Diversified will add the equivalent of 122 MMcf/d to the company’s net 2024 production and will generate an estimated, adjusted EBITDA of $126 million, the company said. (Source: Shutterstock/ Diversified Energy)

Diversified Energy, which is taking advantage of weakness in the natural gas market, has entered into a conditional agreement with Oaktree Capital Management LP to upsize its interests in its previously acquired assets in Oklahoma, East Texas and Louisiana.

The deal, valued at a net $386 million includes the assumption of debt and adds price protection through a hedge book with a positive mark-to-market of approximately $70 million, Diversified said in a March 19 press release.

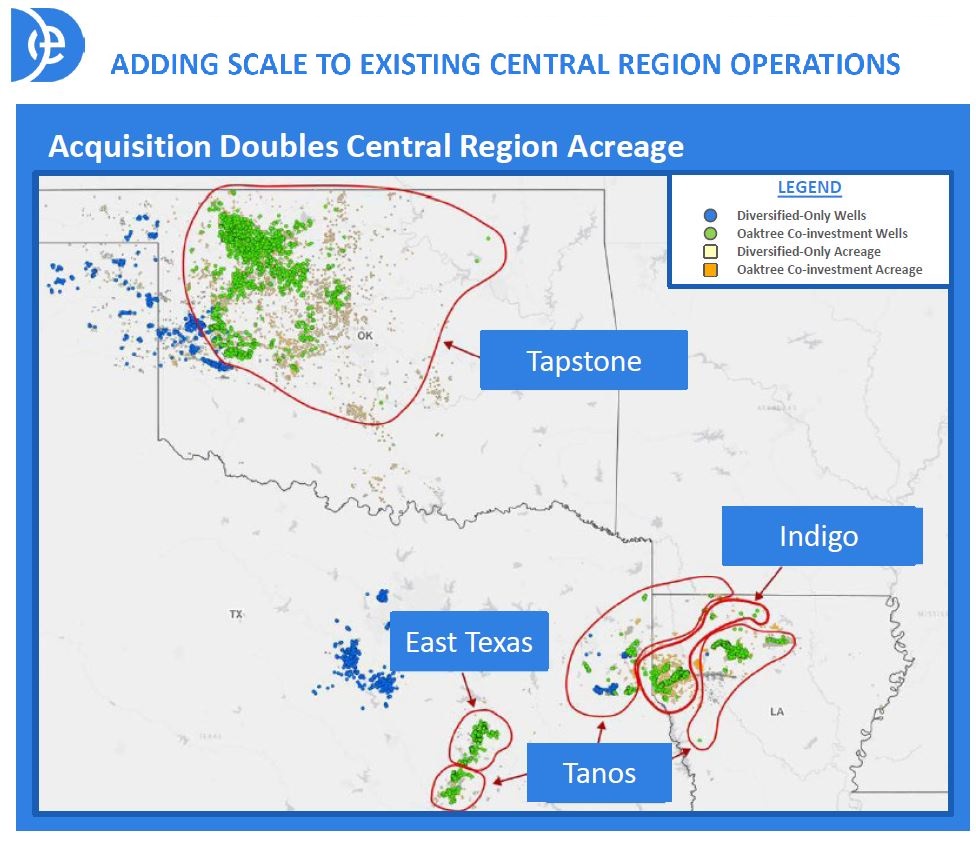

The transaction is a follow-up to a series of deals Diversified has executed since 2021 and targets Oaktree’s holdings in Tapstone Energy, Tanos Energy Holdings III LLC and Indigo Minerals LLC. The acquisition increases Diversified’s ownership of the assets to 100% from 51.5%. The company has operated the assets for the past two years.

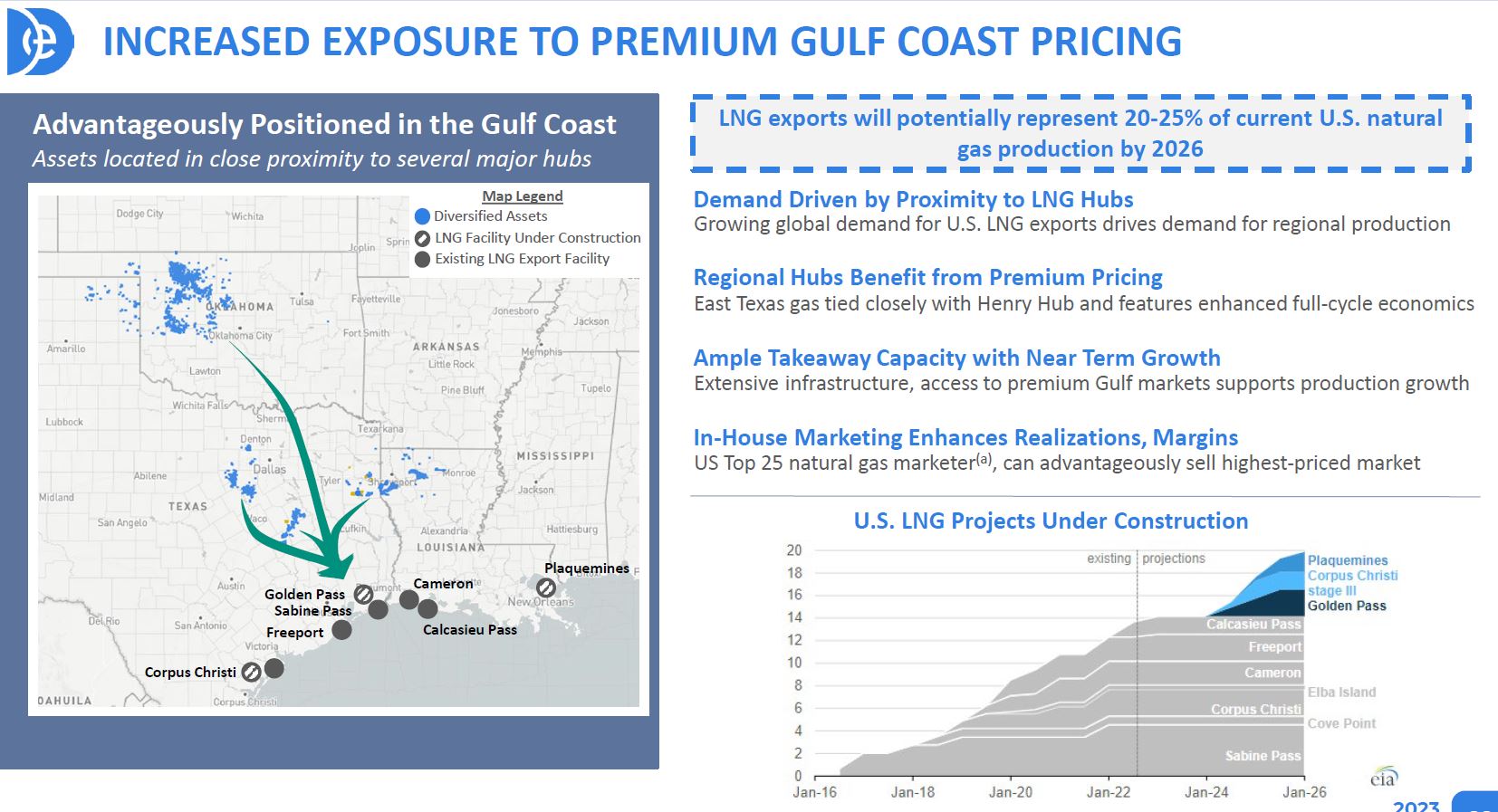

The deal is a bet on natural gas prices rising in 2025 and 2026 as several Gulf Coast LNG export facilities come online, Diversified CEO Rusty Hutson Jr. said on a March 19 call to discuss 2023 results.

While Diversified doesn’t sell to the export facilities, the company will benefit from rising prices based on basis differentials in the Gulf Coast, Hutson said.

“The price of natural gas in the U.S. is going to be highly fragmented between basins and this basin, the Gulf Coast, is going to have the ability to have the best pricing because of its exposure to these natural gas export facilities,” he said. “By the end of ’26, we could see 20% to 25% of our current U.S. production being exported, which is significant and I believe will underpin the gas price for a long time into the future.”

Hutson said the deal represents an acquisition cost equivalent to PV-17, with hedges providing a $0.10 per MMBtu uplift to Diversified’s production. At PV-10 pricing, the assets are valued at $462 million, the company said.

Hutson said the acquisition reduces the company’s unit costs by 2%, requires no increment G&A and will result in $15 million in cost efficiencies. Diversified will add the equivalent of 122 MMcf/d to the company’s net 2024 production and will generate an estimated, adjusted EBITDA of $126 million, the company said.

“It was the best asset we could buy in this market,” Hutson said on the earnings call. “The one thing that we wanted to do was, if we're going to acquire this asset, we definitely don't want to wait until in ‘25 and ‘26, which we believe will have an increase in natural gas prices as the export facilities start to come online. We didn't want to wait and have to acquire that asset in a higher price environment. It is a very strategic asset for us at this time in our company.”

Hutson acknowledged that 2023 has been a difficult year for natural gas producers.

“The gas market is sending a clear signal today; there is too much supply in the marketplace. Producers have already started to respond with reduced activity levels and production guidance,” Hutson said. “We believe Diversified is one of the best-positioned operators to take advantage of this lower commodity price marketplace. We are highly hedged in 2024, and our production base has one of the lowest decline profiles in the gas industry.”

But Hutson also pointed to what he called 2023’s “merger mania,” including $16 billion in gas-weighted deals and potential opportunity as those deals close.

“We know there's a backlog of mergers out there that will be coming to light over the next several months,” he said.

As those companies, including a proposed $7.4 billion combination of Chesapeake Energy and Southwestern Energy —Hutson said he expects significant divestitures to result.

“There will be large companies generated and built off the divestment of assets of these big corporate mergers, which leaves us in a good position as we move forward to be in line for these assets,” he said.

Hutson said he wouldn’t “rule out” Diversified becoming involved in teaming up with merger partners to continue to grow the company’s scale and business.

Diversified said the Oaktree acquisition’s gross purchase price is $410 million, subject to customary purchase price adjustments, including $120 million in debt and approximately $90 million in deferred cash payments to Oaktree.

Diversified said it may pay for the acquisition from non-core asset sales or the potential issuance of a private placement preferred instrument. The company does not plan to issue common equity as part of the acquisition, which will have an effective date of Nov. 1, 2023.

Legal firm Haynes and Boone, LLP advised Diversified on the acquisition.

Recommended Reading

BP Pursues ‘25-by-‘25’ Target to Amp Up LNG Production

2024-02-15 - BP wants to boost its LNG portfolio to 25 mtpa by 2025 under a plan dubbed “25-by-25,” upping its portfolio by 9% compared to 2023, CEO Murray Auchincloss said during the company’s webcast with analysts.

Sunoco’s $7B Acquisition of NuStar Evades Further FTC Scrutiny

2024-04-09 - The waiting period under the Hart-Scott-Rodino Antitrust Improvements Act for Sunoco’s pending acquisition of NuStar Energy has expired, bringing the deal one step closer to completion.

Chesapeake Slashing Drilling Activity, Output Amid Low NatGas Prices

2024-02-20 - With natural gas markets still oversupplied and commodity prices low, gas producer Chesapeake Energy plans to start cutting rigs and frac crews in March.

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.

Will the Ends Justify the Means for W&T Offshore?

2024-03-11 - After several acquisitions toward the end of 2023, W&T Offshore executives say the offshore E&P is poised for a bounce-back year in 2024.