The $2.8 billion sale to Canadian Natural Resources achieves a “clean and timely exit from Canada” for Devon, says CEO Dave Hager in a statement. (Source: Shutterstock.com)

[Editor's note: This story was updated at 1:52 p.m. CDT May 29.]

Devon Energy Corp. on May 29 announced an agreement to sell its Canadian business officially kicking off the Oklahoma City-based independent energy company’s transformation.

Calgary, Alberta-based Canadian Natural Resources Ltd. agreed to buy Devon’s Canadian assets for $2.8 billion (C$3.8 billion). Devon will use proceeds from the sale, expected to close during the second quarter, to pay down debt, which is consistent with the company’s previously announced “New Devon” corporate restructuring plan, said John Aschenbeck, senior analyst with Seaport Global Securities LLC.

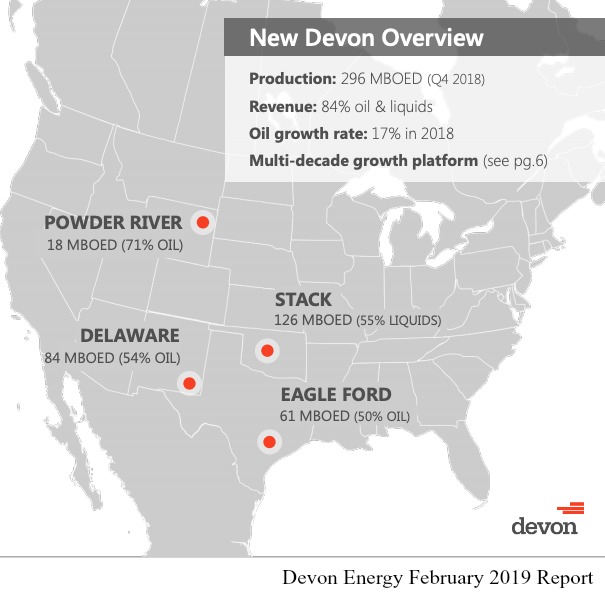

Earlier this year, Devon set out to transform itself into a high-return U.S. oil growth business, which included the possible sale or spin-off of its Canadian and Barnett Shale assets. The end result, core of the core positions in these four basins: the Permian’s Delaware Basin, Stack play, Powder River Basin and Eagle Ford Shale.

Earlier this year, Devon set out to transform itself into a high-return U.S. oil growth business, which included the possible sale or spin-off of its Canadian and Barnett Shale assets. The end result, core of the core positions in these four basins: the Permian’s Delaware Basin, Stack play, Powder River Basin and Eagle Ford Shale.

RELATED: Devon Sharpens Focus On US Unconventionals

“The sale of Canada is an important step in executing Devon’s transformation to a U.S. oil growth business,” Dave Hager, president and CEO of Devon, said in a statement on May 29. “This transaction creates value for our shareholders by achieving a clean and timely exit from Canada, while accelerating efforts to focus exclusively on our high-return U.S. oil portfolio.”

Devon’s Canadian asset portfolio consists of heavy oil assets principally located in the province of Alberta, with net production averaging 113,000 barrels of oil equivalent in first-quarter 2019. At year-end 2018, proved reserves associated with the properties amounted to roughly 409 million barrels of oil. Field-level cash flow accompanying Devon’s Canadian assets, which excludes overhead costs, totaled $236 million in 2018.

According to Hager, Devon built its position in Canada focused in the Athabasca oil sands in northeast Alberta for the past two decades.

Aschenbeck views the sale as a positive for Devon, describing it as “pulling off a sizable transaction at a favorable price, which many investors questioned the viability of.”

“For context, the assets produced 44% of [Devon’s] total oil volumes in first-quarter 2019 and the C$3.8 billion in proceeds are meaningfully above the roughly C$2.7 billion estimate in our model,” he said in a research note on May 29.

Moody's Vice President Amol Joshi said the sale of Devon’s Canadian heavy oil business will sharpen its focus on U.S. unconventional assets

“The Canada sale removes uncertainty regarding volatile Canadian oil differentials and adds to existing cash balances, while the credit impact will largely depend on the quantum of debt reduction,” Joshi said in an emailed statement on May 29.

Though, Joshi noted Devon’s scale will shrink over 20% in terms of production and proved reserves as a result of the sale.

Wood Mackenzie analysts also pointed out that Devon will now drop from the 49th largest producer in the world to the 56th. In comparison, the acquisition of Devon’s Canadian assets will boost Canadian Natural Resources’ ranking to the 25th.

Canadian Natural Rising

The May 29 Devon deal marks Canadian Natural Resources’ seventh major acquisition since 2014 beginning with its purchase of Devon’s Canadian conventional assets for C$3.1 billion (US$2.8 billion). The company also added other gas-weighted conventional properties from Apache Corp. and EOG Resources Inc. that same year.

Other acquisitions include the multibillion-dollar acquisition into the Athabasca Oil Sands Project from Royal Dutch Shell Plc and Marathon Oil Corp. plus the purchase of Cenovus Energy Ltd.’s Pelican Lake asset, all occurring in 2017.

RELATED:

Shell Discards Canadian Oil Sands In $8.5 Billion Deal

Marathon’s $3.6 Billion A&D Swaps Oil Sands For Delaware Pay Dirt

Throughout its buying spree, Canadian Natural Resources has remained committed to heavy oil, according to Stephen Kallir, senior analyst at WoodMac, who also noted the transactions continue a trend of Canadian-domiciled consolidation.

“Canadian Natural Resources is Canada’s largest producer, which has come from a mix of organic growth and opportunistic acquisitions,” Kallir said in an emailed statement on May 29. “Pro forma production will be 1.198 billion barrels of oil equivalent per day. In context, this is slightly less than all of India and more than Colombia.”

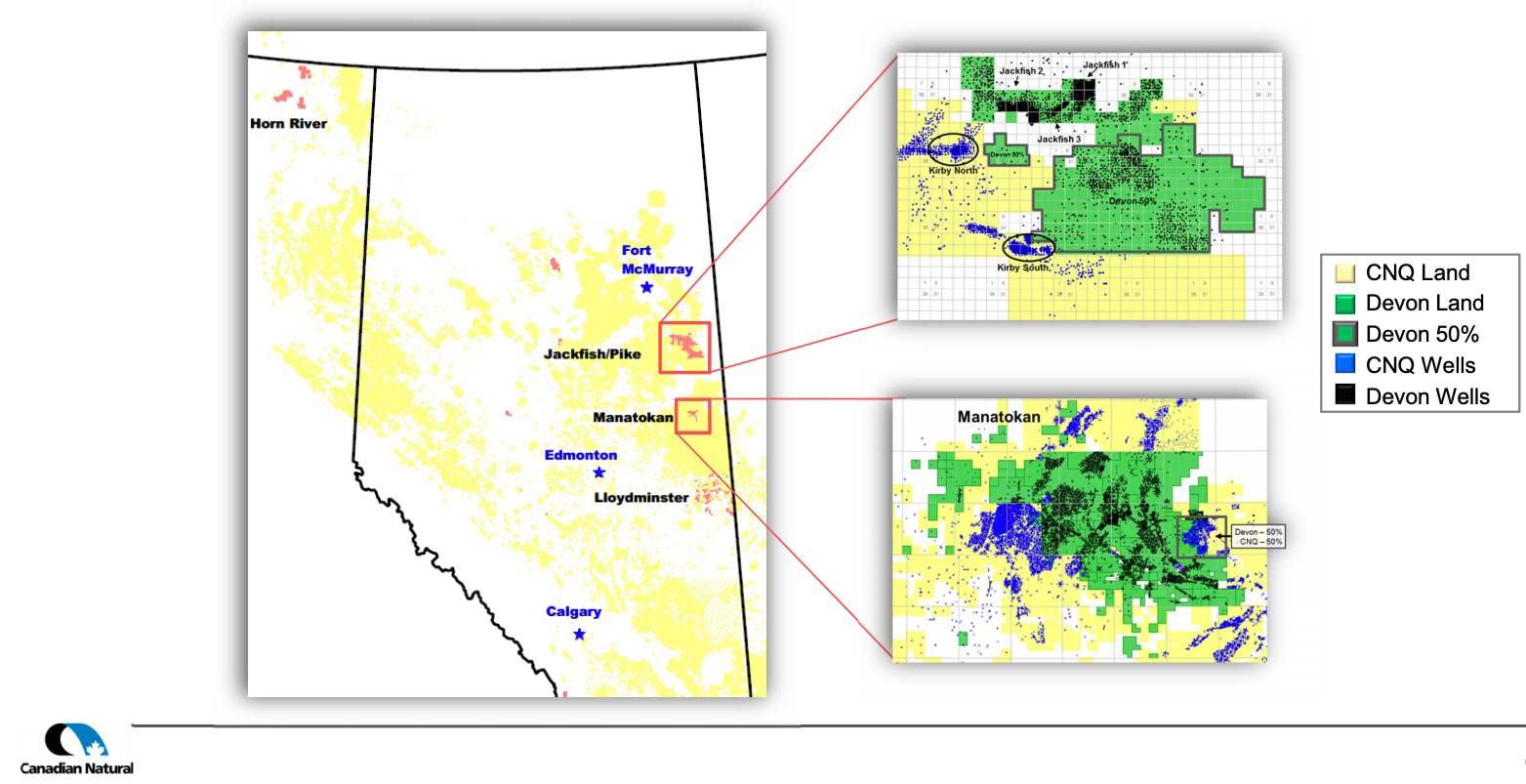

Canadian Natural Resources’ recent purchase from Devon will include 108,000 barrels per day (bbl/d) of oil Jackfish oil sands project. The remainder includes primary heavy oil production of 20,000 bbl/d in Alberta, the undeveloped Pike oil sands lease and Devon’s Horn River and Liard positions.

The Jackfish assets comprise about 88% of the $3.7 billion valuation WoodMac estimated for the transaction after taking into account the subsequent corporate effects of the deal.

(Source: Canadian Natural resources Ltd. May 29 Investor Presentation)

Also notable, Devon’s Canadian land and production are within the company's core areas, which Canadian Natural President Tim McKay said provides the opportunity to add value through synergies.

“These high-quality assets complement our existing asset base and provide further balance to our production profile, while not increasing the need for incremental market access out of western Canada, as it is already existing production,” McKay said in a statement on May 29.

McKay added the company is targeting synergies of C$135 million, which analysts with Tudor, Pickering, Holt & Co. (TPH) said could include facility consolidation, operating and marketing efficiencies as well as likely G&A reductions over time.

Overall, the TPH analysts view the deal as a modest positive for Canadian Natural Resources today as positive impacts from a financial perspective outweigh near-term concerns of incremental bitumen exposure.

“While we see the deal as positive with the transaction screening well from a numbers perspective, investors who have not been fans of the story as a result of limited near-term marketing plans (lack of material rail takeaway plans, for eg.) could continue to struggle in that regard with [Devon’s] assets adding incremental bitumen production without a material plan for egress,” the TPH analysts said in a research note on May 29.

Canadian Natural Resources plans to fund the acquisition of Devon’s assets through a new C$3.25 billion committed term facility provided by TD Securities as sole underwriter and book-runner. TD Securities also acted as financial adviser to the company on the transaction.

J.P. Morgan Securities LLC was lead financial adviser to Devon on the Canada transaction. Goldman Sachs also acted as a financial adviser.

Devon said it continues to advance the divestiture process for its Barnett Shale gas assets in North Texas, which would complete the company’s targeted transformation. Data rooms for the Barnett assets will open in the second quarter and the company expects to exit the assets by the end of 2019.

Emily Patsy can be reached at epatsy@hartenergy.com.

Recommended Reading

US Drillers Cut Oil, Gas Rigs for Fifth Week in Six, Baker Hughes Says

2024-09-20 - U.S. energy firms this week resumed cutting the number of oil and natural gas rigs after adding rigs last week.

Western Haynesville Wildcats’ Output Up as Comstock Loosens Chokes

2024-09-19 - Comstock Resources reported this summer that it is gaining a better understanding of the formations’ pressure regime and how best to produce its “Waynesville” wells.

August Well Permits Rebound in August, led by the Permian Basin

2024-09-18 - Analysis by Evercore ISI shows approved well permits in the Permian Basin, Marcellus and Eagle Ford shales and the Bakken were up month-over-month and compared to 2023.

Kolibri Global Drills First Three SCOOP Wells in Tishomingo Field

2024-09-18 - Kolibri Global Energy reported drilling the three wells in an average 14 days, beating its estimated 20-day drilling schedule.

Permian Resources Closes $820MM Bolt-on of Oxy’s Delaware Assets

2024-09-17 - The Permian Resources acquisition includes about 29,500 net acres, 9,900 net royalty acres and average production of 15,000 boe/d from Occidental Petroleum’s assets in Reeves County, Texas.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.