Drill-to-earn joint ventures have been popular in 2015 as a means to provide private capital to fund drilling costs in the current low commodity price environment. A drill-to-earn joint venture where an E&P company and an investor agree to develop a field on a larger scale is, in essence, just a repackaged version of the age-old farmout with a broader scope. In recent years, this deal structure has been tested by private equity investors, foreign players and nonindustry participants looking for, among other deal drivers, return on investment, commodity exposure, supplies of the commodities themselves, or knowledge about how to development a U.S.-style shale play.

The drill-to-earn JV can provide some attractive benefits, provided the investor keeps an eye on a few of the problem areas inherent in the drilling partnership model.

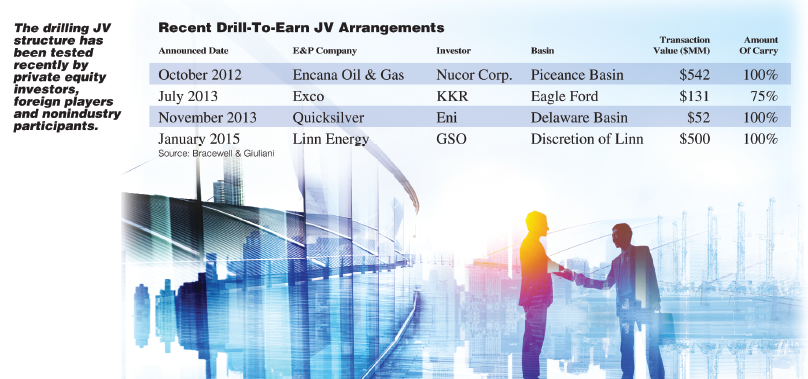

Precedent deals

Recent examples of these JV structures are numerous, including the Encana Oil & Gas/Nucor Corp. Piceance Basin drilling partnership of October 2012, the KKR & Co./Exco Resources Eagle Ford JV of July 2013, the Eni Petroleum/Quicksilver Resources drilling JV in November of 2013 and the Linn Energy/GSO Capital Partners JV targeting undisclosed locations announced in January 2015.

More recently, Legacy Reserves signed a definitive agreement with TPG Special Situations Partners (TSSP) to jointly develop some 6,000 net acres in the Permian, on which Legacy estimates there are more than 150 potential horizontal locations requiring more than $700 million of capital. Similar to Linn's GSO partnership, this structure offers Legacy a way to monetize part of its acreage with minimal capital commitment, allowing the partnership to layer on incremental production over time with a very low capital component.

In the Encana/Nucor transaction, Nucor committed to invest up to $542 million through 2015 and greater amounts in the out years in a pure drilling carry arrangement where Nucor funded the carry costs in exchange for a 49.9% working interest. In that JV arrangement, either party has the right to suspend drilling if gas prices fall below a certain predetermined (undisclosed) threshold and, in December 2013, Nucor temporarily suspended the drilling program as a result of low gas prices.

In July 2013, Exco sold a 50% interest in certain Eagle Ford undeveloped acreage to KKR for $131 million. KKR acquired the 50% working interest in undeveloped properties at closing and Exco agreed to assign half of its remaining 50% working interest to KKR as each well is drilled. Further, KKR agreed to fund and own up to 75% of each well and Exco agreed to fund and own the remaining 25%. Starting in the first quarter of 2015, Exco has the right to purchase wells “in batches” from KKR out of the inventory of wells drilled by the JV.

In the Eni/Quicksilver JV, Eni committed up to $52 million in drilling and seismic costs to earn a 50% working interest in Quicksilver’s Delaware Basin acreage. Eni’s investment was staged with Eni retaining the option to move forward with later stages of the investment. As part of the JV arrangement, Eni and Quicksilver also formed a joint evaluation team to conduct drilling and exploration activities, with Quicksilver named as the operator.

Finally, while just announced in January of this year following execution of a letter of intent, GSO committed to invest up to $500 million over five years to fund drilling programs at locations selected by Linn. GSO agreed to fund 100% of drilling costs associated with new wells in exchange for an 85% working interest in such wells, while Linn will retain a 15% carried working interest in such wells. Upon GSO reaching a 15% internal rate of return on annual groupings of JV-drilled wells, GSO’s interest will be reduced to 5% and Linn’s will be increased to 95%.

Benefits to investors

The drilling JV structure offers clear benefits, similar to other JV constructs. For example, the delayed funding that is central to the macro “farmout” construct allows the investor to delay cash funding further into the future than is possible with other more purchase-oriented upstream investments, including more standard JVs where the investor puts down money up-front for an acreage position with the E&P company. Capital outlays pushing later into the financial model stoke the internal rate of return of the investment. In addition, some investors receive preferential payment of up to 100% of the income until a stated rate of return is achieved (e.g., Linn/GSO). This acceleration of cash inflows increases the certainty of return on investment and provides some assurance to the investor that it will be achieved in the short term, generally consistent with most investors’ goals.

Also benefiting both sides, the JV provides the land-heavy, cash-strapped E&P with a ready source of liquidity and drilling capital and the investor with easy access to shale development in progress and, depending on the structure of the investment, a strong, reasonably low-risk return on investment. Obviously, each partnership will vary in risk, including the risk through the production phase, but stepping into a development that is drill-ready, or close to commencement of drilling, is attractive to the investor in terms of managing the risks.

In addition, in a drilling JV the parties can enter into a tax partnership agreement to allocate the gross income and deductions for federal income tax purposes.

Generally, the gross income from production is allocated to the partner entitled to the related cash proceeds. Intangible drilling costs (IDCs), which are deductible as incurred for federal income tax purposes, typically are allocated to the partner that paid the related cost. Thus, a substantial portion of the investor’s development funding can provide immediate tax deductions, reducing taxable income and phantom income, taxable income recognized without a corresponding receipt of cash or other liquidity to pay the related taxes, which generally is unattractive to investors.

The tax partnership also allows depletion and depreciation deductions with respect to the contributed property interests to be allocated to the partner that purchased and contributed the property or funded its acquisition by the partnership. Thus, the E&Ps may continue to recover the cost of the properties subject to the development plan with the investor for federal income tax purposes.

If, however, the tax partnership terminates early, the partners’ interests in the partnership may not reflect their intended economic interest in the remaining value. Careful tax planning is required to avoid unintended results.

Caveats of the drilling JV

Despite these benefits, it is important when structuring a drill-to-earn JV that the possible detriments to doing these deals be weighed and factored into how the deal is put together, modeled and negotiated on the front end.

For example, the investor typically is not assigned ownership in the leasehold until drilling is imminent or commences (or is completed, in some cases) and then the investor usually receives an assignment on a leasehold, drilling unit or pooled-unit basis. Delaying the assignment can delay the vetting of transfer restrictions binding on the assets (such as consents, preferential purchase rights and maintenance of uniform interest provisions), which can result in delayed drilling if consents are required or preferential rights are triggered.

Best practices dictate that even if the earning or assignment of acreage is delayed, the transfer restrictions should be addressed sooner rather than later to flush out any difficulties that may be lurking in the land instruments.

Further, the investor must protect against commodity prices moving lower during the term of the investment from the levels assumed in the model prepared before the JV commences. However, hedging may not be available based solely on the credit profile of the investor’s special purpose vehicle holding the JV interests.

Recently we have seen this problem stop or slow the progression to closing of some otherwise seemingly good business deals. Parent guaranties or other credit enhancements can be the solution in some cases, but in others (e.g., a private equity-backed structure), credit enhancements to obtain hedging products may be more difficult to navigate.

The shale development economics for a drilling JV deal contain tightly modeled assumptions and parameters that leave little margin of error as operators start drilling. A few bad wells or problems in such operations can poke holes in the economic return of the transaction when compared to the original returns promised at the outset of the JV formation.

While shale development drilling and fracking operations are becoming more efficient as time passes, and market forces demand progress in drilling and development, cost over-runs of any consequence can wreck a JV’s economics quickly when a capped rate of return is agreed to at the front-end of the deal.

In addition, many investors are requiring “off-ramps” to their commitment in the event that certain deal metrics are not met, some of the deal assumptions change materially (e.g. commodity price dislocations occur) or if other exogenous factors impact the deal (i.e., lease expiration).

These off-ramps, while seemingly unlikely at deal execution, can derail the deal in the middle of development and strand the E&P company. Nucor’s drilling partnership was barely a year into development when Nucor exercised its off-ramp and put a halt to development, when the price of natural gas fell below the trigger-point the parties had agreed to.

Finally, for U.S. federal income tax purposes, drilling partnerships holding working interests generally are treated as active businesses holding investments in U.S. real property. Foreign investors, including foreign persons that invest in funds that directly participate in drilling JVs, can recognize operating income from the investment that is subject to U.S. federal income tax, requiring the foreign investor to file a U.S. federal income tax return. Further, if the interest is sold, the gain recognized by the foreign investor is subject to U.S. federal income tax.

Accordingly, foreign investors, or funds with foreign investors, often create a U.S. corporation to hold the interest in the domestic drilling partnership. The foreign investor may be subject to U.S. tax withholding on the dividends paid by the corporation but will not be required to file a U.S. federal income tax return solely because of such investment. Further, if the corporation sells the interest in the drilling JV before liquidating, the foreign investor can avoid U.S. federal income tax on the gain and U.S. tax reporting. However, the U.S. corporation is subject to U.S. federal income tax on its earnings, which can reduce the after-tax return to foreign investors. Tax planning, however, can mitigate the corporate tax on the income.

The drill-to-earn JV model can offer real benefits to both the E&P company in need of capital and the private equity, nonindustry, or foreign investor. However, before entering into any such drilling partnership, each party needs to be aware of the potential risks.

James (J.J.) McAnelly is a partner in Bracewell & Giuliani’s Houston office and co-chair of the oil and gas practice. Elizabeth McGinley is a partner in the firm’s New York office and head of the tax practice.

Recommended Reading

Classic Rock: E&Ps Launch Refracs of Vintage Eagle Ford Wells

2024-06-04 - SilverBow Resources, ConocoPhillips and Devon are among E&Ps seeing positive results from restimulating mature Eagle Ford wells, although no operator is sold on the idea.

Vital Energy’s 57 Miles of Completed Lateral: A Midland Mega-unit

2024-06-06 - Vital Energy’s 20-well unit in southwestern Glasscock County, Texas, is producing some 18,000 bbl/d from some 300,000 feet of horizontal hole — the equivalent of more than two marathons.

Are 3-mile Laterals Worth the Extra Mile?

2024-07-12 - Every additional foot increases production, but it also increases costs.

BPX Expands Its US Shale Game

2024-07-10 - BPX CEO Kyle Koontz delves into development plans in the Permian, Eagle Ford and Haynesville.

Enverus Inventory Rankings: Pinpointing Shale’s Best Remaining Runway

2024-07-11 - The Montney Shale steals the spotlight in Enverus’ play rankings, while the Eagle Ford draws plaudits for its resilience.