W&T reported a full year 2023 net income of $15.6 million, but suffered an adjusted net loss of $21.7 million. (Source: W&T Offshore)

It takes money to make money—at least that’s what W&T Offshore is hoping for.

During fourth-quarter 2023, W&T performed four workovers and three recompletions, leading to more downtime than originally anticipated. The unplanned downtime, combined with a natural decline in production and a series of acquisitions, led W&T to experience a loss for the quarter.

The company says the acquisitions will pay off. In September, W&T purchased working interests in eight shallow Gulf of Mexico (GoM) fields with $27 million in cash on hand. In January 2024, they purchased 100% working interest in six more shallow GoM fields from Cox Operating using $72 million of cash on hand. The deal added 18.7 MMbbl of proved reserves.

“With over 40 years of experience integrating acquisitions into our asset base, we have proven that the near-term costs are well worth it to realize the long-term potential of the newly acquired assets to generate cash flow for us for many years to come,” Tracy Krohn, founder, chairman and CEO of W&T Offshore said during the company’s March 6 earnings call.

“We believe the recent acquisitions will help us to offset natural decline and grow production this year,” Krohn added.

W&T reported a full year 2023 net income of $15.6 million, but suffered an adjusted net loss of $21.7 million. In the fourth quarter, the E&P suffered a net loss of $0.4 million and an adjusted net loss of $8.7 million.

But even with some losses in the fourth quarter, W&T recorded its 24th consecutive quarter of positive free cash flow, generating $15.8 million in the quarter. For the full year, W&T achieved $63.3 million in free cash flow. Net cash from operating activities in the fourth quarter was $35.7 million and $115.3 for the entire year. W&T also continued to pay down borrowings, with net debt falling to $217.3 million.

“Over the years, we've created significant value by integrating producing properties acquisitions, but it's not as easy or straightforward as you might think,” Krohn said. “As we look to implement this culture of operational excellence, this can result in production deferrals and increase near-term investment to both bring fields up to our standards and increase production.”

In 2023, W&T delivered 12.7 MMBoe, averaging 34,900 boe/d—down from full year 2022 production of 14.6 MMboe. Fourth-quarter 2023 production hit 3.1 MMboe, also down from the 3.3 MMboe it reached during the previous quarter. Despite numbers being down from former years, Krohn anticipates an uptick in production in 2024.

“For the full year 2024, we expect to average 36,900 barrels of oil equivalent per day at the midpoint, which is about a 6% increase year-over-year. We’ve focused more on acquisitions over the last few years rather than on drilling many new wells,” Krohn said.

Krohn said W&T’s new properties will offset natural decline and grow production in 2024.

Due to its recent acquisitions, W&T appears to be on the right track to reach its 2024 projections.

“Our first quarter lease operating expense is expected to be between $77.5 million and $86 million, which reflects some of the expected inspection and upgrading work at the former Cox facilities as well as some maintenance and repair costs included with that,” Krohn said. “First quarter G&A costs are expected to be between $15 million and $17 million.”

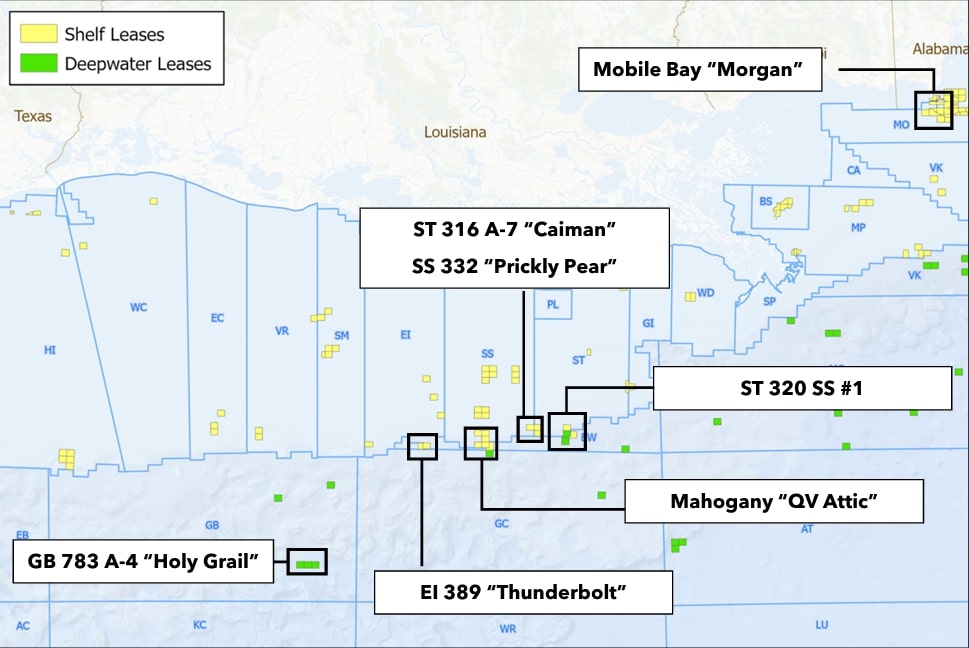

In addition to the projects planned at the recently acquired fields, Krohn also sees a promising future developing some of its undeveloped fields, particularly the Holy Grail Field in the GoM and the Caiman Field. A joint venture could help get W&T’s production numbers in line with guidance as it faces issues with other projects including shut-ins due to the Main Pass pipeline leak and upgrading the Cox acquisitions.

“The former owners left us rather rapidly and didn't really do a whole lot in the way of managing some of the corrosion issues,” Krohn said. “Nothing that I would consider to be hazardous, just some things that needs to be repaired... some of this is pretty simple, but it takes a little bit of time.”

So will the ends justify the means for W&T? Krohn seems to think so.

Recommended Reading

‘Oversupplied’ NatGas Market Aiding Williams’ Storage Business

2024-05-08 - Midstream company Williams saw overall demand growth as heavy gas volumes passed through its network.

Energy Transfer Eyes Draft Environmental Statement for Blue Marlin Project This Quarter

2024-05-09 - Energy Transfer is among several firms vying to build deepwater ports along the Texas Gulf Coast.

Energy Transfer Remains Hungry for M&A, Sees 1Q Oil Volumes Surge

2024-05-09 - Energy Transfer reported record first-quarter crude volumes and expects demand for petrochemicals to continue rising.

Enbridge Plans to Increase Permian Oil Pipeline’s Capacity

2024-05-10 - Midstream company Enbridge announced an open season on the Gray Oak Pipeline for a proposed 120,000 bbl/d expansion and updated its M&A efforts.

Developer Seeks Permit to Send US Gas to Mexico for LNG Exports

2024-05-22 - The project is the latest in a series of developments to convert U.S. gas into LNG and export it from Mexico's Atlantic and Pacific coasts to meet global demand.