(Source: Hart Energy/Shutterstock.com)

[Editor's note: A version of this story appears in the November 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

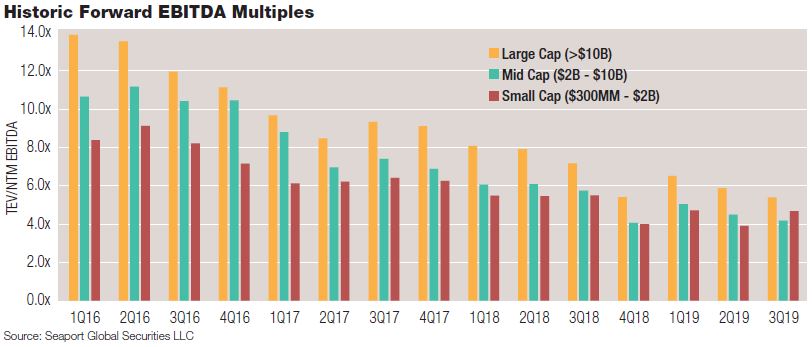

There’s little question that U.S. unconventional resource development has moved into manufacturing mode from what once was an era of nimble E&Ps aggregating acreage and testing target zones. Now a premium value is accorded economies of scale, an advantage enjoyed by integrated and many large-cap producers, while small/mid-cap (SMID) E&P stock valuations have been deeply derated.

With E&Ps facing a narrowing range of options, uncertainty is in the air. Access to capital markets, both equity and debt, is no longer available to many E&Ps. A new set of investors is increasingly pressing for “organic growth” and free cash flow (FCF). Priorities include cutting costs, extending liquidity, bolstering balance sheets, reducing FCF breakeven and returning money to investors.

No small challenge. Or maybe even mission impossible, if striving to reach all the above goals at once.

But what if consolidation can pave the way to greater scale and more easily attained economics? Could consolidation revive investor interest in energy, even if oft called-for mergers have—perhaps ironically—been met mainly by market sell-offs? Could an answer be to structure mergers as “zero premium” or “low premium” transactions among so-called “mergers of equals?”

Certainly, consolidation has worked in the past, especially when valuation disparities are wide. Even recently, management of Chevron Corp. described its now-expired attempt to take over Anadarko Petroleum Corp. as “an opportunistic bid” that was prompted by the sell-off of the E&P sector in last year’s fourth quarter, according to a recent RBC Capital Markets report.

At the time of Chevron’s bid for Anadarko, the average valuation held by Chevron and four of its peers was roughly 25% above that of Anadarko and eight other E&Ps, according to RBC. As of late August, after “continued derating of the E&P space,” the valuation gap was “much more extreme” at a 60% premium to the E&P group, said RBC, “although notably this is skewed by a few names.”

Compression of values

Away from the majors, historical valuation metrics may have less relevance, as much of the E&P sector has seen a sharp compression in values, with SMID-cap names losing several turns in enterprise value-to-EBITDA, or EV-to-EBITDA, ratios. Collectively, the sector’s stock values, as currencies for potential transactions, have largely fallen to levels unforeseen a few years ago.

So, with seemingly most E&P valuations under pressure, is a spree of consolidation set to get underway?

Clearly, benefits can accompany a combination, particularly in the areas of general and administrative (G&A) expenses and potential synergies in field operations if adjoining or nearby acreage exists in a common basin. But, equally, other issues abound: Which of the two executive teams will prevail? Will combined leverage blow out the balance sheet? What’s a good premium to pay, if any?

greater need to

achieve scale

in operations,

especially with

the advent of

unconventional

resources,” said

Charles Meade,

senior analyst

with Johnson

Rice.

In terms of arriving at the “right” premium to pay, one of the earliest advocates of a zero premium combination has been Kimmeridge Energy Management Co., led by founder and managing partner Ben Dell. He remains a staunch advocate of consolidation, describing the energy sector as “massively disaggregated” and in need of “single basin champions.”

In addition to backing E&Ps as a private-equity (PE) sponsor, Kimmeridge has held positions in a number of publicly traded energy securities, including that of PDC Energy Inc. Dell actively encouraged the board of PDC Energy to evaluate a possible combination after Kimmeridge had built a position, mainly in January and February of 2019, of a little over 5%.

Zero premium structure

“What the industry needs is zero premium combinations, where synergies and cost reductions increase returns to the shareholders, and SG&A [selling, general and administrative] is removed and management compensation is redesigned on absolute performance,” Dell told Investor in the spring of 2018. Also noteworthy was a position paper that Kimmeridge posted to its website on the subject of zero premium mergers.

“Since the reward for scale is so great,” the paper said, “we believe E&Ps should seek to consolidate with similarly sized companies, ideally on a zero premium premium basis.” Counterintuitively, it said with some insight, “a zero premium transaction could end up having the highest uplift.”

As it turned out, PDC Energy entered into a definitive merger agreement to acquire SRC Energy Inc. in August 2019. The all-stock deal was, in effect, structured as a merger of equals, although some pointed to terms amounting to a slight, 4% “take-under” of SRC Energy. In post-announcement trading, the stocks of both PDC Energy and SRC Energy traded measurably higher.

seen very few

instances of

these initial

synergies actually

materializing

into improved

financial

performance after

a deal has closed,”

said Betty Jiang,

CFA, senior E&P

analyst at Credit

Suisse.

PDC’s stock ended the day up 17.4% at $29.65 per share; SRC’s stock was up 12% at $4.65 per share.

The positive market reaction allowed investors to breathe a sigh of relief. Reflecting a reversal from earlier negative reaction to a series of mergers structured with significant takeover premiums, a research report by Johnson Rice & Co. was soon issued with the title, “How did the PDCE/SRCI (combination) break the run of (1 + 1 < 2) mergers?”

“The market wants to see consolidation among similarly sized companies, with no premiums, where the fruits of those combinations accrue to shareholders, and where you can be comfortable that you’re not giving away a premium for future synergies,” observed Dell, following the PDC-SRC merger. In addition, without a premium being paid, short sellers have little role to play, he noted.

Short sellers minimized

“When you look at the investor base that’s left in the energy group, there are not a lot of true, long-only investors left,” he commented. “So, if you pay a premium, the hedge fund community is going to sell short your stock pretty aggressively. But if you have a merger of equals, there’s no negative story out there to short. There are only cost synergies and benefits.”

Kimmeridge had earlier pressed PDC Energy to consider a consolidation strategy, and Dell was quick to commend the company for executing “essentially what we had recommended.

“Fundamentally, these companies are doing the right thing and should be applauded, especially SRC’s CEO, Lynn Peterson,” he said. “SRC is the one really making the brave bet, being the smaller of the two, and agreeing not to take a premium, realizing that’s better for its shareholders. In the end, the SRC investors got a big uplift in their equity through the transaction. That’s the key element.”

Single basin champions

Further industry consolidation is likely to continue across multiple basins, according to Dell.

“The Niobrara in the D-J [Denver-Julesburg] Basin is arguably a single field. The question is, ‘Why do you want 10 operators in a single field?’ Whether you see operators consolidating to create a dominant player, or 10 E&Ps forming a joint operating agreement [JOA], it comes down to taking costs out of the development of a single field.”

In terms of what constitutes a target level of scale, Dell pointed to 200,000 barrels of oil equivalent per day (boe/d), a threshold he estimated half the industry did not now reach. The PDC-SRC combination, on a pro forma basis, had output of nearly 200,000 boe/d in the second quarter. Of this, roughly 166,000 boe/d was produced in the D-J, making it the second-largest producer in the basin.

However, over time, Dell could see little reason not to consider further possible avenues to add scale.

“If I were PDC-SRC, I would look at consolidating with the D-J position held by Noble Energy [Inc.], or creating a joint venture with Occidental Petroleum Corp.’s assets [previously owned by Anadarko Petroleum Corp.],” he commented. “It doesn’t necessarily have to be a merger. It can be a JOA, or a joint venture, or a single field unit operating agreement.”

Why stocks ‘get hammered’

As indicated earlier, a recent Johnson Rice report focused on a conundrum regarding consolidation in the energy sector. It explored two questions.

First, why is it that, after investors have “clamored for consolidation,” the stocks taking part in a merger frequently “get hammered by the market?” And, second, while not unusual to see an arbitrage narrow on announcing an all-stock acquisition—with the bidder’s stock falling and the target stock rising—why would “the combined market cap of merging companies (end up) lower post-deal than pre-deal?”

In an analysis by Johnson Rice of 20 mainly E&P mergers in the energy sector, two findings came to light. One was that, post-merger, about half of the combined equity values of companies involved in a merger trailed their benchmark (for E&Ps, the XOP, or S&P Oil & Gas Exploration & Production ETF). A second was that “more than half” saw an absolute decline in combined market cap vs. pre-deal levels.

In theory, commented Johnson Rice, “investors who believe in synergies should reward the combining companies via increased market capitalization. But this hasn’t been happening much in energy.”

So what are some of the pitfalls that, in practice, may befall E&P mergers?

One of the key issues relates to the synergies projected in a merger being credible, noted Johnson Rice. Transaction costs in mergers are real and incurred upfront, whereas synergies tend to be less tangible and are only realized over a period of years. Another relates to balance sheet strength: What may be a de-leveraging transaction for one party may be one that levers up the balance sheet of another.

But among the chief drivers of mergers is still the issue of scale and what to do with E&Ps that are sub-scale. And the problem is unlikely to be solved by combining two sub-scale producers to create a third that is also still sub-scale, whether in the E&P or in the oilfield services sector, said Johnson Rice.

‘Engineering and production’

“There’s a greater need to achieve scale in operations, especially with the advent of unconventional resources,” said Charles Meade, senior analyst with Johnson Rice. “The industry has become more focused on engineering and optimization in unconventional plays. The joke is that the sector used to be called ‘exploration and production,’ and now it’s ‘engineering and production.’”

Given the resource is largely now a known factor, it’s “more a matter of how much you can get out and at what cost,” he continued. “Scale is one of the things you need to have to run an efficient rig and completion operation, and also spread out the fixed costs of operating over a larger base of production. That’s a different game than it was 10 years or more ago.”

Although it may vary by basin, Meade pointed to three rigs and one completion crew as typically being the “minimum acceptable” scale, while five to six rigs and two completion crews would be preferable in order to afford E&Ps greater flexibility in operating. “Just at that level—five to six rigs and a couple of completion crews—that’s a $1 billion capex program. That’s the big drive to merge.”

Assuming roughly $400 million of EBITDA is needed to fund a minimum three-rig, $400 million annual capex budget, as well as an EV-to-EBITDA multiple of 4 times, this would imply an enterprise value of around $1.6 billion. In turn, assuming a leverage ratio of net debt-to-EBITDA at a conservative 1.5 times, or about $600 million, this would imply a market capitalization of roughly $1 billion, noted Meade.

Stakes at the table

“It’s hard to get investors to care if you’re below $1 billion market cap or even $2 billion,” he said. “I’m not saying that’s right, or it will always be that way, but that’s the way it is right now. For an E&P trying to be an efficient operator in an unconventional play, those are the stakes at the table right now. The market is saying, ‘If you’re not at least that big, then it’s unlikely you’ll be good at what you’re doing.’”

In addition, in the near term, E&Ps are striving for more efficient levels of G&A, as measured on a per barrel of production basis, said Meade, “but I don’t see that as the big, strategic driver.”

Obviously, a number of factors played a role in each of the 20 M&A transactions reviewed by Johnson Rice in its report. That said, deals received poorly by the market generally reflected two factors: one involving migration by E&P into new basins, where synergies are less identifiable; and another involving mergers where—even after combining—the merged entity is still at sub-scale levels.

As for moves into a new basin, “I don’t want to suggest there’s no benefit from increased scale, but they are certainly diminished as compared to benefits of an intra-basin increase in scale,” said Meade.

The positive reception received by a handful of other deals, such as the PDC-SRC transaction, was attributed to several factors: synergies viewed as being credible; transactions structured with zero or low premiums, providing little room to argue the acquirer was ‘paying too much for this’; and combined leverage that was low, since “leverage has been just anathema in this market,” he added.

“The deals that worked have typically been intra-basin consolidations, where synergies are more credible and deals have low leverage metrics,” Meade said.

Meade is cautious, however, as to how broadly—or for how long—this formula may be applicable.

“I don’t think there’s a single magic formula. But this is one formula that, in the current environment, seems like it’s going to work,” he said. “That’s not to suggest it’s a formula that will work forever. But it seems to be what the market would like to see now.”

The PDC-SRC combination is described as a “no-premium premium deal” by Betty Jiang, senior E&P analyst with Credit Suisse. A positive reaction by investors may reflect the M&A market becoming more attuned to investor demands for mergers of equals, but she is not expecting a short-term swirl of similar deals due to a variety of factors that are likely hard to replicate.

First, why did the market effectively reward SRC Energy with a post-announcement takeout premium?

“It was a good deal and an accretive transaction, particularly in terms of FCF and with management committing to an increased return of FCF to shareholders, which should support the continued positive performance of the stock,” said Jiang. “SRC also had a very good balance sheet. By combining with SRC, PDC’s balance sheet remains very good. They’re not sacrificing their balance sheet in the merger.”

‘Clear, deliverable synergies’

The combination also brings together two sets of assets with “clear, deliverable synergies,” she said. In addition, any prior concerns of inventory depth at PDC are put to rest, as it is adding 86,200 net acres of core Weld County acreage for a total of 182,000 net acres. This gives PDC, now the second-largest producer in the D-J, about 10 years of risked inventory in the basin at its 2020 projected pace of drilling.

These positives helped overcome what was a series of deals that failed to deliver, according to Jiang.

“What we’ve seen in the past is that E&Ps have tried to justify deals with synergies, mainly G&A and some operational synergies,” observed Jiang. “However, investors have seen very few instances of these initial synergies actually materializing into improved financial performance after a deal has closed. Post-deal, the economics have rarely translated into one-plus-one equals more than two.”

As a result, this has “created a reluctance on the part of investors to pay for synergies upfront in the form of an M&A premium,” according to Jiang. “And if the market doesn’t believe in the synergies, or doesn’t want to give operators credit for those synergies upfront, then the market value of the premium paid in a deal is typically taken out of the buyer’s pro forma market cap.”

‘Basin jumping deals’

Another instance of investors being loathe to assume up-front synergies involves “basin jumping” deals, where a buyer goes into a basin in which it lacks an operational track record, said Jiang. This may take shareholders by surprise, prompting questions such as not only, “Why go into a different basin?” but also, “Are there unknown issues with your current asset portfolio?”

This may have contributed to negative reaction to deals such as Callon Petroleum Co.’s purchase of Carrizo Oil & Gas Inc. Not only did Callon pay a 25% premium, but the acquisition also took Callon, previously a pure-play Permian operator, into the Eagle Ford, and “that de-rated the shares,” commented Jiang. “The market reaction reflects in part an additional discount for multibasin E&Ps vs. pure-play Permian names.”

UPDATE:

Callon Petroleum Sweetens Deal Price For Carrizo Oil & Gas Merger

An early indication of the PDC-SRC deal potentially bucking the negative trend of M&A deals came in the wake of a news item—but no formal announcement as yet—suggesting a merger.

“With no additional details, PDC traded up on the headline,” recalled Jiang. “This was very different from any of the other merger headlines we’ve seen. The initial reaction to the PDC-SRC deal showcased that the market had already approved the synergistic benefits of having two companies combine that are located right next to each other and are trading at similar valuations.

“The uncertainty was what price was going to be paid,” she continued. “After the deal was announced, and terms called for a slight discount to Friday’s closing price—in essence a ‘no premium’ deal—then it really outperformed. It showed that the synergies were upside rather than baked in upfront. The market could see identifiable synergies: the acreage right next to one another, G&A that clearly can be reduced, etc.”

So does the PDC-SRC deal offer a sure-fire recipe for success that other E&Ps can also implement?

“It’s a success case that may make other managements think of it as a possible path,” commented Jiang. “At the same time, very few managements are really willing sellers at little to no premium at current stock price levels. If you have good assets, a good balance sheet, and your stock is at or near an all-time low, do you expect E&Ps to rush into a deal with little to no premium?

“On the other hand, buyers say their shareholders are pressuring them to not do deals where they pay up for assets, which means they can offer only very little to no premium. It’s difficult for the two sides to come together. The ones that really need to consolidate for financial reasons tend to have higher leverage. And it’s difficult for an E&P with a good balance sheet to buy one with a bad balance sheet.”

A ‘slow, arduous process’

Steve Trauber, head of global energy investment banking at Citi, sees consolidation in energy as likely being a challenging process—but an imperative one—given a variety of social and other issues.

everybody in the

sector recognizes

that consolidation

is the right thing

for the sector,”

said Steve

Trauber, head of

global energy

investment

banking at Citi.

“The problem

is that everyone

thinks that they

are going to be

the buyer.”

“I think interest in the sector will grow as consolidation becomes increasingly necessary,” said Trauber. “It is going to be a slow, arduous process. It is likely to take several years for the sector to consolidate into a much stronger position. Companies are going to have to merge to survive. There’s no doubt about that.”

According to Trauber, “almost everybody in the sector recognizes that consolidation is the right thing for the sector. People aren’t holding out, saying, ‘Look, I don’t think it’s the right thing to do.’ Everybody recognizes it. The problem is that everyone thinks that they are going to be the buyer. There’s not a lot in it for them financially to sell.”

Trauber praised the PDC-SRC deal, in which Citi advised SRC, saying “the reality is that they’re not selling; they’re combining on a stock-for-stock basis. These are the deals people want to see. You’re not transferring wealth from one side to another. The value being created from real synergies is accruing to the shareholders. These types of deals have to happen more readily.”

As for the Callon-Carrizo transaction, Trauber said a natural arbitrage trade of 5% to 8% was typical in a takeover, and the steeper sell-off may have reflected doubt about the size of synergies, a move into a new basin and an expectation among some investors that Callon would be a takeover candidate rather than an acquirer. “When it goes the other way, people sit on the sidelines,” he commented.

However, Trauber viewed both PDC and Callon as going on to be “natural acquirers” in their basins.

“At the end of the day we have to have some natural acquirers who can consolidate basins and take out costs,” he said. “There is just too much cost in these companies, and there’s too much leverage. Because they’re small, the cost of debt is so much higher. They need to get bigger so the costs of equity and debt can decline and so they can generate substantial returns in excess of the cost of capital.”

‘A better buyer’

“Once you get bigger, you become a much better buyer because there are a lot of E&Ps out there that don’t have the scale to be a buyer,” he continued. “This sector is consolidating, and there will be winners and losers. The winners will be those that do smart deals and get bigger.”

According to Trauber, combining two $2 billion or $3 billion E&Ps should only be “a first step,” since the advantages are not much greater than with a $3 billion company. “Until these guys get over $10 billion, they’re still too small,” he said. “Every company out there that is sub-$10 billion knows they need to buy or sell. The question is: ‘Who is the right buyer, and which ones are going to be sellers?’”

In terms of transactions getting done at recent low valuation metrics for E&Ps, “you’ve got to look at what is the relative value of what you are buying vs. the relative value of what you are selling in a stock-for-stock transaction,” said Trauber. “You’re giving up your currency at a low value, but you’re buying something at an equally low level. And the synergies are what help give you scale.”

In two or so years, the energy sector should be “stronger” and comprise producers that may be fewer in number but capable of making “substantial returns,” predicted Trauber. “But until they combine, take costs out of the business, increase scale of operations and drive greater efficiencies, it’s hard to see investors coming back to the sector.”

Michael Bodino, managing director of E&P and midstream investment banking at Seaport Global, offered a historical perspective of M&A trends as well as a forecast of M&A activity.

The recent energy environment is somewhat reminiscent of 1999, when Dot.com investing was “all the rage,” and the energy sector’s access to capital was “nonexistent,” recalled Bodino. This led to a surge in M&A activity during the 1999 to 2000 period marked by a number of highly notable transactions: what is now BP Plc buying Amoco Corp, Chevron Corp. acquiring Texaco Inc., etc.

picture is that

we expect to

see another 10

transactions

over the next

18 months,”

said Michael

Bodino, managing

director, E&P

and midstream

investment

banking, Seaport

Global.

While Bodino noted recent A&D activity has trailed prior periods, he counted 10 public energy M&A transactions in a trend that began in March of 2018. In terms of public mergers during the past 18 months or so, this was roughly equivalent to the total of M&A transactions completed during the prior four years from 2014 to 2017, he said.

Reading the tea leaves

“My reading of the tea leaves is that we’re going to see quite a bit of M&A activity through next year—and maybe beyond that,” he said. “The bigger picture is that we expect to see another 10 transactions over the next 18 months. We’ve talked to a lot of companies that are receptive to having conversations if it makes sense. No one is drawing a line in the sand and saying, ‘never.’”

Bodino cited three ingredients generally needed in a successful merger. First, “it’s got to be accretive,” meaning an E&P with a higher multiple stock acquiring a lower multiple one. Second, it should be de-leveraging, leaving investors with a “financially healthy company.” Third, it has to add inventory that “competes for dollars on an economic basis in the combined company.”

With investors urging E&Ps to generate FCF, “the only way you’re going to free up your capital is to cut costs and reduce capex,” he continued. “And that means you have to reduce leverage, which means you have to reduce G&A, which means you’ve got to get to scale. Very few smaller E&Ps are successfully growing organically out of cash flow after servicing debt and paying their G&A.”

In a study by Seaport Global of SG&A as a percent of EBITDA, looking at E&Ps with an enterprise value of less than $10 billion, SG&A expenses accounted for 23% and 18% of second-quarter 2019 and full-year 2019 estimated EBITDA, respectively. The above figures were calculated on a simple average basis, noted Bodino, and on a weighted average basis would come in at a reduced level of around 10% to 15%.

“If you can cut $100 million of duplicative G&A, and assume a five multiple of EBITDA, this would translate into $500 million of equity that could be created by a merger,” observed Bodino.

‘The best athletes on the field’

Of course, any merger is at risk of involving considerable downside from job losses, although in some cases employees may be able to “transition,” said Bodino. “There are very few deals where it is, ‘thanks, we don’t need anyone.’ The survivor wants the best athletes on the field. They go through a lot of due diligence to make sure they have the best team possible.”

Even if M&A lies ahead, Bodino signals caution about assuming it will follow the zero premium model.

“We don’t have many examples of zero premium mergers, just the PDC-SRC. That one doesn’t mean we’re going to have a bunch of zero premium transactions,” said Bodino. “I think the premium is a function of relative value as much as anything else. The problem is that the relative value of a lot of these E&P companies is relatively low, and they’re under pressure from shareholders to perform.”

While exactly how mergers are structured may be open to debate, the dynamics of the broader market may in the end force the hand of E&Ps.

“We’ve got to get bigger to be relevant,” said Bodino. “Twenty-five years ago we used to define small-cap stocks as less than $1 billion. Today, in the broader market, small-caps are considered to be sub-$10 billion. When you look at the energy sector, we really have an amalgamation of small-cap names. There are very few that qualify as mid- or large-cap when you compare them to the broader market.”

SIDEBAR:

G&A Metrics For SMID-Cap E&Ps

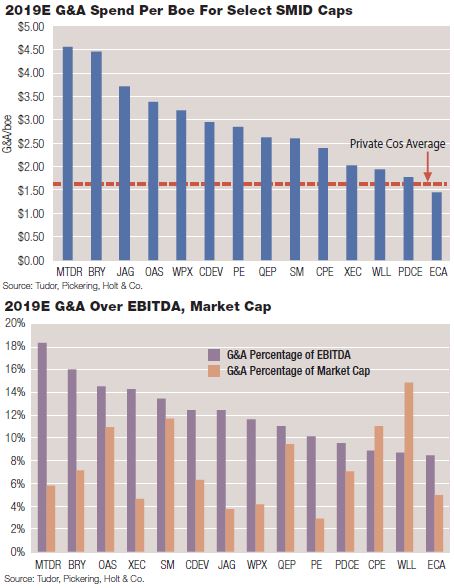

Tudor Pickering & Holt (TPH) conducted a study on general and administrative (G&A) expenses borne by the E&P sector within a framework of a variety of metrics, including G&A per barrel of oil equivalent (boe), G&A as a percentage of EBITDA, G&A as a percentage of market capitalization, etc.

“We expect the subject to remain topical,” said the TPH study, given the potential for increased M&A activity in which “G&A is typically the lowest hanging fruit to realize tangible synergies. The TPH study examined G&A levels at not only small/mid-cap (SMID-cap) public companies, but also at private E&P companies.

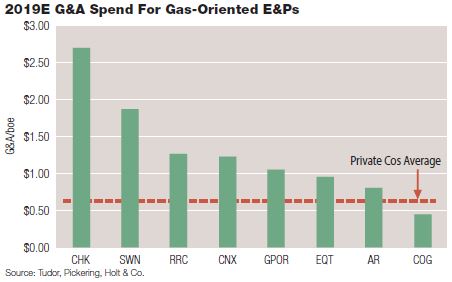

“The punch line is that private names are blowing away SMID-cap names (and some large caps) on cost metrics,” said TPH. For oil-oriented names, private operators spent an average of $1.65 to $1.70/boe on G&A, markedly less than the average $2.90/boe for TPH’s oil coverage. For gas-oriented names, private E&Ps’ G&A fell into a range of 50 to 70 cents/boe vs. $1.20/boe for TPH’s gas coverage.

Given SMID-caps’ substantially poorer G&A metrics vs. large-cap and private sector E&Ps, “many SMID-caps lack the scale or inventory to compete for investment dollars relative to large-cap peers,” said TPH. Its report pointed to two courses of action: “pursuing mergers to gain scale while driving tangible cost synergies;” and lowering G&A via “right-sizing of the organization into 2020.”

The SMID-cap oil group has the “widest dispersion” of G&A per boe metrics, said the TPH report. Data showed only Encana Corp. to have a G&A metric below the private E&P range of $1.65 to $1.70/boe, while nine SMID-caps showed G&A at least twice that of the private E&P average. Following mergers by Callon-Carrizo and PDC-SRC, TPH cited expected G&A reductions of 31% and 21%, respectively.

For the SMID-cap oil sector as a whole, if G&A per boe moved towards a “best in class” level—put at about $1.50 per barrel, or less—the savings would come to roughly $680 million. Using a 10% discount rate to arrive at a present value, and then applying a 6 times multiple, this could create a boost in equity value of some $3.76 billion to $4 billion, or a jump in equity appreciation of 10% to 15%.

Looking at the natural gas sector, the TPH report said that while M&A activity was “less likely in the near term given absolute debt levels and our bearish view on the forward curve, G&A reductions could materially help some names weather a $2.25 to $2.50/Mcf [thousand cubic feet] environment.” TPH data showed only one E&P, Cabot Oil & Gas, with G&A per boe that was lower than the private sector’s 50 to 70 cents/boe.

Recommended Reading

Initiative Equity Partners Acquires Equity in Renewable Firm ArtIn Energy

2024-04-26 - Initiative Equity Partners is taking steps to accelerate deployment of renewable energy globally, including in North America.

Energy Transition in Motion (Week of April 26, 2024)

2024-04-26 - Here is a look at some of this week’s renewable energy news, including the close of a $1.4 billion decarbonization-focused investment fund.

Solar Sector Awaits Feds’ Next Move on Tariffs

2024-04-25 - A group of solar manufacturers want the U.S. to impose tariffs to ensure panels and modules imported from four Southeast Asian countries are priced at fair market value.

Solar Panel Tariff, AD/CVD Speculation No Concern for NextEra

2024-04-24 - NextEra Energy CEO John Ketchum addressed speculation regarding solar panel tariffs and antidumping and countervailing duties on its latest earnings call.