The number of high-impact wells drilled globally jumped by 36% to 91 in 2019, according to Westwood Global Energy Group. (Source: Shutterstock.com)

Oil and gas explorers are coming off what could be described as a successful year by some standards, particularly when it comes to high-impact drilling in parts of the world.

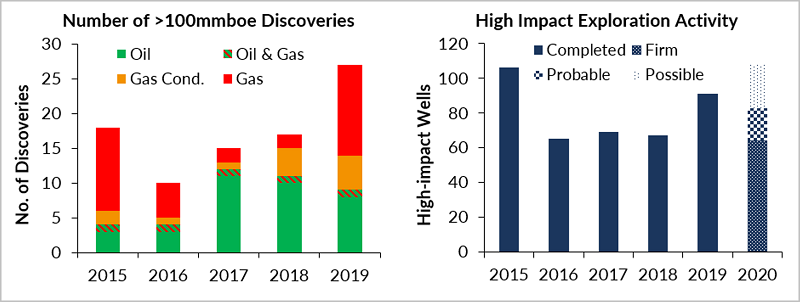

That, as defined by analysts at Westwood Global Energy Group, is wells targeting new plays and prospects potentially holding more than 100 million barrels of oil or 1 trillion cubic feet of natural gas.

The 27 high-impact discoveries made by wells drilled last year collectively pushed discovered commercial volumes to a level not seen since 2015—about 13 billion barrels of oil equivalent (Bboe), according to the U.K.-based energy market research and intelligence firm. The commercial success rate also hit 32%, a 10-year high.

“This level of activity looks likely to be sustained through 2020,” according to Westwood.

The number of high-impact wells drilled globally jumped by 36% last year to 91. The increase in high-impact drilling came despite focus on the energy transition and a move by some oil and gas companies to slow down activity onshore, working to return more cash to investors via higher dividends and stock buybacks while strengthening balance sheets.

“High-impact exploration is dominated by the largest companies much more than say 10 years ago,” Myers told Hart Energy in a statement. However, “Investor appetite for funding higher risk exploration has definitely diminished and the industry relies much more on recycling operating cash flow into exploration than tapping equity markets.”

Attention to high-impact drilling can pave the path toward future growth engines, and falling costs appear to be helping.

“Exploration costs have fallen dramatically and Guyana shows that there is still a big economic prize for the successful explorers,” Myers said. “Energy transition concerns are impacting sentiment, if not yet the well count.”

The report also showed average well costs fell as companies doled out roughly the same amount on drilling—$3.5 billion—as in 2018. Average well costs for high-impact deepwater wells dropped to $50 million in 2019, compared to $130 million in 2015, based on the firm’s analysis.

“This is due to continued lower rig and well services costs and shorter, simpler, smarter wells,” Myers said. “Hard to see well costs falling further in 2020 and in some places, they could edge up on higher rig rates.”

Most of the oil discovered by high-impact drilling efforts were in the Stabroek Block offshore Guyana, according to Westwood. Here, Exxon Mobil Corp. is leading the exploration effort that has led to more than 6 Bboe in estimated recoverable resources. Exxon Mobil and partners Hess Corp. and CNOOC Ltd. made five commercial discoveries on the block in 2019 alone.

The latest was announced in December. The Mako-1 well, located about 10 km (6 miles) southeast of the Liza Field, hit about 50 m (164 ft) of oil-bearing sandstone reservoir.

The analyst pointed out that the commercial success rate was also high—57%—in Africa despite only 14 high-impact wells being drilled. Total’s Brulpadda gas condensate discovery in the Outeniqua Basin offshore South Africa was among the notables. The discovery, announced in February, opened a new petroleum province.

Most of the 3 Bboe-plus discovered in the Africa region was gas, according to the firm.

“In 2020, a similar number of high impact wells are expected spread across 10 countries with potentially six frontier play tests in Guinea Bissau, Kenya, Namibia and Gabon,” according to the report. “Total is testing a new play concept at a well in Block 48, Congo Basin Angola, notable for being the deepest water exploration well ever at over 3,600 m.”

Similar success stories could unfold offshore Guyana, where Exxon Mobil continues drilling prospects, and nearby Suriname, where Apache Corp. and partner Total made a significant discovery.

But high-impact drilling comes with risks and not everyone chalked up wins.

Only two discoveries were made by the 27 high-impact wells drilled in the more mature Northwest Europe region.

“This is a woeful success rate of only 7%. Two wells are still drilling and could yet deliver discoveries, but the low discovery rate should cause pause for thought and the high impact well count should drop in 2020,” the report said.

Commercial discovery hopefuls from high-impact exploration drilling were also elusive in Mexico, where five wells—one still underway—were drilled by international oil companies.

The firm’s analysis showed most of the hydrocarbon resources—77% of the total estimated 13 billion barrels of oil equivalent—found globally was gas. Two of the discoveries were made in Russia. Others were made in Iran, Mauritania, Senegal, Indonesia and Cyprus, according to Westwood.

Looking at 2020, Myers said the firm forecasts between 80 and 90 high-impact wells will be drilled this year with roughly the same, possibly less, spend of about $3.5 billion.

So, what are some of the high-impact wells to watch this year?

Myers’ list includes Royal Dutch Shell Plc’s Chibu deepwater frontier well in the Campeche salt basin offshore Mexico and the Saturno play extension test in Brazil’s presalt Santos Basin along with Exxon Mobil’s Bulletwood play extension test offshore Guyana and Karoon Gas’ frontier Marina well offshore Peru.

Others on the radar include three planned by Total: Mailu well offshore Papua New Guinea (PNG), the frontier Venus well offshore Namibia, Onnjaba offshore Angola and Byblos well offshore Lebanon.

Frontier plays are also set to be tested in Mexico, Australia, New Zealand, PNG and Timor-Leste, the firm said.

Recommended Reading

Offshore Guyana: ‘The Place to Spend Money’

2024-07-09 - Exxon Mobil, Hess and CNOOC are prepared to pump as much as $105 billion into the vast potential of the Stabroek Block.

Endeavor Energy Founder Autry Stephens Dies at 86

2024-08-16 - Stephens created a legacy in the Permian Basin that Endeavor said will continue to shape the future of the company.

Superior Sees Executive Leadership Changes

2024-08-15 - Superior Energy Services’ president, CEO and chairman Brian Moore is retiring, and his roles are to be split between the two people succeeding him.

CEO: Baker Hughes Lands $3.5B in New Contracts in ‘Age of Gas’

2024-07-26 - Baker Hughes revised down its global upstream spending outlook for the year due to “North American softness” with oil activity recovery in second half unlikely to materialize, President and CEO Lorenzo Simonelli said.

Dividends Declared in the Week of July 22

2024-07-25 - Second quarter earnings are underway, and companies are declaring dividends.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.