Alaskan crude production declined from a peak of over 2 million barrels per day (MMbbl/d) in the late 1980s to an average 500,000 bbl/d in 2018, according to the Alaska Department of Revenue. Higher prices for this medium-sour crude now offer producers an incentive to expand output and exploit export potential to Asia.

Refineries in Washington State and California consume most Alaska North Slope (ANS) crude. Recent limits placed on Bakken crude sent by rail to Washington State restrict any growth in refinery use of competitive shale grades—potentially widening the domestic market for ANS.

So what are the market prospects for Alaskan crude production?

After most U.S. crude exports were banned in the 1970s to preserve dwindling national supplies, Alaskan crude was exempted from that rule during the 1980s. A further requirement—that the state’s most prolific ANS grade be shipped to market using expensive, U.S.-flag Jones Act tankers—priced Alaskan crude out of world markets.

Asian markets

When the export ban was lifted comprehensively at the end of December 2015—including the Jones Act restriction—ANS (a medium-sour crude with an API gravity of 31.5 and 0.96 % sulfur) became an obvious candidate for overseas sales. That’s because of its remote production location far away from U.S. refining markets and its relative proximity to Asian refineries. Many refineries in China, Japan and South Korea typically process medium sour grades from Russia and the Middle East that are similar to ANS, which can be delivered to Asia from Alaska in half the four-week journey time from the Arabian Gulf.

Since then, lower Alaskan production has restricted supplies to feeding regional refineries in Alaska, California, Washington State and Hawaii.

Unlike the U.S. Gulf Coast where surplus shale crude depressed domestic prices to attract overseas buyers, the lack of new ANS production has kept prices higher and closed the export arbitrage window.

Improving prospects

Today, there are better prospects for reversing the ongoing decline in Alaskan production. New discoveries and the recent application of more efficient technologies in the Prudhoe Bay, Alaska, region where ANS is produced led IHS Markit to forecast in August 2018 that output could grow by 40% in the next eight years to 2026.

Increased investment by legacy producers ConocoPhillips, BP, and ExxonMobil, as well as newer discoveries operated by Repsol, ENI, Hilcorp and the Australian company Oil Search, have all shown promise for future output. Note that these expansions underway do not involve the Arctic National Wildlife Refuge or the offshore Arctic Ocean regions that were opened when the Trump administration overruled Obama-era restrictions in 2017. In the second quarter of this year, the administration appeared to roll back that ruling until after the 2020 election in response to public opposition to expanded drilling.

Since the new discoveries and drilling described above are happening outside of these environmentally disputed areas, they will not be impacted.

Since the shale era, any plans to expand ANS output have been overshadowed by the rapid growth in production in Texas and North Dakota, both of which require lower investment and are closer to U.S. refineries. However, the attraction of ANS-quality crude to both West Coast and Asian refiners helps justify new investment today, at a time when the world is arguably oversupplied with light shale crude.

Although Alaskan drilling costs are high, producers can leverage existing infrastructure, such as the 2.1 MMbbl/d Trans-Alaska Pipeline System (TAPS) that carries crude 800 miles south from Prudhoe Bay to the ice-free deepwater Valdez oil terminal, from where it can be shipped to U.S. or overseas destinations.

Similar cost savings achieved by linking to existing infrastructure have recently increased investment in offshore Gulf of Mexico drilling, where typical crude quality is also medium sour.

TAPS room

With current Alaskan output not much over 500,000 bbl/d, there’s plenty of room on the TAPS pipeline for a 40% increase to around 700,000 bbl/d. At that level, ANS production would begin to exceed regional domestic demand—and encourage export flows.

Now, however, lower output and a lack of ready alternatives for regional refiners have raised ANS prices relative to both domestic and international grades. ANS prices earlier in 2019 averaged a premium of more than $9/bbl above the domestic benchmark West Texas Intermediate at the Cushing, Okla., trading hub, nearly 50 cents/bbl above international benchmark Brent and 65 cents/bbl above Mideast equivalent Oman crude.

ANS prices need to retreat below Oman to compete in Asian export markets.

Current demand

Current ANS production is either consumed by Alaskan refineries or shipped from Valdez on Jones Act tankers to Washington State and California, with a smaller volume going to Hawaii and exports confined to occasional spot cargoes, two in 2018, for example.

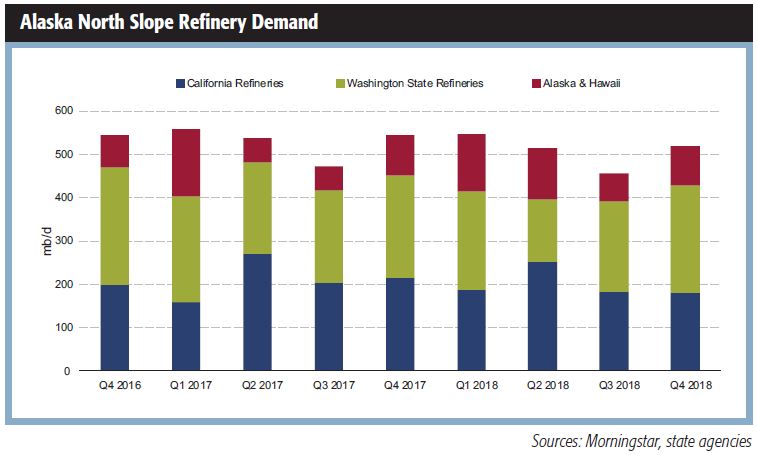

The accompanying chart shows our estimate of where ANS was consumed between the final quarter of 2016 and the fourth quarter of 2018. Volumes shipped to California, in blue, are from California Energy Commission reports. Volumes into Washington State, in green, are calculated from that state’s Department of Ecology crude movement reports. The balance, in red, is quarterly production, minus California and Washington volumes, that we assume is mostly consumed in Alaska.

During 2018, the averages worked out to be 200,000 bbl/d to California, 208,000 bbl/d to Washington State and 108,000 bbl/d to Alaska.

Export prospects

With current supply and demand for ANS tight, prospects for exports depend on increased production exceeding regional refinery requirements. Important variables in that equation include the impact of competing crude supplies from Canada and North Dakota delivered to Washington State refineries.

On average during 2018, North Dakota Bakken represented 17% and Canadian crude delivered by pipeline 20% of Washington feedstock, with most of the rest being ANS.

Two potential changes to Washington State refinery supply could affect ANS demand. The first is completion from the Trans Mountain Express pipeline expansion between Edmonton, Alberta, and Vancouver, British Columbia, that would increase Canadian crude supply to the West Coast by 600,000 bbl/d. This much-delayed project, now owned by the Canadian government, may not be complete until after 2021, but it would allow Washington refiners to increase Canadian crude runs at the expense of ANS.

Increased Canadian supplies at Vancouver could also be shipped down the West Coast to California with the same impact—freeing up more ANS for potential export.

The second change impacts the volume of Bakken crude railed from North Dakota to Washington State refineries. These shipments, which averaged 148,000 bbl/d during 2018, could be curtailed or limited by a Washington State regulation concerning the quality of crude permitted to move by rail.

That regulation restricts crude flammability by imposing a Reid Vapor Pressure (RVP) limit of 9 pounds/square-inch on crude. That reduces crude volatility in case of a rail accident—but is regarded as prohibitively expensive by Bakken producers since it requires pre-processing crude to remove light components.

The implication is that a ban on crude over 9 RVP would preclude shipments to Washington refineries, rendering them increasingly reliant on ANS supplies. The final iteration of the legislation only applies to incremental crude barrels, representing 10% more than previously shipped by rail.

That would reduce the impact on current ANS demand.

Time is right

Whatever happens with Bakken crude-by-rail or Canadian crude supplies, the potential for increased ANS exports relies firmly on production shifting to a higher gear in the next several years. Right now, the relative shortage of sour crude in world markets caused by OPEC production cuts and sanctions on Venezuela and Iran easily justify increased output of medium sour grades like ANS, which is pricing higher than Brent.

Producers are making that bet by investing and drilling to increase output—hoping to leverage existing infrastructure to keep costs down. If the forecasted increase in production happens, there should be a market for more ANS—either at West Coast refineries or in Asian markets.

Recommended Reading

Crescent to Offer $750MM in Senior Notes to Settle SilverBow Debt

2024-06-13 - Crescent Energy intends to use the proceeds to fund the cash portion of its merger with SilverBow Resources and to repay SilverBow’s outstanding debt at the time of the transaction’s closing.

Crescent’s Credit Score Found Positive Following $2.1B SilverBow Deal

2024-05-23 - Crescent Energy, which is in the process of buying SilverBow Resources, said ratings agencies Moody’s, Fitchand S&P Global reacted positively to the pending $2.1 billion deal.

Crescent Point Divests Non-core Saskatchewan Assets to Saturn Oil & Gas

2024-05-07 - Crescent Point Energy is divesting non-core assets to boost its portfolio for long-term sustainability and repay debt.

Diversified Closes $377MM Oaktree Acquisition

2024-06-07 - The acquisition grows Diversified Energy's scale, margins and free cash flow with the bolt-on of interests in Oklahoma, East Texas and Louisiana.

Evolution Petroleum Sees Production Uplift from SCOOP/STACK Deals

2024-05-07 - Evolution Petroleum said the company added 300 gross undeveloped locations and more than a dozen DUCs.