The recent downturn in oil price has demonstrated the resiliency of the U.S. shale and resource business. While painful in the near term for producers (but very good for consumers), this resiliency may allow the U.S. to maintain production higher than anyone had predicted, even in a $60-$70/bbl price environment.

From 2008 to mid-2014, the E&P business was built around speed during the rush to develop the shales. Those that missed the land rush, such as the majors and large international companies, needed to play catch up and acquire acreage or companies. Those that held the acreage, the large and small independents and some large private companies, needed more capital than they had available, and matching up these needs generated more than $300 billion in deals during this period.

This deal mania also fed a drilling mania driven by the need to prove up plays, or hold acreage, or achieve the development plans promised investors or, in the case of joint ventures, use the capital carries operators had been provided. This resulted in peaking U.S. rig counts and companies spending more capital than could efficiently be spent.

The massive drilling push caused U.S. oil production over the last four years to jump from less than 6 MMbbl/d to more than 9 MMbbl/d. Ultimately, the huge growth of supply in the face of weakening worldwide demand drove down oil prices. The OPEC reaction, especially from Saudi Arabia, was to maintain its production rate, which drove oil prices lower in the face of oversupply. The Saudis chose to defend market share, not maximize revenues, betting that the U.S. would ultimately have to cut its drilling activity, which should ultimately lower U.S. production rates.

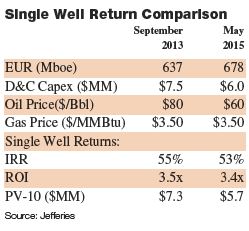

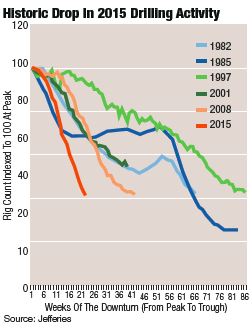

The cut in drilling in the U.S. occurred quicker than in any time in modern history. Investors demanded and companies adhered to living within expected cash flow as oil bottomed out at $45 per barrel. But the shock therapy also caused companies to pivot from going fast to being efficient, massively driving down capital costs. It is not an exaggeration that $60/bbl oil is now the new $80/bbl. Due to both reductions in capital costs and increases in ultimate recovery per well, companies can now achieve similar rates of return in a $60 world as those previously attained in an $80-plus world.

Combining capital efficiencies with improved recoveries will even further strengthen the U.S. For example, recovery factors for core Eagle Ford are 8-12% of oil in place. Consider the impact of being able to improve this to 20-30%. The best Permian sections contain more than 200 MMboe in place in more than a dozen potential producing benches. Think about the additional amount of oil available if technology allows production from all of these benches rather than just a few with this much oil in place.

Interestingly, the expected decline of U.S. production in the face of massive rig cuts has not yet occurred and price is decently stable at $60/bbl. This could mean we will live in a $60/bbl world for a long time with a continuing prosperous U.S. oil business with OPEC and others that count on $90/bbl for revenues being sorely disappointed. The tide could turn in the favor of the U.S., and the rest of the world will have to figure out how to cut production while the U.S. prospers in a $60/bbl world.

Deal flow will become even more concentrated in fewer areas. Instead of transactions being done broadly and widely dispersed in many early life plays, the industry will more narrowly focus on fewer plays but will go deeper in those plays.

Efficiency will be emphasized to distinguish the core from non-core areas of plays and efforts will continue to be more keenly focused in a $60-plus/bbl world. With the tremendous supply of private money dedicated to energy and the continued ability to raise money in the public capital markets, deal flow will grow back toward its normal $80-plus billion per year in the U.S. As investors scour the world for ideas, the U.S. should remain the top area in the world to invest in oil and gas.

—William A. Marko, Jefferies LLC, 281-774-2068, wmarko@jefferies.com

Recommended Reading

E&P Highlights: April 22, 2024

2024-04-22 - Here’s a roundup of the latest E&P headlines, including a standardization MoU and new contract awards.

E&P Highlights: Feb. 26, 2024

2024-02-26 - Here’s a roundup of the latest E&P headlines, including interest in some projects changing hands and new contract awards.

Deepwater Roundup 2024: Americas

2024-04-23 - The final part of Hart Energy E&P’s Deepwater Roundup focuses on projects coming online in the Americas from 2023 until the end of the decade.

Gibson, SOGDC to Develop Oil, Gas Facilities at Industrial Park in Malaysia

2024-02-14 - Sabah Oil & Gas Development Corp. says its collaboration with Gibson Shipbrokers will unlock energy availability for domestic and international markets.

Woodside’s GoM Trion Project Wins Social Impact Assessment Approval

2024-02-14 - Woodside Energy’s Trion is expected to start production in the Mexican sector of the Gulf of Mexico in 2028, and Woodside said the impact assessment will help the operator engage with local communities during the construction phase.