The midstream adds storage capacity to handle a cascade of crude as the market awaits a demand rebound.

Straddling the U.S.-Canadian border, the Bakken Shale unleashes a torrent of light crude oil that slowly makes its way south by rail and pipeline. In the Midcontinent, the flow is joined by output from the Niobrara Shale and other plays, and then by the river of crude produced in the vast Permian Basin.

Add production from the Eagle Ford to the migration that has been dubbed a “cascade of crude” by Stratas Advisors, a Hart Energy company, and the North American petroleum empire invites an epic comparison.

‘Rome of the Gulf Coast’

“All pipelines lead to the Rome of the Gulf Coast in the United States, that is, to the Louisiana and Texas refining network,” Greg Haas, Houston-based Stratas director, told Midstream Business. “This presents an interesting opportunity for storage providers and/or developers here in the Gulf Coast area.”

Coastal facilities turn that crude into numerous refined products that are moved inland for domestic use or are exported to trading partners. Any surplus crude is loaded onto tankers and shipped overseas to customers in—no, wait … there’s a ban on exporting U.S. crude oil.

Rather than exporting excess crude oil production, surplus crude is pumped into storage facilities, most famously in the Cushing, Okla., storage and trading complex. But with crude supply outrunning current demand, production rising for most of the first half of the year even during the price crunch and no export safety valve, an oil glut is inevitable, isn’t it?

Not necessarily.

“You can’t have a supply glut for long in this market,” Andy Steinhubl, Houston-based principal, strategy, at KPMG LLP, told Midstream Business. “If you have an oversupply for a period of time, then the market dynamics of demand and price bring it back into balance.”

Supply shock

That’s pretty much what has happened. What Steinhubl calls a “supply shock”began when the unconventional technologies of horizontal drilling and hydraulic fracturing that liberated natural gas from shale were deployed in oil fields. The resulting boom in North American production prompted leading OPEC members to sacrifice price to maintain market share, calculating that U.S. producers would retreat in the face of relatively high unconventional extraction costs.

“If you go back about two years ago, you were seeing production ramp up something like 3 million barrels per day [MMbbl/d] incremental,” Steinhubl said. “Worldwide demand was only ramping up about 1 million bbl/d and the balance in between was storage. But at some point you run out of storage capacity so price has got to play a role in balancing the market. What OPEC decided to do was not continue to yield share.”

Instead, cartel members decided to hold share by maintaining their level of output. North American shale production continued to ramp up, so the only way for the market to find its balance was for the price of oil to decline, which it did.

“Then the supply started to ramp down—largely the shale supply, but also supply from more marginal deepwater projects and others like oil sands around the world,” Steinhubl said. “We had a price response to the supply shock leading to a supply response.”

OPEC, Steinhubl said, has at least temporarily relinquished its role of global swing producer. From the cartel’s point of view, if the price falls, then the price falls. It can take the hit, at least for a while. Its members have the currency reserves to maintain spending at lower oil revenues but not forever. In this scenario, U.S. light, tight oil inhabits the role of a scalable, flexible resource that can be quickly put on or taken off the market. In other words, shale oil becomes the swing producer.

Nearing balance

“Among other marginal barrels around the world, the higher-cost light, tight oil production is scaling back in the current price environment and bringing supply and demand back into balance,” he said. “We are pretty close to now being back into balance.”

James West, senior managing director of Evercore Group LLC, dismissed the notion of a worldwide oil glut.

“You hear about gluts over and over again,” he said at Mayer Brown LLP’s recent global energy conference in Houston. “We’re overproducing by about 1.5 million bbl/d today. We’re consuming about 93 million barrels of oil.

“If another industry is 98% utilized, you wouldn’t be talking about prices going down. You’d be talking about prices going straight up.”

West did not deny that a “perceived glut” exists, but he expects that notion within the industry and investment community to evaporate as U.S. production falls by 500,000 bbl/d by the end of 2015 and Brent’s price recovers to $80 per bbl.

Storage is tight

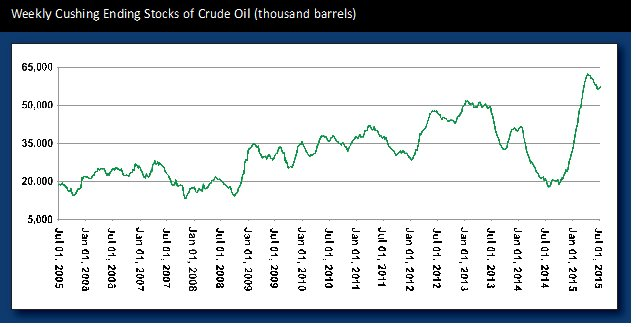

The oversupply of crude may not constitute a glut, but it strained storage limits in North America during the first half of the year.

“Clearly, it’s very tight,” N. Foster Mellen, senior strategic industry analyst, Global Oil & Gas Center, Ernst & Young, told Midstream Business. “We’ve got record supply of U.S. commercial stocks of crude.”

The great storage complex in Cushing has a capacity estimated by the U.S. Energy Information Administration (EIA) at about 71 MMbbl. Not all of the crude is in tanks. The EIA’s capacity figure includes pipelines and lease stocks or oil that has not entered into the supply chain.

Cushing’s highest utilization rate was 91% in March 2011. The recent buildout allowed the volume of oil stored to set a record in April of this year, even though the utilization rate only reached 78%“To push more crude into storage, we may need a bit sharper contango, which does not please the producers,” Mellen said. “On the flip side, the problem may have peaked in that we have some early signs that U.S. production may have peaked. We’ve had early indicators that production is starting to slide. The best guess from the EIA is that production peaked in March or April so that the storage situation is not likely to get too much worse, particularly given that refiners are now getting out of their turnaround season so we should start to see an uptick in demand for crude.”

Refining shift

The storage conundrum in the U.S. derives from the surge in unconventional production. Output from prolific shale plays like the Bakken, Permian and Eagle Ford has been shipped to the gates of refineries that had already been reconfigured to handle heavy crudes imported from Mexico and Venezuela. Now the refining system has shifted to incorporate more domestic light, tight oil onto its crude slates, displacing light, tight oil that had been imported, Steinhubl said.

In response, storage capacity has increased significantly on the Gulf Coast, but that storage is filling up. Still, Steinhubl is not concerned.

“Utilization is high but it’s not at a peak level if you compare it to historical utilization,” he said. “It’s just a structural shift because we’re now in a mode as a country of producing and consuming more barrels at the refining level, and so we’ve had to build out the storage infrastructure to accommodate that shift in production and the displacement therefore of imported barrels.”

To everything there is a season, and summer is the time to cut into that high storage rate.

“It’s full, but refiners are running it off,” he said. “It’s not filling up further. It’s hit a temporal peak and now as the summer driving season and refiners kick up their gasoline production, you’re starting to see that storage run down.”

CME Group’s Dan Brusstar and Erik Norland aren’t so sure. In a recent report they acknowledge that Americans are taking advantage of lower fuel prices and are driving more. They note that the 2.3% increase in miles driven, year over year as reported by the Federal Highway Administration, is the fastest pace of increase since 2005. They also cite Bloomberg for the figure of 16 million new cars and trucks purchased in the past 12 months. Presumably, their new owners will want to hit the road before the new car smell wears off, a factor that should add to miles driven and gasoline consumed in the U.S.

But CME notes another trend, as well: 2014 model year cars use 17% less fuel. “If such efficiency gains continue,” Brusstar and Norland wrote, “miles driven will have to rise by about 2.5% per year to offset the gains in efficiency and keep demand for gasoline stable.”

Future shock

Beyond the expected seasonal effects, the neat rows of massive steel tanks comprise the eye in a contango market storm. Swirling around them are metaphorical projections that barrels of crude will be more valuable in months to come than they are today.

“The other thing that drives storage is the traders,” Steinhubl continued. “They want to buy barrels today, stick it away if they think the market is going to move in their direction in the future.

“It’s interesting right now—there’s so much speculation in the market about exports or not exports, and the relative values of Brent and WTI [West Texas Intermediate] are bouncing all over the place as is the overall price of crude,” he said. “It’s been at a generally low level, $60 to $65, but it’s still balancing on a high wire, so currency fluctuations are changing it, negotiations with Iran about its nuclear program are changing it, so the volatility is very high right now, and the trading component of storage is alive and well.”

‘Money for nothing’

Appropriately for the industry that provides material used to create countless controlled explosions every day, volatility is what investors seek.

“Why do people invest in this sector? There’s a tremendous amount of access to capital,” said John Gerdes, managing director and head of research for KLR Group LLC, at the Mayer Brown conference. “The cost of capital in this industry is zero. It’s somewhere between zero and 10%. This industry gets money for nothing, not to quote Dire Straits, for some very good reasons.

“This is a highly volatile sector; it’s an amplified volatile sector,” he said. “How do you make margin as a financial participant? You make margin on volatility. It’s highly attractive. The reality is, you’ve got all that volatility set up— that’s a profit opportunity. It’s also a loss opportunity, but it’s a profit opportunity. So what do I get for that? I get money for nothing.”

There’s more to it than gaming the system, though, and Gerdes stressed that gas volumes coming from the Marcellus and Utica shales, oil generated by the Bakken, Midcontinent shales and the Permian and Eagle Ford plays in Texas constitute legitimate value creation. It’s the industry’s ability to create those volume wedges that sets the markets in motion.

“If you set up volatility and the panacea of value wedges, that’s massively attractive,” he said. “The $13 billion that was raised earlier this year was raised predominantly for one simple reason: People think oil prices are going to go back up.”

Steinhubl’s outlook is that interesting times will continue.

“Looking ahead, I perceive volatility,” he said. “I perceive generally, we’re going to get out of the current, slightly supply- overhang/flat-demand market to something where economies do recover, demand recovers, supply overhang goes away and we get back into some form of contango market, and all those things will drive demand for storage.”

The siege of the storage sectors from market factors will persist.

“It’s still a fairly weak situation for prices,” Mellen said. “The storage levels are extremely high. Storage on the Gulf is a little bit looser, but still it’s in the upper ranges, and we’ve still got a good amount of imported crude pushing its way in because of the fact that the global oil fundamentals are so weak that foreign suppliers are competing for market share. So we still haven’t backed out all of the U.S. imports that we could. A lot of those are also pushing up storage.”

Lift the ban?

But what if the ban on exports of U.S.-produced crude oil were to go away? Would that help? Gerdes is skeptical.

“We think the natural disposition is that LLS [Louisiana Light Sweet] will go from what was a $2 premium to a $2-to-$3 discount to international grade,” he said. “Why? To displace crude and incent internationally outbound U.S. crude oil.”

Gerdes cited internal North American tariffs on crude flowing from Cushing to the Gulf Coast.

“What’s cool is that, right now Brent and LLS are around parity, with a little bit of a mild discount to Brent,” he said. “The reality is, if LLS and Brent are around parity, whether you can export crude or not, you don’t have a financial incentive to do so. Remember, I don’t export crude offshore unless I’ve got $2 to $3 of price cushion.

“LLS has got to be $2 to $3 below Brent to absorb transport to international destinations,” he maintained. “Right now it’s about $1.”

Still, hope springs eternal for those desiring a lifting of the crude export ban, including Harold Hamm, chairman and CEO of Continental Resources Inc.

“Continental has been working hard with other industry leaders to lift the U.S. ban on crude oil exports,” Hamm told analysts during a first-quarter conference call. The current environment of world energy markets perfectly illustrate why this should happen, and I’m highly optimistic we’ll get this done this year.”

Hamm’s optimism that the ban could disappear in 2015 sets him apart from most observers of Capitol Hill, but his reasoning is shared by many in the industry and was echoed in a recent joint study released by the Harvard Business School and the Boston Consulting Group. Hamm told analysts that he believed many members of Congress were gaining knowledge about the issue and considered it, as he does, a relic of 1970s-era price control policies that contradict the country’s commitment to free trade.

“It is becoming widely recognized that sufficient refinery capacity does not exist in America today to process American light, sweet crude oil from shale plays such as the Bakken and we, the producers, are subject to a steeply discounted value as a result,” he said.

West agrees that the ban ultimately will be lifted, but not during the administration of a president intent on a legacy defined by, among other issues, its stance on climate change.

“We do expect the ban to be lifted by the next administration, probably on Jan. 21, 2017,” he quipped to the Mayer Brown conference audience.

Politically charged

But while the reasons to lift the ban may appear to be patently sensible within the industry, particularly in the upstream sector, it remains a politically charged issue to the public.

“Some of it comes down to: What do the voters think? What do the voters understand?” said Steinhubl. “Voters understand gasoline prices. Voters understand that somewhere back there is a correlation between lower crude prices and low gasoline prices. How much would prices rise if they allowed exports? These relationships are not well understood by the public.”

What can be counted on is a rising fear factor over the possibility of soaring prices at the pump fueled by election-cycle hyperbole over exports. But KPMG relies on hard numbers and economic fundamentals when it advises clients, and the economics indicate that U.S. gasoline prices would experience a small rise, if any, because gasoline trades on world markets and is not directly linked to the price of U.S. crudes. Separately, U.S. crude is currently discounted to world market levels. Steinhubl reminds that the differential between U.S. benchmark WTI and Brent stems from WTI’s inability to find its way to those markets due to export constraints.

“Does it show up in gasoline prices?” he asked. “No, it actually doesn’t because we still import crude and we still export gasoline and diesel at the margin. The U.S. consumer is actually seeing world pricing levels for products regardless of what’s happening at the crude level. All we’ve done in this country, effectively, is shift profits from the upstream to the downstream, because it’s the U.S. refiners who are taking that discounted crude and are able to convert it to world price products. We’ve really just shifted profits across the chain.”

Such is the economic reality that will dictate government policy the moment citizens enter voting booths influenced more by spreadsheets on their smart phones than emotions. Don’t count on it. In elections, voters prefer the sense of security offered by the concept of energy security. That means producing oil and gas and keeping it within the country’s borders.

But what would happen if the ban were lifted?

Brent parity

“What you’d see is, WTI would go to at least Brent parity,” Steinhubl said. “It’s been trading well below Brent parity because of the prohibition on exports. If the U.S. light crude barrel could compete on world markets, you would uplift the market, roughly speaking, by $10 per bbl. So yes, that would be a positive for producers.

“But that crude has got to be converted into product,” he continued. “What’s happening now is that discounted crude is being purchased by U.S. refiners and converted to world price products, so the economics are being captured by the refining sector today, which has actually been a positive for the refining sector. The energy industry all has an interest on the export question. The independent producers clearly want it because they have no offsetting benefit for a refining system. The independent refiners certainly don’t want it because then they lose the advantage of low-cost U.S. crudes by virtue of the discount. The integrated players, depending on their upstream/downstream balance, could be neutral.”

Gerdes sees it, too.

“What’s really wild is what the U.S. refining industry has done in terms of feedstock adjustments,” he said. “Over the last year what we’ve seen is a very significant amount of synthetic blending between lights and heavies to create, basically, a synthetic medium.

“The refining industry today has literally accomplished what U.S. crude oil exports arguably couldn’t.”

The only problem is one of principle: The concept of free trade is discarded.

“We really run against that thesis by not permitting crude exports,” Gerdes said. “But in practical economic terms, the spread relationships right now don’t make a lot of arbitrage sense in terms of actual outbound significance.”

Granddaddy of storage

The suddenly abundant resource won’t leave the U.S. anytime soon, except to journey to Canadian refineries on the East Coast. Should it go into the granddaddy of all oil storage units, the U.S. Strategic Petroleum Reserve (SPR)? For that matter, is the SPR even relevant since the advent of the shale revolution?

“The answer is yes,” Mellen said. “We have to remember that the SPR isn’t just for us. It is part of a broader agreement on the part of the OECD [Organization for Economic Co-operation and Development] countries to provide support for shocks in the oil market. The chances of those shocks have not gotten any less in recent years and don’t look to at any time in the foreseeable future.”

Declining U.S. demand and this country’s declining dependence on imports lessens the importance of the reserve domestically, Mellen said, but it retains its importance as a hedge against a possible global oil crisis, much like the stocks that exist in Europe and Japan.

That said, fixing it so that the SPR operationally is efficient certainly is worthwhile to do,” Mellen said. “I would doubt that we would see much of a movement to increase the amount of oil in the SPR but potentially, at these prices, it might make perfect sense to do that. Given the other budgetary issues the country faces, that’s probably not likely to happen.”

Steinhubl agrees.

“It’s a judgment call,” he said. “Do you think world events are such that the combination of our existing producing reserves with our existing strategic petroleum reserve is enough so that we can do without the Strategic Petroleum Reserve? Has the rationale, the imperative for it declined somewhat? Yes. Has it declined to zero? There’s still a lot of stuff that can go on in the world and we’re still not completely self-reliant.”

He also sees the equivalent of an industry extension of the SPR in the many wells producers drilled but chose not to complete when oil prices started to dive.

“In effect, we’ve extended our Strategic Petroleum Reserve,” Steinhubl said. “It’s not owned by the government but the amount of barrels that can very quickly come back into the market is quite high right now, which is why some people suggest that we could see a W effect in pricing.

“Instead of prices going up, there’s a lot of supply overhang—ready to come to market supply—that can quickly come back in and take price back down It’s not controlled by the government so it’s not literally the Strategic Petroleum Reserve, and the other aspect of that is, it’s a risk decision.”

What’s next?

Pearce Hammond, managing director and co-head of E&P research for Simmons & Co. International, gets this question a lot: Is the current price downturn a repeat of the 1980s

“There are so many differences,” he told the crowd at the Mayer Brown conference. “The biggest one is that global spare capacity is about 2.5 million barrels on a 90 million bbl/d market. It’s very small. Whereas in 1986, you were looking at somewhere around 16 million bbl/d on a 60 million bbl/d market as far as excess supply.”

Now that was a glut.

But there are other fundamental differences, Hammond said. Petroleum demand was on the decline in the 1970s because power generation was moving from oil to nuclear and coal as fuel sources. While U.S. oil demand slipped further over the intervening several years as drivers drove less and their vehicles became more efficient, U.S. fuel demand appears to be back on a growth trend amid the current low prices.

Continued crude supply growth amid tepid demand growth puts a premium on crude oil storage.

“We think that Gulf Coast storage will continue to be at a premium, simply because of all this light crude coming down,” Haas of Stratas said. “Then you add on top a significant influx of new heavy crude pipelines connecting Cushing to the Gulf Coast, so now you have the additional impetus of having segmented storage of crude oils.”

It’s not just the steady flow of light oil from the shale plays but the logistics of bringing in high volumes of heavy crude from Canada that keeps storage on the Stratas radar.

“On all fronts, we think the storage builds are a thing to watch,” he said. “It’s going to continue to happen just because of production and greater access to that production. Storage should continue to be at a premium.”

Uncertainty a certainty

The cascade of crude keeps flowing from north to south as demand wobbles and skittish prices, while climbing upward, seem reluctant to climb too high too fast. The certainty in the industry’s future seems to be uncertainty Mellen has kept watch over the industry for close to four decades.

“It seems like there’s more uncertainty but it may be, like a lot of things, it’s always been there but we just didn’t know about it,” he said. “We’re probably a lot more aware of uncertainty now. It seems like it’s higher than it’s ever been.”

But some aspects of the storage quandary seem quite clear.

“Long term, this will even out, but the storage overhang could hang over the market for quite some time,” said Mellen, who expects it to last into 2016. “It will have a dampening effect on prices. How much is still up in the air? We don’t know how fast U.S. crude production will turn down. There are estimates all over the map. And we also don’t know how strong of a pick-up in oil demand we might have over the next year.

“There are some early signs that we are seeing a fairly good recovery in U.S. oil demand,” he said. “So those factors would help alleviate some of the storage problems, but it’s going to take a while. We’ve just got a huge amount of oil in storage.”

Recommended Reading

Deep Well Services, CNX Launch JV AutoSep Technologies

2024-04-25 - AutoSep Technologies, a joint venture between Deep Well Services and CNX Resources, will provide automated conventional flowback operations to the oil and gas industry.

EQT Sees Clear Path to $5B in Potential Divestments

2024-04-24 - EQT Corp. executives said that an April deal with Equinor has been a catalyst for talks with potential buyers as the company looks to shed debt for its Equitrans Midstream acquisition.

Matador Hoards Dry Powder for Potential M&A, Adds Delaware Acreage

2024-04-24 - Delaware-focused E&P Matador Resources is growing oil production, expanding midstream capacity, keeping debt low and hunting for M&A opportunities.

TotalEnergies, Vanguard Renewables Form RNG JV in US

2024-04-24 - Total Energies and Vanguard Renewable’s equally owned joint venture initially aims to advance 10 RNG projects into construction during the next 12 months.

Sitio Royalties Dives Deeper in D-J with $150MM Acquisition

2024-02-29 - Sitio Royalties is deepening its roots in the D-J Basin with a $150 million acquisition—citing regulatory certainty over future development activity in Colorado.