AUSTIN, Texas—It’s not all doom and gloom in the energy market, not by a long shot. In fact, public equity valuations are “astounding,” Joe Gladbach, managing director, Jefferies LLC, said at Hart Energy’s 8th annual Energy Capital Conference in Austin.

“Looking at next 12 month EBITDA, companies are being priced equivalent to $80 WTI, right now,” he said.

“If you price them at Nymex, their multiples would be way off the charts. Implicitly, and none of the analysts will tell you this, but their consensus pricing is showing $80 flat. That tells you that everyone in the industry believes that $80 per barrel is going to happen next year—so watch out.”

The stars of the show have been the public equity and debt markets and private capital, which have been “extremely robust,” he said.

Prior to Gladbach’s speech, crude prices jumped some 5% to top $52 per barrel (bbl) after Saudi Arabia hiked prices for crude shipments to Asia.

Summing up the less-cheery energy fundamentals, Gladbach said, “M&A sucks, oil is coming back, we have more natural gas than we can consume in our lifetimes, and gas prices will stay down for a long, long time.”

On the other hand, “Everyone with a dollar in their pocket thinks they can be an opportunistic oil and gas investor,” he said, to appreciative chuckles from the audience of upstream financiers, advisers and producers. “We’re screening those so we can get the legitimate investors to the table. The capital markets are doing well and, once again, are saving our bacon.”

Jefferies has been involved in some influential deals of late, including:

- March -- Advised LinnCo LLC (NASDAQ: LNCO) on a financial joint venture (JV) with private capital investor Quantum Energy Partners for $1 billion;

- January -- $500 million for a LinnCo drilling entity with GSO Capital Partners in January;

- December -- A buyside deal for FourPoint Energy and EnerVest worth nearly $2 billion for Granite Wash assets; and

- 2014 -- Midstream financings for Chevron (NYSE: CVX), $800 million, and Kinder Morgan Inc. (NYSE: KMI), $71.7 billion.

Gladbach, a geological engineer, said he was impressed by how rapidly the upstream industry has responded to the current downturn, the fourth he’s seen. He called the response from a capital structure and operational standpoint “quick and thoughtful.”

Drilling and completion optimization and service cost reductions are helping producers live to fight another day and “making plays still highly economic, particularly in the tier 1 onshore acreage.”

Private capital firms are the differentiator this time around, he said, with an unprecedented amount available to help the industry “work through this.”

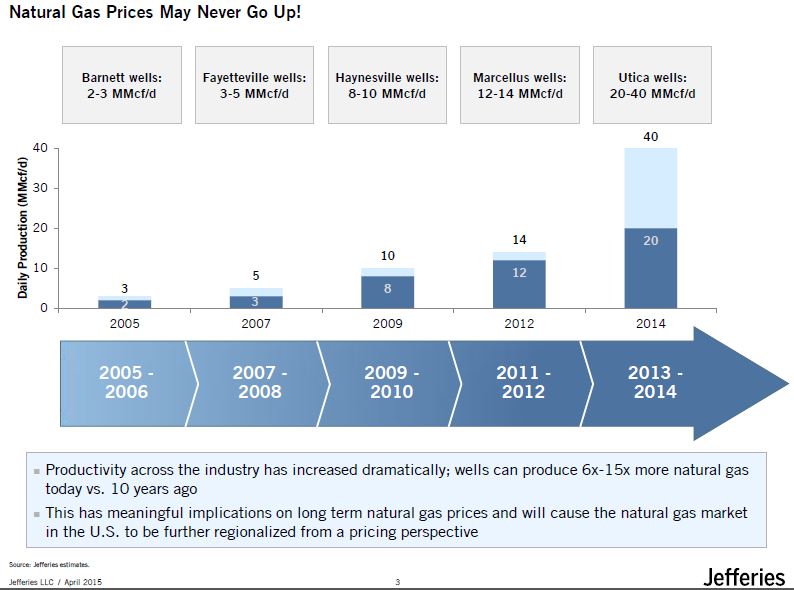

On the natural gas front, prices might never go up, he said. High-rate Marcellus and Utica shale wells are producing up to 15x what average gas wells produced a decade ago. Further, looming in the wings are currently forgotten giant gas shales like the Haynesville. LNG exports won’t be a game changer for natural gas for quite a while, he said, predicting prices of $3 to $4 for the next five years.

Crude’s ride will be bumpy, with prices changing week to week. Regardless, he looks for a significant spike in 2016 and 2017, with a “strong consensus around $80 for 2016.”

Supporting his oil price outlook is a projected decline of 1.5 MMbbl/d in North American production for 2016, matched with 1 MMbbl/d in demand growth, for a total need of 2.5 MMbbl/d.

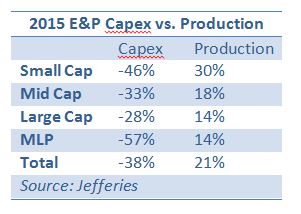

He said it was “intriguing” that producers large and small are cutting 2015 capex by nearly 40% but some still project production will rise 20%.

Falling Rigs

Rigs are fast disappearing from the drilling landscape, as rig counts have dropped 46% in the U.S. and 81% in Canada.

The Permian Basin, Eagle Ford and Bakken are taking the brunt.

But that’s not all bad.

That rigs are falling from view so quickly is positive in the long run, Gladbach said, suggesting crude prices would turn around quickly as a result.

Further, the quick reductions are “by choice.” Conventional plays, with higher risk profiles than the shales, have dropped rigs by 55% and will continue to register the highest declines.

Even at current Nymex prices, the resource plays have “really good returns” available in the top four or five plays’ core areas, enhanced by service cost reductions and completion optimization. EURs have responded.

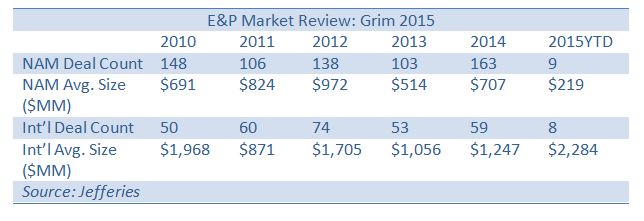

The cash M&A market is currently “dead,” he said, with a paltry $2 billion in deals done so far in North America in 2015. However, observers believe stock mergers have a better chance of getting done.

Despite the downs, investors remain eager. Concho Resources (NYSE: CXO) made a recent large equity offering, noting that the company didn’t even need to clean up its balance sheet—it is “pristine,” Gladbach said.

Rather, the moves are more about being positioned to take over companies or be taken over. Great assets and balance sheets allow companies to “play offense and defense, simultaneously,” he said.

Private capital is stepping in and financings are taking every conceivable structure, he said. The money is ready to be put to work, where to do so and how. About $100 billion is dedicated to the energy industry and ready to be deployed.

“Hedge funds have shown up and shown up in force,” he said. “More than 10 firms have raised new funds with less than 10% deployed.

“Every firm is focused on LP co-investment and new debt and equity funds continue to be formed in the space on a daily basis.”

Private equity and private capital are willing to fit private or public companies’ portfolios and needs. “They are no longer saying, ‘here are my terms, you will do as I say,’ but rather, ‘I have multiple structures, infinite flexibility—tell me what you need and I will put the right money together with your right assets and need.’”

There is a taste for gas; there is willingness to take undeveloped acreage or fully developed portfolios; and there are sizes of about $1 billion currently, but these can be scaled down considerably, he said. “We just did a second-lien deal for $200 million that had nine term sheets and nearly all were very competitive,” he noted.

The JV Nation

While the oil and gas JVs with international firms of days gone by are just that—gone by—the financial companies have stepped into the void. Today, the list of JV partners is broader, he said, including hedge funds.

Gladbach outlined the asset and drilling JVs Jefferies recently advised on for LinnCo.

- Asset-level JVformed to fund drilling capital associated with undeveloped assets owned by company in a structure suited for MLPs

- Operator allocates undeveloped wells to partnership in annual tranches

- Investor funds majority of drilling capital associated with these wells

- Operator retains a carried working interest

- After investor achieves specified rate of return on each tranche, operator claws back a majority of working interest

In the acquisition deal, a new entity is formed as a partnership between a company and private investors to acquire and develop assets. They are managed by the company in exchange for a management services fee, and the company’s ownership in AcqCo, the entity created by LinnCo and Quantum, increases over time after certain investor return hurdles are achieved.

Recommended Reading

US Raises Crude Production Growth Forecast for 2024

2024-03-12 - U.S. crude oil production will rise by 260,000 bbl/d to 13.19 MMbbl/d this year, the EIA said in its Short-Term Energy Outlook.

E&P Highlights: March 11, 2024

2024-03-11 - Here’s a roundup of the latest E&P headlines, including a new bid round offshore Bangladesh and new contract awards.

Galp Seeks to Sell Stake in Namibia Oilfield After Discovery, Sources Say

2024-04-22 - Portuguese oil company Galp Energia has launched the sale of half of its stake in an exploration block offshore Namibia.

Exxon Versus Chevron: The Fight for Hess’ 30% Guyana Interest

2024-03-04 - Chevron's plan to buy Hess Corp. and assume a 30% foothold in Guyana has been complicated by Exxon Mobil and CNOOC's claims that they have the right of first refusal for the interest.

Petrobras to Step Up Exploration with $7.5B in Capex, CEO Says

2024-03-26 - Petrobras CEO Jean Paul Prates said the company is considering exploration opportunities from the Equatorial margin of South America to West Africa.