Rystad believes the reinvestment rate—the ratio of capex and cash flow from operations—is in decline from a high of 72% reached in the second quarter. (Source: Shutterstock)

U.S. shale oil producers’ high reinvestment rates are expected to drop this year as inflation eases and global oil prices increase, according to a study by Rystad Energy.

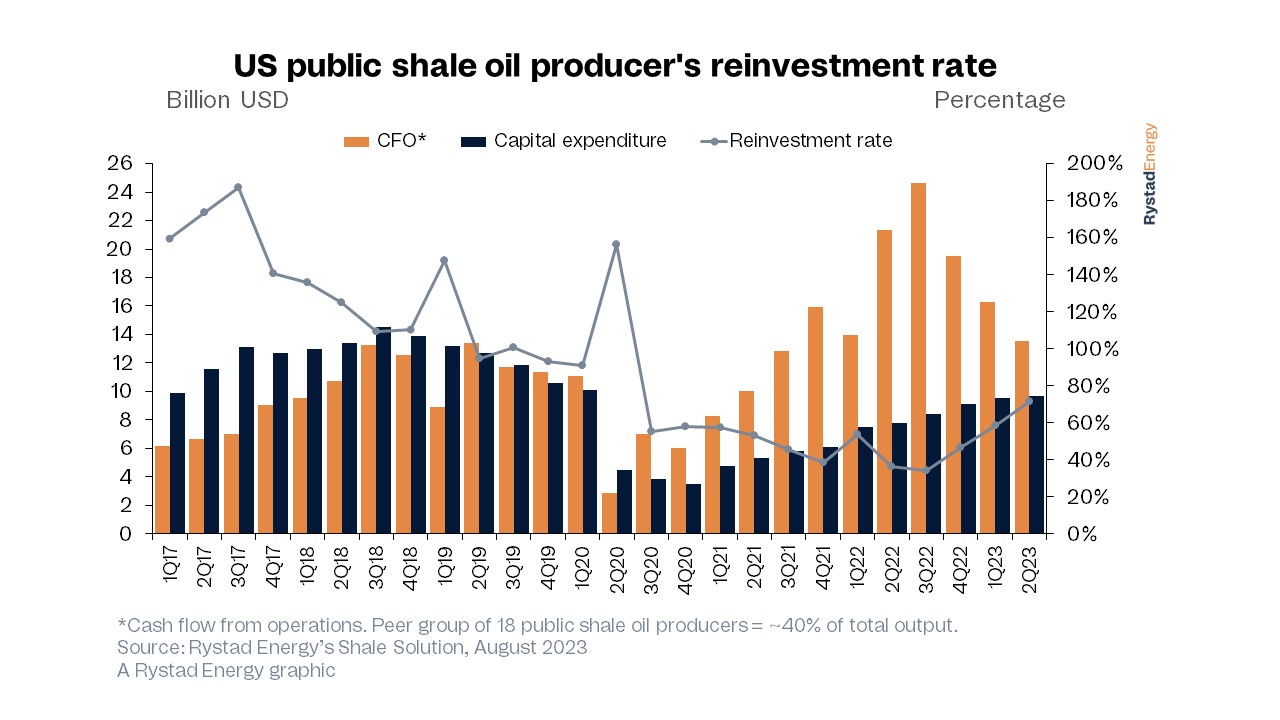

Reinvestment rates—the ratio of capex and cash flow from operations—hit their highest level in three years in the second quarter, Rystad found.

The Norwegian energy research company studied 18 public E&Ps and found their reinvestment rate was the highest in 2020 when it reached 150%. The rate was 58% in the first quarter of this year and 72% in the second quarter. Capex rose for 10 straight quarters, reaching $9.7 billion in the second quarter.

Matthew Bernstein, Rystad senior upstream analyst and author of the study, said the rate appears to have hit its peak and is already reversing.

“The price inflation that has caused service prices associated with drilling and completing wells to skyrocket during 2022 has mostly leveled out, and executives have voiced confidence during earnings calls that we will soon start to see deflation,” Bernstein told Hart Energy. “This is partially driven by the reduced drilling activity that has occurred over the last several months which equals less rig demand. Some segments include rigs, steel, fuel and oil country tubular goods where some deflationary signs are visible.”

Another factor is that many companies have already spent most of their capex budget for the year. The study noted that “the vast majority of our operators have spent more than 50% of their guided 2023 budgets during the first two quarters, with several having only 45% or less to invest.”

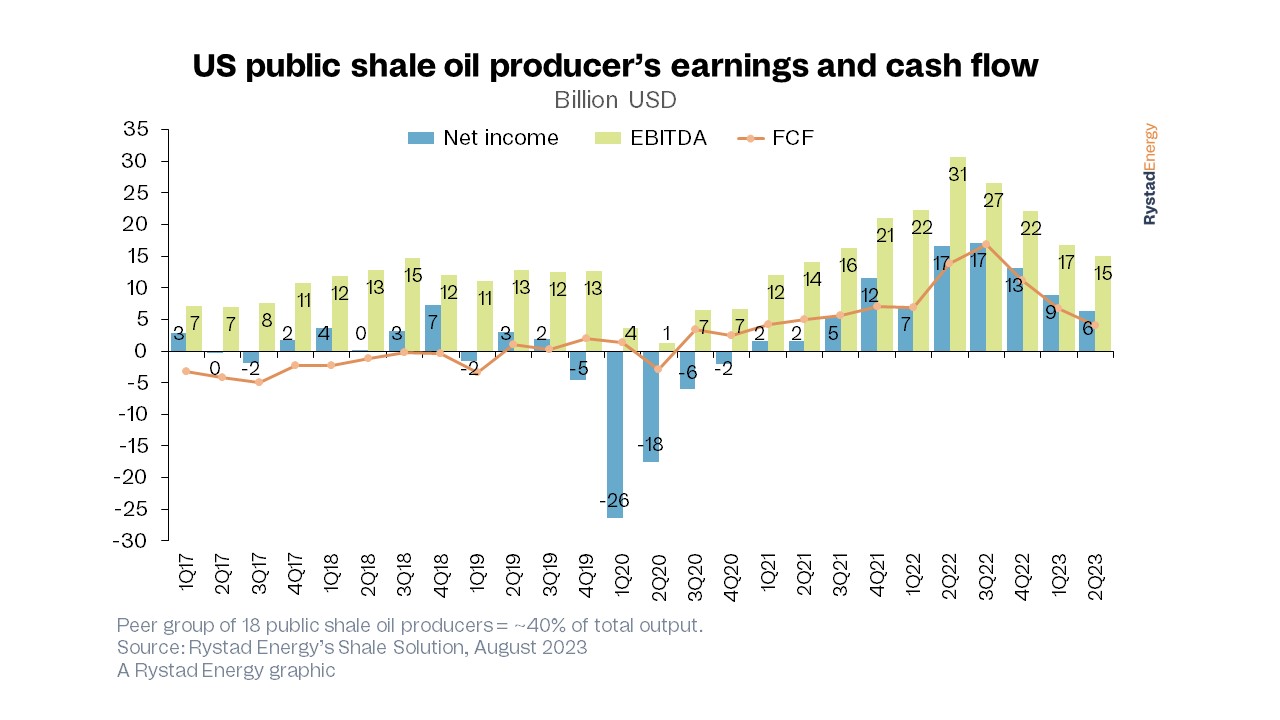

Rystad found cash from operations to be declining since third-quarter 2022, when it peaked at $24.6 billion. Cash from operations is now at $9.7 billion.

However, Bernstein said he does not see the shift as an immediate threat to the generous shareholder returns that have been a hallmark of the industry’s current era of capital discipline.

“The new business model puts investor returns over growth. While the absolute dollar value of returns is based on how much revenue is generated, we would expect capex to be reduced in the name of keeping up returns, even if prices should decline later in the 2020s,” he said. “Investors have been generally understanding of the market conditions that have thus far inhibited further cash generation, and thus payouts.

Many operators have bound themselves to cash return pledges and issued modest guidance for organic growth, prompting investors to align their expectations to market conditions.

“As long as E&Ps remain committed to capital discipline, investors will likely not punish them,” he said. “Still, in the longer-term it could be difficult to please investors if prices fall significantly.”

The study found stock repurchases to be down to $1.7 billion or 17% of capex among the 18 E&Ps studied.

Declining capex costs were specifically mentioned in the most recent earnings calls by leaders of Diamondback Energy, Permian Resources, Southwestern Energy and others.

The group of E&Ps studied since 2019 dropped to 18 from 39 due to bankruptcies, privatization and M&A. Other companies studied include Ring Energy, EOG, Devon Energy, Ovintiv, Vital Energy, Hess Corp. and Civitas Resources. Major oil companies were not included in review.

Recommended Reading

Kosmos Energy’s RBL Increased, Maturity Date Extended

2024-04-29 - Kosmos Energy’s reserve-based lending facility’s size has been increased by about 8% to $1.35 billion from $1.25 billion, with current commitments of approximately $1.2 billion.

Barnett & Beyond: Marathon, Oxy, Peers Testing Deeper Permian Zones

2024-04-29 - Marathon Oil, Occidental, Continental Resources and others are reaching under the Permian’s popular benches for new drilling locations. Analysts think there are areas of the basin where the Permian’s deeper zones can compete for capital.

NOV Announces $1B Repurchase Program, Ups Dividend

2024-04-28 - NOV expects to increase its quarterly cash dividend on its common stock by 50% to $0.075 per share from $0.05 per share.

Repsol to Drop Marcellus Rig in June

2024-04-28 - Spain’s Repsol plans to drop its Marcellus Shale rig in June and reduce capex in the play due to the current U.S. gas price environment, CEO Josu Jon Imaz told analysts during a quarterly webcast.

US Drillers Cut Most Oil Rigs in a Week Since November

2024-04-26 - The number of oil rigs fell by five to 506 this week, while gas rigs fell by one to 105, their lowest since December 2021.