By Dan Steffens, Oilprice.com

Low oil prices today might be setting the world up for an oil shortage as early as 2016. Today we have just 2% more crude oil supply than demand and the price of gasoline is under $2 per gallon in Texas. If oil supply falls too far, we could see gasoline prices doubling within 18 months. For a commodity as critical to our standard of living as oil is, it only takes a small shortage to drive up the price.

On Thanksgiving Day 2014, Saudi Arabia decided to maintain their crude oil output of about 9.5 million barrels per day (MMbbl/d). They’ve taken this action despite the fact that they know the world’s oil markets are currently over-supplied by an estimated 1.5 MMbbl/d and the severe financial pain it is causing many of the other OPEC nations. By now you are all aware this has caused a sharp drop in global crude oil prices and has a dark cloud hanging over the energy sector. I believe this will be a short-lived dip in the long history of crude oil price cycles. Oil prices have always bounced back and this is not going to be an exception.

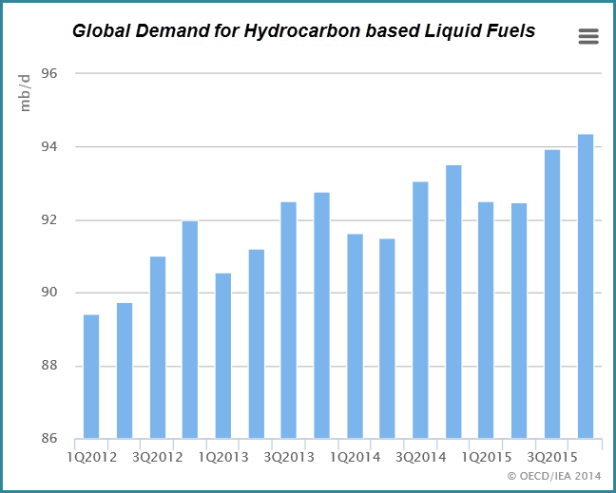

To put this in perspective, the world currently consumes about 93.5 MMbbl/d of liquid fuels, not all of which are made from crude oil. About 17% of the world’s total fuel supply comes from NGL and biofuels.

One thing that drives the Bears opinion that oil prices will go lower during the first half of 2015 is that demand does decline during the first half of each year. Since most humans live in the northern hemisphere, weather does have an impact on demand. I agree that this fact will play a part in keeping oil prices depressed for the next few months. However, low gasoline prices in the U.S. are certain to play a part in the fuel demand outlook for this year’s vacation driving season.

Brent oil prices are now hovering around $60/bbl. In my opinion, this is quite a bit lower than Saudi Arabia thought the price would go and might lead to an “emergency” OPEC meeting during the first quarter. But for now, I am assuming that Saudi Arabia is willing to let the other OPEC members suffer until the next scheduled OPEC meeting in June.

The commonly held belief is that Saudi Arabia is doing this to put a stop to the rapid growth of production from the U.S. shale oil plays. Others believe it is their goal to crush the Russian and Iranian economies. If the oil price remains at the current level for a few months longer it will do all of the above.

My forecast models for 2015 assume that crude oil prices will remain depressed during the first quarter, then slowly ramp up and accelerate as next winter approaches. I believe that by December we will see a much tighter oil market and significantly higher prices. In a Dec. 24, 2014 article in The National, Steven Kopits, managing director of Princeton Energy Advisors, states that, “In permitting low oil prices, the Saudis seek to bring the market back into equilibrium. At present, our calculation of breakeven system-wide is in the $85 to $100 a barrel range on a Brent basis.”

Mark Mobius, an economist and regular guest on Bloomberg TV, recently said he sees Brent rebounding to $90/bbl by the end of 2015.

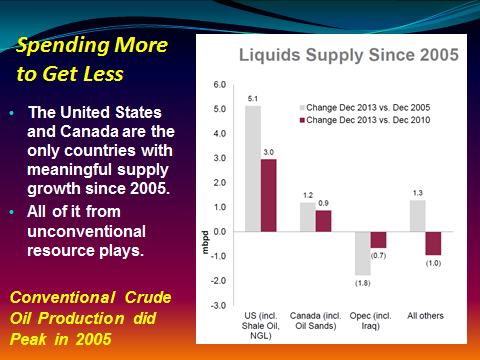

Since 2005, only North America has been able to add meaningful crude oil supply. Outside of Canada and the United States, including the Gulf of Mexico (GoM), the rest of the world’s crude oil production netted to a decline of 1 MMbbl/d from December 2010 to December 2013. More than half of the OPEC nations are now in decline. We’ve been able to supplement our fuel supply during the last ten years with biofuels, but that is limited since we need the farmland for food supply.

I believe the current low crude oil price could be overkill and result in the next “Energy Crisis” by early 2016. Enjoy these low gasoline prices while they last.

The upstream U.S. oil companies we follow closely are all announcing 20% to 50% cuts in capital spending for 2015. We will start seeing the impact on supply at the same time the annual increase in demand kicks in. Our model portfolio companies are all expected to report year-over-year (yoy) increases in production, but at a much slower pace than the last few years.

A study released by Credit Suisse two weeks ago shows that U.S. independents expect capex cuts of one-third against production gains of 10% next year. This would imply production growth of 600,000 bbl/d of shale liquids, and perhaps another 200,000 bbl/d from GoM deepwater projects. At the same time, U.S. conventional onshore production continues to fall. I have seen estimates of 500,000 to 700,000 bbl/d declines within twelve months. If these forecasts are accurate, U.S. oil production growth would be barely positive next year and headed for a material downturn in 2016.

North American unconventionals (oil sands, shale and other tight formations) have been almost all of net global supply growth since 2005. If unconventional growth grinds to zero and conventional growth is falling outright, the supply side heading into 2016 looks highly compromised. At today’s oil price, only the “sweet spots” in the North American shale plays and the Canadian oil sands generate decent financial returns to justify the massive capital requirements needed to continue development. Global deepwater exploration is rapidly coming to a halt.

Were demand growth muted, this might not matter. Demand for liquid fuels goes up yoy. It even increased in 2008 during the “Great Recession” and ramped up sharply during 2009 and 2010 despite a sluggish global economy. Low fuel prices are increasing demand today and my guess is that, with U.S. GDP growth now forecast at 5% in 2015, we could see demand for fuels increase by close to 1.5 MMbbl/d this year. The current IEA forecast is for oil demand to increase by 900,000 bbl/d in 2015.

If this plays out, the oil markets will be heading into a significant squeeze in the first half of 2016.

The last extended period of low oil prices was 1985 to 1990. In 1985, when oil prices collapsed similar to what’s happening now, the world had 13 MMbbl/d of spare capacity, with 7 MMbbl/d in Saudi Arabia alone. OPEC was well-positioned to comfortably meet any increase in demand.

Today, just about all of the world’s discretionary spare capacity resides in Saudi Arabia and amounts to an estimated 2 MMbbl/d. Lou Powers, an EPG member and author of “The World Energy Dilemma," has said that Saudi Arabia will have difficulty maintaining production at over 10 MMbbl/d for an extended period. If we do swing to a supply shortage, Saudi Arabia might find itself in the position of needing to run the taps full out for much of 2016. In such an event, the world will be headed right back into an oil shock and we will see much higher oil prices than $100/bbl.

Low oil prices will hurt the unhedged upstream companies, but they will hurt the oilfield services sector the most. I’m expecting the onshore active rig count to drop by 30% by mid-2015. Oil price will need to firm up for several months before the upstream companies commit to higher spending levels. That said, the high quality drillers like Helmerich & Payne (HP), Patterson-UTI Energy (PTEN) and Precision Drilling Corp. (PDS) will be fine since a lot of their high-end rigs will keep working on long-term contracts. By 2016, they will have gained market share.

Remember, North America and deepwater are the only places with meaningful production upside. If crude oil prices move below $60/bbl and stay there for even six months it could prove catastrophic to non-OPEC supply. At some point, OPEC action might become necessary.

“But perhaps not by the Saudis. Russia’s position is comparable to Saudi Arabia’s. Either could cut production by meaningful quantity, but the Russians need the incremental revenue more. Saudi Arabia would be right to argue that any calls for production cuts should be directed to Moscow. OPEC could cut production to prop up prices and increase revenues. But for now, a better strategy [for Saudi Arabia] would be to hang back, deflect criticism, and let events play out. If the Russians are thinking clearly, Moscow will cut first.” - Steven Kopits, the managing director of Princeton Energy Advisors.

The best news for all of us is that Iran might be quite willing to put an end to their nuclear enrichment program a few months from now. I believe this is the real reason for what Saudi Arabia is doing.

Recommended Reading

Baytex Energy Joins Eagle Ford Shale’s Refrac Rally

2024-07-26 - Canadian operator Baytex Energy joins a growing number of E&Ps touting refrac projects in the Eagle Ford Shale.

US Rig Count Makes Biggest Monthly Jump Since November 2022

2024-07-26 - The oil and gas rig count, an early indicator of future output, rose by three to 589 in the week to July 26.

Private Equity Looks for Minerals Exit

2024-07-26 - Private equity firms have become adroit at finding the best mineral and royalties acreage; the trick is to get public markets to pay more attention.

BP and NGC Sign E&P Deal for Offshore Venezuelan Cocuina Field

2024-07-26 - BP and NGC signed a 20-year agreement to develop Venezuela’s Cocuina offshore gas field, part of the Manakin-Cocuina cross border maritime field between Venezuela and Trinidad and Tobago.

Nabors’ High-spec Rigs Help Keep Lower 48 Revenue Stable in 2Q

2024-07-25 - Nabors’ second quarter EBITDA was down 1% quarter-over-quarter but the company sees signs of increased drilling activity in international markets the second half of the year.