Daily oil and gas output is forecasted to decline from shale basins across the Lower 48 in February—except from the mighty Permian Basin, according to new Energy Information Administration figures. (Source: Shutterstock.com)

Oil and natural gas production is expected to drop from most basins across the Lower 48 in February, according to new figures published by the Energy Information Administration (EIA).

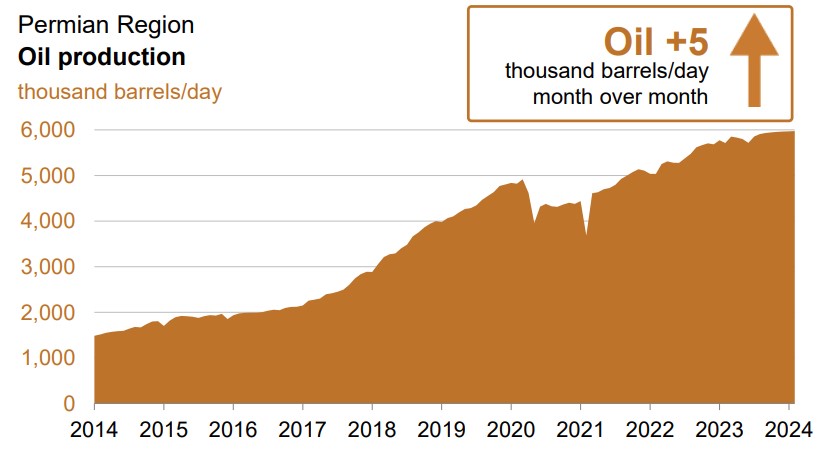

Total monthly crude oil volumes are expected to drop by about 2,000 bbl/d from January to February, the EIA said in its latest Drilling Productivity Report released Jan. 16.

Oil output is forecasted to see month-over-month declines from almost every region across the U.S.—save the prolific Permian Basin.

Eagle Ford Shale crude production is expected to fall by around 2,000 bbl/d in February per the EIA; the Bakken, the Anadarko Basin and the Rockies are each expected to see their respective oil production fall by around 1,000 bbl/d.

But those declines are expected to be offset by gains in the Permian, the nation’s top oil-producing region: Permian crude volumes will grow by around 5,000 bbl/d next month, according to EIA.

Those incremental barrels would push Permian crude production to a record average of more than 5.97 MMbbl/d, per EIA estimates.

Experts and operators anticipate slower U.S. crude production growth in 2024 compared to last year. E&P EOG Resources, one of the nation’s largest producers, expects U.S. crude output to grow at less than half of last year’s pace as drilling activity in key oil fields slows down.

The U.S. rig count dropped by around 20% last year—mostly due to declines in oil and natural gas prices, higher drilling costs and a preference by E&Ps to return cash to shareholders in lieu of putting cash into the ground.

U.S. oil and gas rigs fell by two to 619 in the week ended Jan. 12, the lowest levels since November 2023, according to data from oilfield services firm Baker Hughes.

RELATED: Dallas Fed Survey: More M&A? Sure, but 2024 Remains Uncertain

Gas glut

Gas producers have seen some short-term demand upside from the arctic weather that froze most of the country beginning Jan. 13. But producers are still contending with low prices and a market oversupplied with gas.

Henry Hub spot gas prices averaged $6.42/MMBtu in 2022 amid a confluence of supply-demand imbalances emerging from the COVID-19 downturn and geopolitical instabilities, including Russia’s invasion of Ukraine.

Gas producers raised output, chased high prices and raked in outsized profits. But instead of the structural shortages the global market saw in 2022, today the market is glutted with too much gas.

Relatively flat consumption of gas by the electric power sector and persistently high storage inventories are factors that continue to weigh on natural gas pricing, the EIA reported in its most recent Short-Term Energy Outlook.

The EIA expects Henry Hub spot prices to average under $3/MMBtu in both 2024 and 2025.

The oversupplied market and lackluster prices are being reflected in gas-producing regions around the Lower 48. Total gas output is expected to fall by an average 187 MMcf/d from January to February.

Gas volumes from Appalachia—the nation’s top gas-producing region—are anticipated to fall by 159 MMcf/d over the month.

Output declines are also expected in the Haynesville Shale (-88 MMcf/d), the Eagle Ford (-46 MMcf/d) and the Anadarko (-27 MMcf/d).

Those declines are expected to be offset by additional volumes of gas associated with drilling new oil wells.

Permian associated gas output will rise by around 122 MMcf/d over the month; Bakken gas volumes will also grow by 10 MMcf/d in February, per EIA estimates.

RELATED: Arctic Vortex Pumps Up Natural Gas Demand, But It Won’t Last

Recommended Reading

CEO: Baker Hughes Lands $3.5B in New Contracts in ‘Age of Gas’

2024-07-26 - Baker Hughes revised down its global upstream spending outlook for the year due to “North American softness” with oil activity recovery in second half unlikely to materialize, President and CEO Lorenzo Simonelli said.

Pemex Hits Debt Target, Struggles to Reverse Production Declines

2024-07-26 - Pemex achieved its long-term debt target, which aimed to gets its financial obligations below the $100 billion, while struggling to halt production declines.

Dividends Declared in the Week of July 22

2024-07-25 - Second quarter earnings are underway, and companies are declaring dividends.

NextDecade Appoints Former Exxon Mobil Executive Tarik Skeik as COO

2024-07-25 - Tarik Skeik will take up NextDecade's COO reins roughly two months after the company disclosed it had doubts about remaining a “going concern.”

Freeport LNG Parent Receives Junk-level Credit Score From Fitch

2024-07-25 - Credit-rating firm Fitch Ratings cited the 2 Bcf/d Texas plant’s frequent downtimes among the factors leading to lowering Freeport LNG Investments LLLP’s credit grade on July 25.