Crescent Energy Co. on March 30 closed its acquisition of Uinta Basin assets in Utah previously owned by EP Energy for $690 million—several hundred million dollars less than originally announced.

“We are excited to close this highly accretive transaction and expand our Rockies position,” Crescent CEO David Rockecharlie commented in a company release.

Houston-based Crescent Energy had previously announced the agreement in February to acquire the Uinta Basin assets in an all-cash transaction from Verdun Oil Co. II LLC, an EnCap Investments LP-backed firm formed in 2015. At the time of the transaction’s announcement, the company said total cash consideration was approximately $815 million.

“The Uinta transaction clearly demonstrates Crescent’s competitive strengths and ability to deliver shareholder value through accretive acquisitions,” Crescent Chairman John Goff said in the release on March 30.

“We continue to see significant opportunity in today’s market to create long-term value for our shareholders through consolidation,” Goff added.

The Uinta transaction was funded on Crescent’s revolving credit facility. At closing, Crescent’s lenders increased the borrowing base under the credit facility to $1.8 billion with an elected commitment amount of $1.3 billion, an increase of $600 million from the prior elected commitment amount of $700 million.

“We were able to acquire these assets at a compelling valuation while maintaining our financial strength and flexibility,” Rockecharlie also said. “The transaction adds significant cash flow and a multiyear inventory of high-quality oil-weighted undeveloped locations to our existing asset base.”

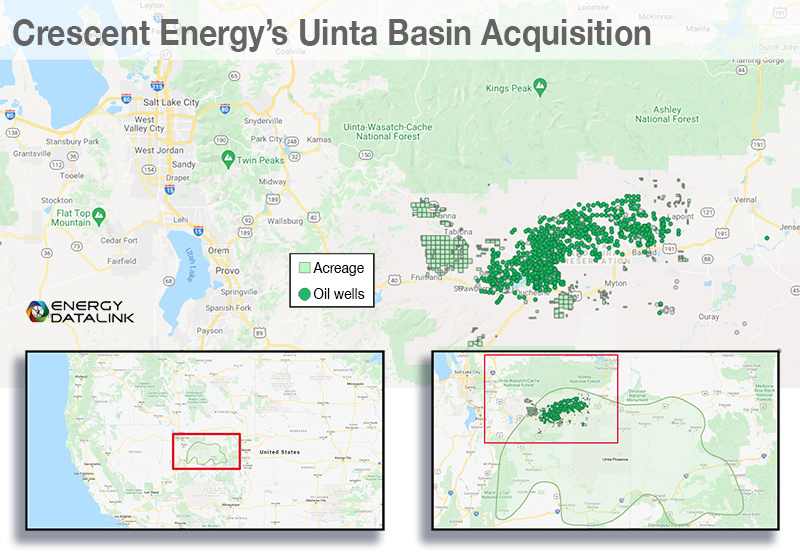

The Uinta acquisition included approximately 145,000 contiguous net acres in Utah producing about 30,000 boe/d, roughly 65% oil. EP Energy had previously owned the assets, according to the Crescent Energy release on Feb. 16.

In August 2021, EnCap Investments had agreed to take over EP Energy’s assets in the Eagle Ford and Uinta basins in a $1.5 billion deal, less than a year after EP Energy emerged from a bankruptcy process that handed control to its creditors.

However, U.S. antitrust regulators had threatened to block EnCap’s takeover of the EP Energy assets, citing concerns about the private equity firm’s dominance in the Uinta shale play.

On March 25, Reuters reported that the U.S. Federal Trade Commission (FTC) approved EnCap’s $1.5 billion takeover of EP Energy on the condition that the firm sell EP Energy’s entire Utah oil business.

The FTC said the deal without the sale of the assets in Utah would have left just three significant producers that sell Uinta Basin crude oil to refiners in Salt Lake City, and led to higher prices for consumers, according to the Reuters report.

Crescent Energy formed in December through the all-stock combination of Contango Oil & Gas with a KKR-backed team. The company, which remains partnered with KKR, currently operates a portfolio of assets across the Lower 48 with Contango as its operating subsidiary.

Following closing the Uinta acquisition, Crescent Energy plans to operate two rigs on the Uinta assets for the remainder of the year.

The company also reiterated on March 30 its previously announced 2022 capital investment plan as well as production and cost guidance. The $600 million-$700 million 2022 capital program is allocated 80%-85% to its operated assets in the Eagle Ford and Uinta basins.

Including contribution from the acquired Uinta assets, Crescent’s pro forma year-end 2021 proved reserves totaled 598 million boe, of which 83% were proved developed and 55% were liquids, and proved PV-10 was $6.2 billion utilizing SEC pricing. The first year decline rate of Crescent’s proved developed producing reserves is 22%, based on production type curves used in the company’s third party reserve reports.

Consistent with its risk management practices, the Company added additional oil hedges in conjunction with the Uinta transaction. Inclusive of expected Uinta volumes, Crescent now has derivatives in place on approximately 60% of expected 2022 total production.

Recommended Reading

Gulfport Energy to Offer $500MM Senior Notes Due 2029

2024-09-03 - Gulfport Energy Corp. also commenced a tender offer to purchase for cash its 8.0% senior notes due 2026.

ONEOK Offers $7B in Notes to Fund EnLink, Medallion Midstream Deals

2024-09-11 - ONEOK intends to use the proceeds to fund its previously announced acquisition of Global Infrastructure Partners’ interest in midstream companies EnLink and Medallion.

Kosmos to Repay Debt with $500MM Senior Notes Offer

2024-09-11 - Kosmos Energy’s offering will be used to fund a portion of its 7.125% senior notes due 2026, 7.750% senior notes due 2027 and 7.500% senior notes due 2028.

Upstream, Midstream Dividends Declared in the Week of July 8, 2024

2024-07-11 - Here is a selection of upstream and midstream dividends declared in the week of July 8.

Solaris Stock Jumps 40% On $200MM Acquisition of Distributed Power Provider

2024-07-11 - With the acquisition of distributed power provider Mobile Energy Rentals, oilfield services player Solaris sees opportunity to grow in industries outside of the oil patch—data centers, in particular.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.