(Source: Shutterstock)

Current oil and gas market conditions have caused an unprecedented number of E&P bankruptcy filings. However, these troublesome times also create an A&D opportunity for those prepared, said a group of lawyers.

Although the current downturn presents new concepts and conditions that might make the acquisition process more challenging than in previous cycles, the lawyers, who spoke during a recent Summer NAPE roundtable discussion, expect E&P companies to continue to shed oil and gas assets out of bankruptcy, ultimately setting up a favorable landscape for stalking-horse bidders.

“If you are the stalking horse it gives you a leg up, allowing you to control the contours of what goes into the asset purchase agreement,” said Sarah Schultz, partner at Akin Gump Strauss Hauer & Feld LLP.

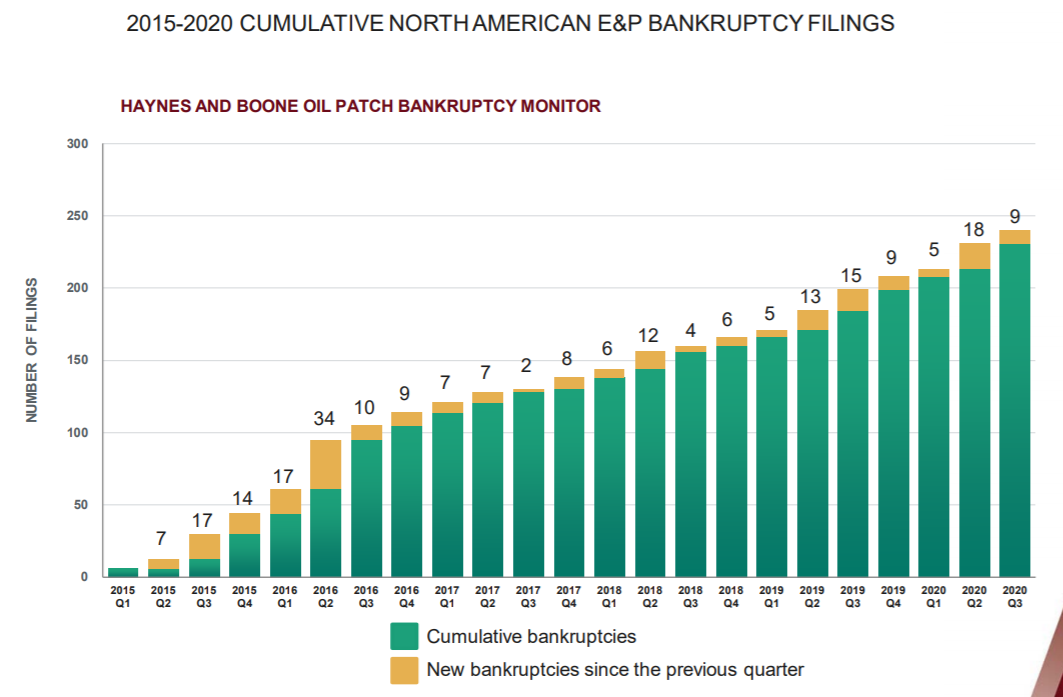

As of June 30, 23 E&P companies in North America have filed for bankruptcy so far this year, according to Haynes and Boone LLP. That number is expected to significantly increase in the second half of 2020. Most recently, bankrupt E&P, Lilis Energy Inc., switched gears to a sales process after a restructuring support agreement (RSA) with its biggest investor fell through. The Permian Basin pure-play had voluntarily filed for Chapter 11 bankruptcy on June 29.

In an Aug. 17 release, Lilis said that per the RSA entered into with its lenders, the company will immediately begin pursuing a process to sell substantially all of its assets with a hearing on bidding procedures scheduled for Aug. 21.

Schultz noted that, in Chapter 11 cases, the timeline is very compressed so potential stalking horses have to be prepared to react quickly. While there is a premarketing process where the banker will reach out to inquire if the buyer is interested in purchasing certain assets she said the process really starts when the procedures are approved by the bankruptcy court.

“Once those procedures are approved, that timeline from the date the order is entered until the date that the sale is going to be approved by the bankruptcy court can be very short like 50 days, which isn’t a lot of time for your due diligence,” she said. “But, it is not unusual for the process to move incredibly quickly in Chapter 11 because, frankly, you have a company that doesn't have the luxury oftentimes of liquidity to fund an extended process.”

Melissa Munson, Steptoe & Johnson PLLC member, agreed that stalking horse is the best position for a buyer but warned that there are a lot of risks with being the initial bidder like reputational costs and the repercussions of capped-bid protections. “Anecdotally, I think the stalking horse is in the strongest position to actually be the ultimate successful bidder when it comes to a 363 asset sale,” Munson said.

“But, I think it's worth noting that you can put a lot of time and expense into doing the due diligence, negotiating the asset purchase agreement, and ultimately, you are not the successful bidder and you don't end up closing the deal,” she continued. “While you do have some bid protections built in, sometimes those are caps and that expense can run well in excess of that cap and other buyers are potentially going to piggyback on your hard work.”

However, Munson noted the stalking-horse bidder’s ability to help design the framework for the deal by setting the floor price for the 363 asset sale, negotiating the initial asset purchase agreement and—more importantly—the bidding procedures with the debtor.

“The intent of the bidding procedures is to set an even playing field and encourage additional interest from the field to maximize the value of the estate,” she said.

The bidding procedures will include an outline of what the stalking horse is entitled to, and then ultimately it will include some language about how the sale is going to be approved.

In agreeance, fellow member at Steptoe & Johnson, Arthur Standish, said controlling the terms of the purchase agreement is important and favors the stalking horse.

“Debtors and courts don't like to see bidding contests,” Standish said. “So once the original asset purchase agreement is negotiated, most people, most bidders fall in line with that [agreement].”

To get a leg up on due diligence costs, Standish said the interested initial buyer should negotiate and help draft the ultimate sales order that the court approves and all the protections that come with it.

“By doing that, once the bidding procedures orders are entered into, it would short the due diligence period for any competing bidders that are out there, so you would have additional time to get your due diligence ahead of others,” he said.

On the flip side, he notes these deals typically fall under the “as is, where is” clause and they lack exclusivity.

“There's no sale protections in the bankruptcy process,” he said. “You may get into it and spend a lot of money and the court may not end up approving your negotiated-bid protections and the procedures that you wanted. There could be delays in the process which could drive your costs and if you actually lose the option, you may end up as a backup bidder.”

To avoid this, he said when shaping the contours of the contract, it is important to negotiate exclusivity provisions and no shop agreements, if possible.

As the stalking horse, the panelists agreed, it is important to be mindful of what the debtors as well as what the secured creditors behind the scene require, while also negotiating in provisions that protect them as buyers. Specifically, Munson said it is very valuable for interested buyers to understand their risk tolerance “because it’s not going to be a perfect asset, a perfect transaction or a perfect position”.

“If you want to participate in this space, be prepared to act early, act quickly, and you need to be prepared to act often because you're not always going to be the successful bidder,” Schultz added.

Recommended Reading

BP’s Kate Thomson Promoted to CFO, Joins Board

2024-02-05 - Before becoming BP’s interim CFO in September 2023, Kate Thomson served as senior vice president of finance for production and operations.

Magnolia Oil & Gas Hikes Quarterly Cash Dividend by 13%

2024-02-05 - Magnolia’s dividend will rise 13% to $0.13 per share, the company said.

TPG Adds Lebovitz as Head of Infrastructure for Climate Investing Platform

2024-02-07 - TPG Rise Climate was launched in 2021 to make investments across asset classes in climate solutions globally.

Air Products Sees $15B Hydrogen, Energy Transition Project Backlog

2024-02-07 - Pennsylvania-headquartered Air Products has eight hydrogen projects underway and is targeting an IRR of more than 10%.

HighPeak Energy Authorizes First Share Buyback Since Founding

2024-02-06 - Along with a $75 million share repurchase program, Midland Basin operator HighPeak Energy’s board also increased its quarterly dividend.