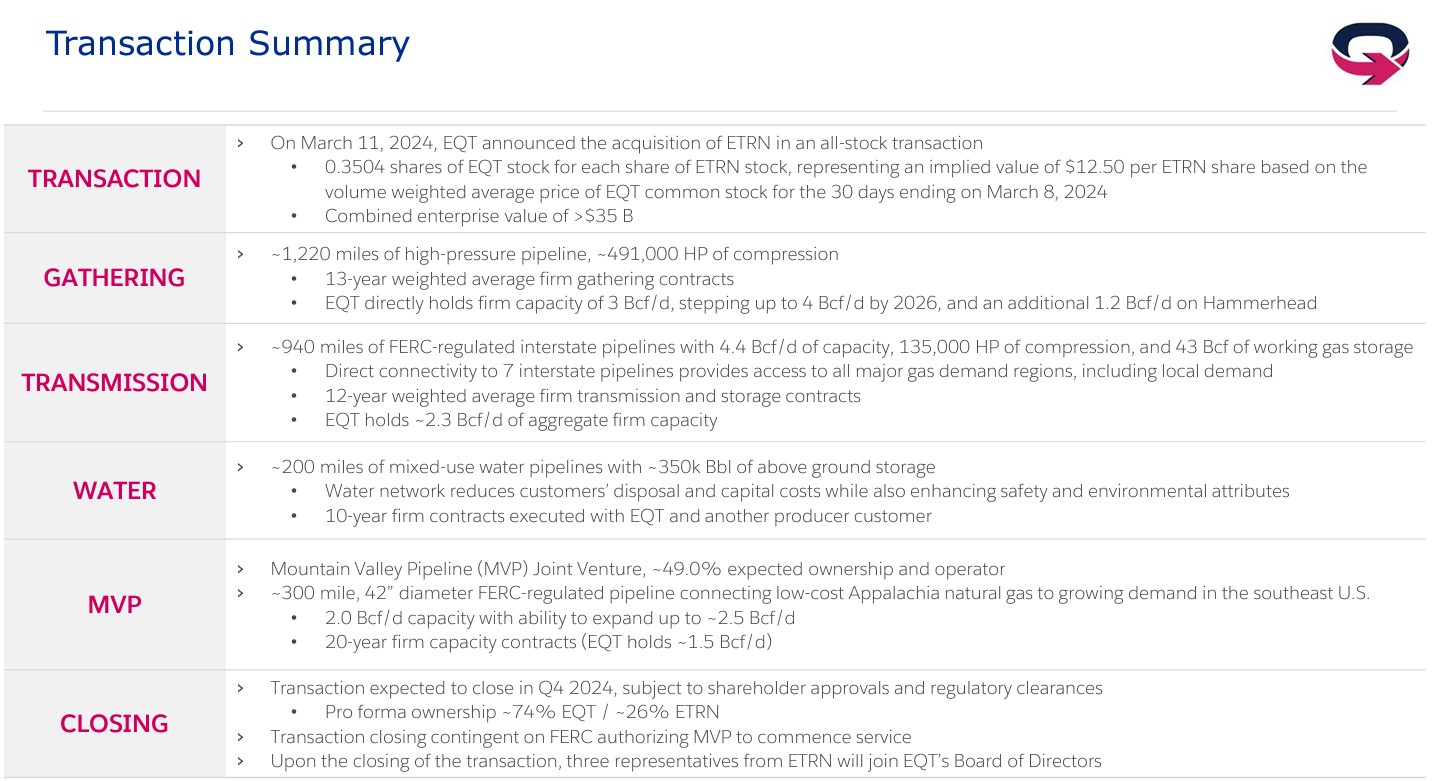

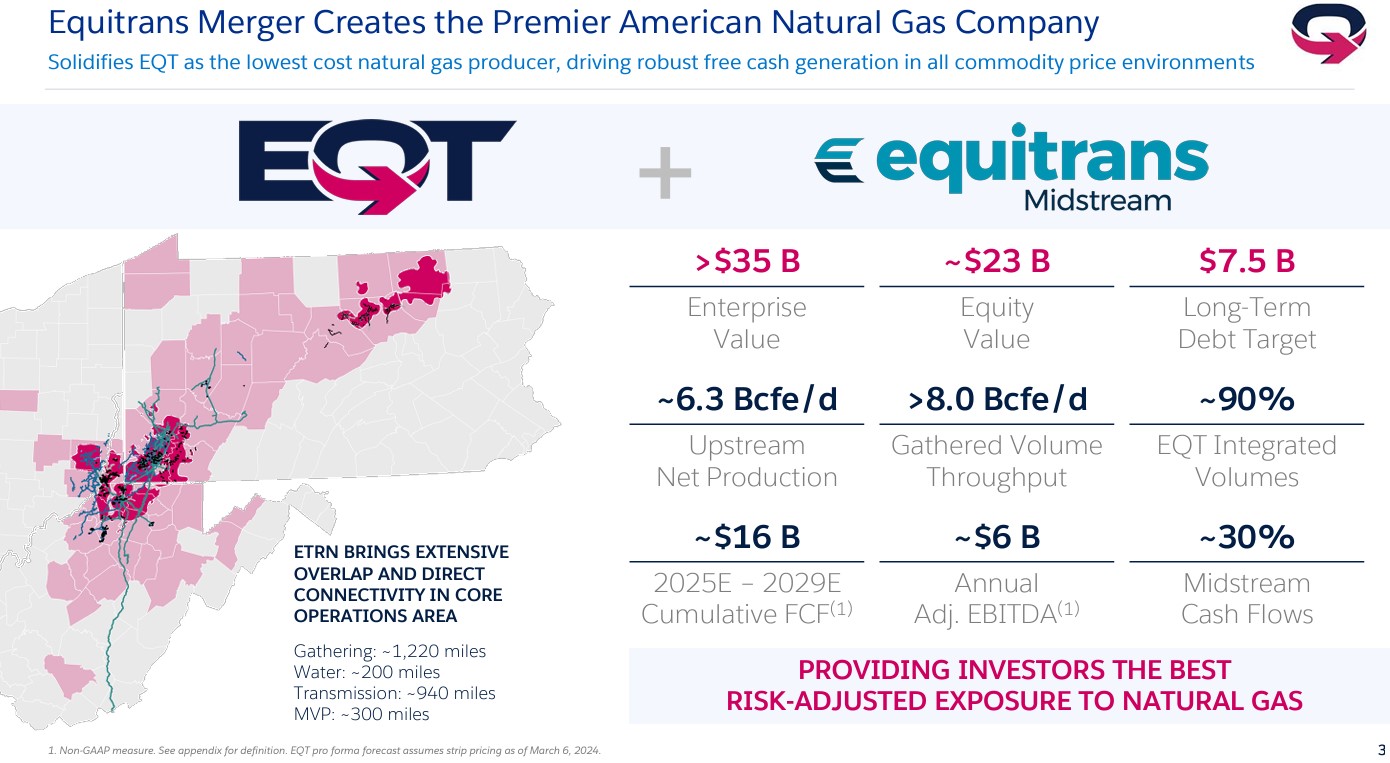

EQT’s rationale for the deal is simple: The company will become the only large-scale vertically integrated U.S. natural gas company. Equitrans’ 2,000 miles of pipeline will integrate with EQT’s upstream assets to create a company capable of breaking even at natural gas prices as low as $2/MMbtu.

On a March 11 call to discuss the transaction, EQT President and CEO Toby Z. Rice said its upstream acquisitions have shared a common theme: pipelines.

“Each acquisition we’ve done included midstream ownership, which was by design as we recognized early on the strategic value associated with owning integrated midstream infrastructure,” Rice said. That includes EQT’s acquisition last August of the $5.2 billion Tug Hill and XCL Midstream acquisition.

“Pro forma for Equitrans, approximately 90% of our operated production will flow through EQT-owned midstream assets, creating unrivaled margin enhancement relative to the rest of the industry,” Rice said.

EQT executives said that at prices of $2.75/MMBtu, most of its natural gas peers do not generate “any” free cash flow in maintenance mode without hedges.

By locking in a low-cost price structure, EQT executives said the company would virtually eliminate the need for hedging—a strategy that protects on the downside but, as with the post COVID-19 price spike, costs EQT more than $5 billion in lost revenue.

“Though the acquisition does not inorganically grow EQT's inventory, the addition of ETRN's midstream assets materially drops the breakeven price of the remaining ~4,000 locations below $3/MMBtu with ~3,000 locations below $2.50/MMBtu,” David Deckelbaum, TD Cowen managing director, wrote in analyzing the deal.

Long-term, EQT management projects cumulative free cash flow of about $16 billion at strip through 2029, Deckelbaum said.

M&A to solve debt

Near-term, the tension for EQT is that the Marcellus and Utica shale E&P will spend up to 18 months chewing through $5.5 billion in debt after the deal closes.

To tackle the debt, the company plans sell off $3.5 billion in “highly coveted noncore assets.” The rest will be paid through organic excess free cash flow. EQT executives said sales could include Equitrans’ Appalachian crown jewel, the Mountain Valley Pipeline (MVP).

EQT CFO Jeremy Knop said assets sales will be focused on some of Equitrans’ assets regulated by the Federal Energy Regulatory Commission (FERC).

“MVP certainly could be part of that. It's a very logical divestment candidate, one of the highest quality pipelines in the country with brand new 20-year contracts,” Knop said. “We do have that ongoing sale for our non-op assets that I would say that is going very, very well, and we hope to update investors on that in the near term.”

The transaction’s closing is contingent on FERC authorizing Equitrans’ MVP to commence service.

Knop agreed with an analyst’s scenario that the company would keep its base dividend while excess free cash flow would go toward debt repayment.

“With our deleveraging plan, the guidance we've gotten from the rating agencies has been post-closing. You typically have 12 to 18 months to complete that plan,” Knop said. “And we think with what we have on the table today and what we've outlined … we have really more than two times the number of sale candidates available.

“So we think that path to be leveraging is very low risk and very high confidence, something we can execute on in pretty short order. But really we're looking at mid- to yearend 2025 is that timeframe to get to that target debt level.”

Midstream, upstream behemoth

A combined EQT-Equitrans company would be formidable—EQT is the largest U.S. natural gas producer—but scrutiny from federal regulators is likely to be just as tough.

Rice was asked twice about the regulatory approval process during a call with analysts.

Rice said he wouldn’t speculate on the regulatory process, but he welcomed a chance to talk about the benefits of the transaction for the companies, the Appalachia region and the country.

“We are looking forward to discussing with regulators, especially in this environment where people are talking about energy. It's a political issue,” he said. “This is a great opportunity for us to communicate how this transaction is going to make the energy we produce more affordable, more reliable and cleaner.”

EQT’s Tug Hill/XCL acquisition won approval after more than a year of review by the Federal Trade Commission. The FTC ultimately allowed the deal to proceed by preventing “entanglements” between EQT and seller Quantum Energy Partners.

Likewise, other large proposed transactions, including Exxon Mobil’s proposed acquisition of Pioneer Natural Resources and Chevron’s deal to buyout Hess Corp., have been put under the microscope as Congressional Democrats raise anticompetitive concerns.

Pro forma, EQT would boast 27.6 Tcfe of proved reserves across about 1.9 million net acres, with 6.3 Bcfe/d of net production and more than 8 Bcfe/d of gathering throughput across 3,000 miles of pipeline. Some of that infrastructure serves third party producers that may be EQT competitors.

Combined, EQT and Equitrans would have an estimated market cap of $23 billion and add pipeline infrastructure that have “extensive overlap with EQT's core upstream operations and existing midstream assets.”

Under the terms of the merger agreement, each outstanding share of Equitrans’ common stock will be exchanged for 0.3504 shares of EQT common stock, representing an implied value of $12.50 per Equitrans share based on the volume weighted average price of EQT common stock for the 30 days ending on March 8. The transaction suggested a 12% premium compared to Equitrans’ March 8 closing price of $11.16.

After the deal, EQT shareholders would own 74% of the combined company, and Equitrans shareholders the remaining 26%.

The companies said the merger would create $250 million in annual synergies, including lower financial and corporate costs; uptime and production optimization; and reduced capital and operating costs. EQT has also identified an “upside pathway” to another $175 million in additional yearly synergies.

Recommended Reading

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

CorEnergy Infrastructure to Reorganize in Pre-packaged Bankruptcy

2024-02-26 - CorEnergy, coming off a January sale of its MoGas and Omega pipeline and gathering systems, filed for bankruptcy protect after reaching an agreement with most of its debtors.

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.

Canadian Natural Resources Boosting Production in Oil Sands

2024-03-04 - Canadian Natural Resources will increase its quarterly dividend following record production volumes in the quarter.

Bobby Tudor on Capital Access and Oil, Gas Participation in the Energy Transition

2024-04-05 - Bobby Tudor, the founder and CEO of Artemis Energy Partners, says while public companies are generating cash, private equity firms in the upstream business are facing more difficulties raising new funds, in this Hart Energy Exclusive interview.