The A&D market has been a bit slow for the week of Feb. 15—perhaps the most interesting acquisition was Warren Buffett’s purchase of 26.5 million shares of Kinder Morgan Inc. (NYSE: KMI).

Buffett’s Berkshire Hathaway disclosed in Securities and Exchange Commission filings it bought the midstream giant’s shares for $395.8 million. The vote of confidence was enough to bump up Kinder’s stock by more than 10%.

Otherwise, M&A remains hit or miss. But it isn’t for a lack of sellers and, in particular, those that have gas assets. A commodity market stuck in reverse and overall uncertainty may mean buyers are more open to other assets—whatever makes money—over purchases of potential treasure.

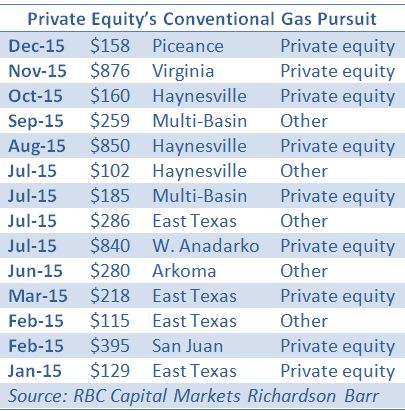

In 2015, natural gas deals were surprisingly fertile. Led largely by private equity cash, gas assets valued at $100 million generated $4.8 billion in deals, according to RBC Capital Markets Richardson Barr.

On Feb. 9, natural gas’ improbable market run extended into 2016. WPX Energy Inc. (NYSE: WPX) sold its Piceance gas assets for $910 million, below some expectations but still a strong price for producing gas assets.

Tudor, Pickering, Holt & Co. (TPH) said at the time that the sale is a good sign for other companies that want to sell gas assets. And the possible sellers include some big names.

Already, Anadarko Petroleum Corp. (NYSE: APC) has 50 thousand barrels of oil equivalent per day (Mboe/d) for sale and Devon Energy Corp. (NYSE: DVN) has at least another 45 Mboe/d legacy gas. Devon said Feb. 16 it would cut capex by 75%, make spending cuts and reduce its dividend.

TPH said other companies that may decide to divest gas assets include:

TPH said other companies that may decide to divest gas assets include:

- Carrizo Oil &Gas, Marcellus, 80 million cubic feet equivalent per day (MMcfe/d);

- EP Energy Corp., Haynesville, 85 MMcfe/d; and

- Newfield Exploration Co., Arkoma, 100 MMcfe/d.

Picky

Buyers are likely to be picky in the current oil industry malaise, seeking out returns without having to wait for a drilling program to prove up an asset.

In 2016, they will fine tune their operations and approach deals more conservatively.

Oil may have been a sought after commodity in the past several years, but it’s also been purchased in areas where the economics simply didn’t work even at $100 per barrel prices.

In a study released Feb. 16, Deloitte anticipates M&A motivations, such as preference for oil-heavy assets and buying for growth and scale are likely to change.

Companies that prioritize returns over size, have a balanced and flexible production profile rather than a deep inventory of non-producing assets and give thought to economies of scale are most likely to thrive when the price environment improves.

“There is no silver bullet solution that applies to the whole industry; in fact, the landscape has never been more complicated,” said Andrew Slaughter, executive director at Deloitte Center for Energy Solutions. “Each company has its own set of unique factors to consider—from issues specific to each producing region and asset, to various states of financial circumstances.”

In buyer’s favor, sellers in many cases will need to make deals.

Remaining solvent will require the same level of perseverance, innovative thinking and creativity as the technology breakthroughs that led to the boom in supply, Slaughter said.

Charles Robertson, analyst with Cowen and Co., evaluated cash flow for 51 E&Ps that represent 63% of U.S. onshore production. Taking into account hedging he sees equity or asset sales totaling $12 billion to meet their capex needs.

“Assuming these companies are unable to source financing, their 2016 spending would need to fall by 41% to stay within cash flow,” Cowen reported. “Shortfalls are expected to be met with equity and asset sales rather than debt given rating agency downgrades and limited debt capacity.”

Robertson said prices of $50 per barrel are needed to fund maintenance capital and keep exit rate production flat.

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Enterprise Increasing Permian NatGas Production

2024-04-03 - Enterprise Products Partners began service on two natural gas plants: the Leonidas in the Midland Basin and the Mentone 3 in the Delaware Basin, each with a capacity to process 300 MMcf/d of natural gas and 40,000 bbl/d of NGLs.

Paisie: Crude Prices Rising Faster Than Expected

2024-04-19 - Supply cuts by OPEC+, tensions in Ukraine and Gaza drive the increases.

US Gulf Coast Heavy Crude Oil Prices Firm as Supplies Tighten

2024-04-10 - Pushing up heavy crude prices are falling oil exports from Mexico, the potential for resumption of sanctions on Venezuelan crude, the imminent startup of a Canadian pipeline and continued output cuts by OPEC+.

US Refiners to Face Tighter Heavy Spreads this Summer TPH

2024-04-22 - Tudor, Pickering, Holt and Co. (TPH) expects fairly tight heavy crude discounts in the U.S. this summer and beyond owing to lower imports of Canadian, Mexican and Venezuelan crudes.

WTI Delivered to East Houston Hits Highest Premium in Nearly Three Years

2024-05-01 - Oil takeaway capacity from the Permian Basin will tighten next month due to scheduled pipeline maintenance.