[Editor's note: This article has been updated to add additional information.]

In what appears to be the largest Permian Basin deal of the year, Concho Resources Inc. (NYSE: CXO) said Aug. 15 that it will buy 40,000 net acres from Reliance Energy for $1.625 billion.

Concho said the acquisition features an average working interest of 99% and will add to the company’s core Midland Basin position. Reliance is a privately held company.

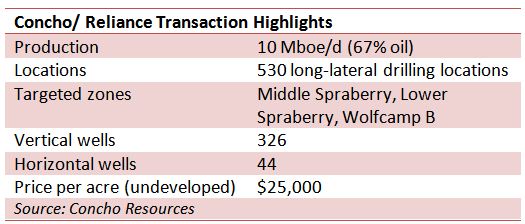

The Reliance addition will put Concho’s Midland Basin position at 150,000 net acres with production at 30,000 barrels of oil equivalent per day (boe/d).

Concho said the value of the production, based on current Nymex strip pricing, is about $500 million. The remaining $1.1 billion price tag will go toward acquiring 40,000 undeveloped acres.

Tim Leach, chairman, CEO and president said the transaction demonstrates Concho’s commitment to the Midland Basin as a core operating area.

“In line with the objectives of our southern Delaware Basin acquisition in the first quarter of 2016, these assets not only build scale, but more importantly high-grade our inventory with additional long-lateral locations that compete with the best projects in the Permian Basin,” Leach said. “As we continue to enhance our ability to efficiently allocate capital across our four key assets in the Permian Basin, we are uniquely positioned to deliver attractive returns today and build shareholder value over the long term.”

Wells Fargo Securities said the company paid about $31,000 per acre, in line with SM Energy Co. (NYSE: SM) acquisition in Howard County, Texas, of $32,000 per acre. On Aug. 8, SM Energy said it would purchase 24,783 net acres for $980 million.

The company said Aug. 15 that it would launch a public offering of 9 million shares of common stock to pay for the Midland Basin transaction. On Aug. 15, shares closed at $136.44.

The stock sale, with a 15% shoe, will generate estimated gross proceeds of $1.178 billion. The equity proceeds, cash and $600 million of senior notes will make up the balance of the purchase price, said David Tameron, senior analyst, Wells Fargo Securities.

“We estimate the transaction, expected to close in the fourth quarter, along with updated guidance is $0.12 accretive in 2016 and more than $0.60 accretive in 2017 to EPS,” Tameron said.

The acquisition adds about 48 MMboe in estimated proved reserves, 69% of which is proved developed reserves.

The acquired acreage is located in Andrews, Martin and Ector counties, Texas. The acquisition adds more than 530 long-lateral drilling locations to the company’s inventory.

The contiguous acreage allows about two-third of the locations to extend laterals to two miles. Remaining locations are 1.5-mile laterals.

Concho said substantial development upside is possible from optimal drilling and completion methods, testing closer well-spacing and delineating other zones.

Concho updated its full-year 2016 production outlook to a range of 1% to 3% annual growth to reflect production from the acquired assets in the fourth quarter. Capex will remain between $1.1 billion and $1.3 billion, excluding acquisitions.

For 2017, Concho expects to execute a capital program within cash flow and deliver about 20% annual production growth — with oil volume growth exceeding 20%.

The acquisition is expected to close in October and is subject to customary closing conditions.

Vinson & Elkins LLP acted as legal adviser and Evercore acted as financial adviser to Concho on the acquisition. Sidley Austin LLP acted as legal adviser to Reliance Energy.

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

TPH: Lower 48 to Shed Rigs Through 3Q Before Gas Plays Rebound

2024-03-13 - TPH&Co. analysis shows the Permian Basin will lose rigs near term, but as activity in gassy plays ticks up later this year, the Permian may be headed towards muted activity into 2025.

For Sale, Again: Oily Northern Midland’s HighPeak Energy

2024-03-08 - The E&P is looking to hitch a ride on heated, renewed Permian Basin M&A.

E&P Highlights: Feb. 26, 2024

2024-02-26 - Here’s a roundup of the latest E&P headlines, including interest in some projects changing hands and new contract awards.

Gibson, SOGDC to Develop Oil, Gas Facilities at Industrial Park in Malaysia

2024-02-14 - Sabah Oil & Gas Development Corp. says its collaboration with Gibson Shipbrokers will unlock energy availability for domestic and international markets.

E&P Highlights: Feb. 16, 2024

2024-02-19 - From the mobile offshore production unit arriving at the Nong Yao Field offshore Thailand to approval for the Castorone vessel to resume operations, below is a compilation of the latest headlines in the E&P space.