A natural gas pad in Jefferson County, Ohio, where Gulfport Energy has operations. (Source: Shutterstock)

Is Gulfport the GameStop of E&P stocks? The rocket-like trajectory of GPOR’s share-price growth begs the question.

But analysts say investors have latched on to a stock that, for a variety of reasons, has legitimate potential upside.

Shares for Oklahoma City-based Gulfport Energy massively outperformed market peers over the past year—and analysts think the natural gas-weighted name has even more upside in 2024.

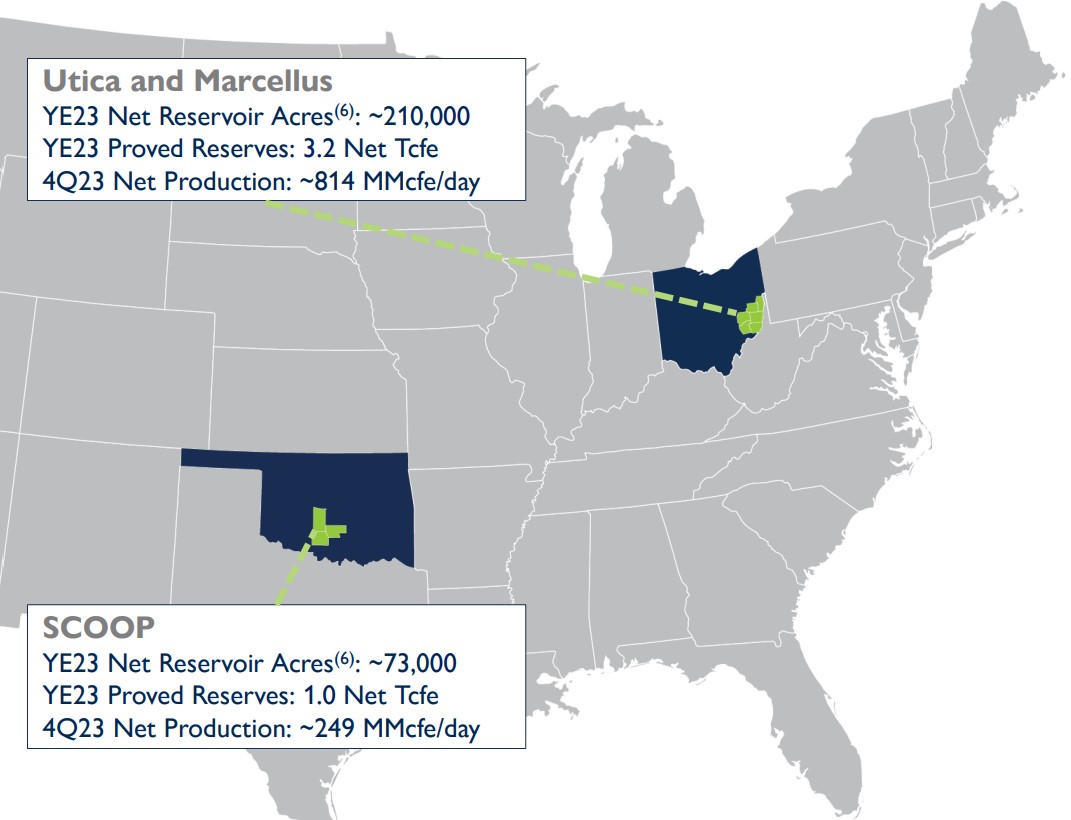

Gulfport Energy has a large footprint in Ohio, where the company holds around 210,000 net acres across the Utica and Marcellus shales. Gulfport also has around 73,000 net acres in the SCOOP play in Oklahoma.

Gulfport’s stock price has risen more than 115% since the end of last February. The S&P XOP index, which includes some of the oil and gas E&P sector’s top names, grew by less than 5% over the same period.

And Gulfport shares have also outperformed other gas-weighted peers in Appalachia, including CNX Resources (up ~36% year-over-year), Southwestern Energy (~31% YOY), Range Resources (~17% YOY) and Antero Resources (down ~2% YOY).

Shares for Appalachia giant EQT Corp. rose around 11% over the same period. EOG Resources, which is testing wells in oil-rich fairways of the Ohio Utica, saw its stock price grow around 1% over the past year.

Analysts say there are a myriad factors fueling Gulfport’s stock price tear, all of which are resonating with the current oil and gas commodity price cycle.

Truist Securities Energy Research Analyst Bertrand Donnes summed it up succinctly for Hart Energy: Gulfport is the cheapest gas name, has a stable program with incremental improvements and is poised to participate in M&A transactions.

The company’s total net production averaged 1.06 Bcfe/d during the fourth quarter, Gulfport reported Feb. 27 after markets closed.

RELATED

Gushing, Ohio: EOG Joins Ascent, Encino in Top Oil Wells

Still undervalued?

Despite massively outperforming the market and its peers, Gulfport is still underappreciated by the broader investment community, analysts said.

Price targets for the ticker are ranging between approximately $170/share and $190/share; GPOR closed up slightly at $142.26/share on Feb. 28.

In addition to being heavily discounted by the market, Gulfport is also delivering top-tier free cash flow yield—even through the current cycle of severely depressed natural gas prices.

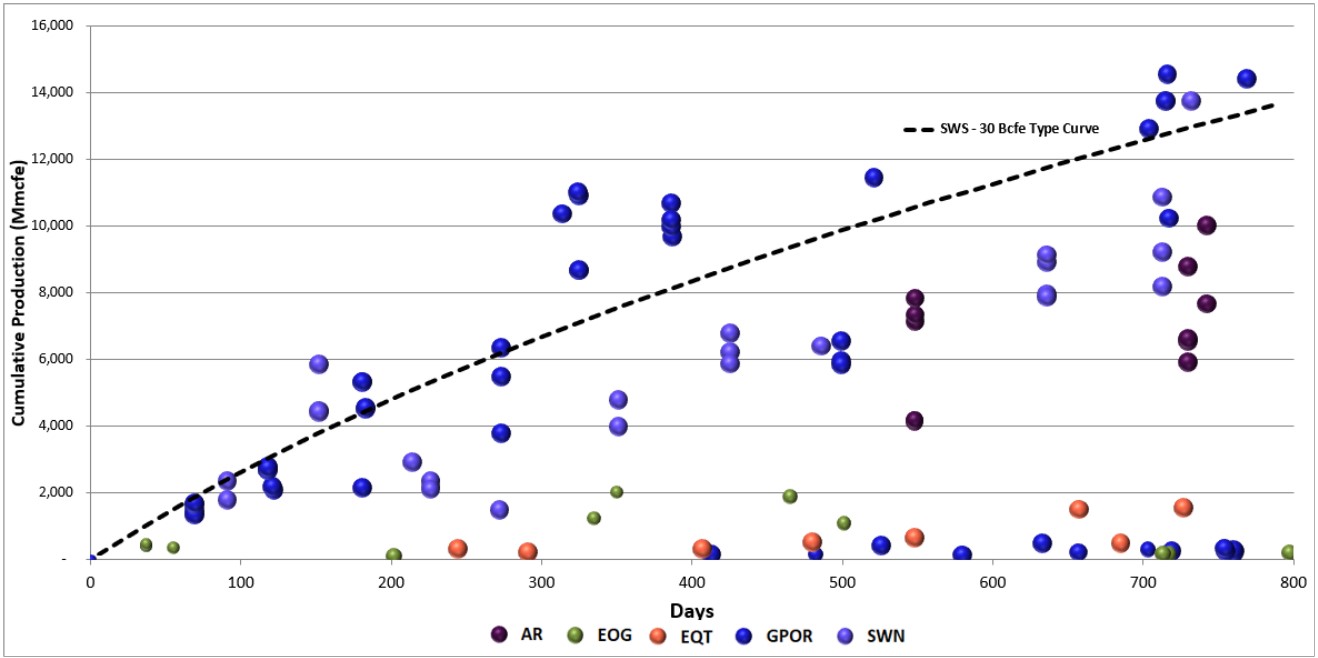

That’s because Gulfport is drilling some of the best wells in the Utica, according to a Siebert Williams Shank analysis of Ohio state regulatory data.

NOTE: Bubble size represents % wet gas

Gulfport is also slashing drilling costs by optimizing well spacing and enhancing stimulation techniques—resulting in longer production plateau periods, shallower declines and improved recoveries, according to Siebert Williams Shank Managing Director Gabriele Sorbara.

Gulfport has targeted total 2024 spending to come in between $380 million and $420 million, a 10% decrease compared to 2023.

The reduced capex requirements give Gulfport “an impressive free cash flow profile,” which is set to generate between 80% and 125% of the E&P’s entire market value over the next five years—with Henry Hub prices between $3.50/Mcf to $4/Mcf— Sorbara said.

“[Gulfport] has fine-tuned its capital program to run a much more efficient program, shaving costs and managing production levels away from the more volatile ups and downs in the past, which is exactly what investors want from a small cap,” Truist’s Donnes said.

“Essentially, don’t mess anything up and you will see multiple appreciation,” he said.

As Gulfport’s gassy assets spit out robust free cash flow, the company will continue to deploy nearly all of it into share buybacks this year.

Gulfport returned substantially all full year adjusted free cash flow, excluding discretionary acreage acquisitions, to shareholders in 2023 by repurchasing 1.5 million shares for $148.9 million, the company said.

RELATED

E&Ps’ Rich Cash Flows Obscuring Critically Needed Capex Investment

Eyes on LNG, M&A

An eventual uptick in natural gas prices, and an uptick in upstream M&A activity, are also factors fueling the fiery growth in GPOR’s stock price.

U.S. natural gas producers have weathered through a prolonged period of low commodity prices due to lower-than-expected demand, a mild winter and overfilled storage inventories.

But most gas producers, by and large, expect to see higher prices return later this year and into 2025 as a wave of new LNG export terminals come online along the Gulf Coast.

Gas investors really aren’t concerned with near-term cash flows right now, Donnes said; the market has seen a drastic downward revision in natural gas prices, while gas-weighted equities have held in line just fine.

“Instead, sentiment is driving stock performance and investors are looking for the cheapest way to play the “eventual” return to high gas prices, which put GPOR right in the crosshairs as the cheapest name in the group,” he said.

Investors also want in on GPOR shares sooner than later because of the current wave of consolidation sweeping across the U.S. upstream sector.

Truist does not believe Gulfport will exist in its current position in the long term. Gulfport is incentivized by market valuations—with the larger-cap names receiving higher valuations—to grow in scale.

“While [Gulfport’s] organic growth is admirable, it will likely take a transformational transaction to achieve the scale investors want, which has investors wanting to own the name headed into a change in scale,” Donnes said.

RELATED

Which Haynesville E&Ps Might Bid for Tellurian’s Upstream Assets?

Recommended Reading

BKV Prices IPO at $270MM Nearly Two Years After First Filing

2024-09-25 - BKV Corp. priced its common shares at $18 each after and will begin trading on Sept. 26, about two years after the Denver company first filed for an IPO.

Oil, Gas Completions Company Covenant Testing Rebrands as One X

2024-09-25 - Covenant Testing said the name change to One X is meant to bring awareness to the company’s “comprehensive, end-to-end solutions for our clients.”

Mach to Sell Additional Common Units to Fund A&D

2024-09-25 - Mach Natural Resources announced that the underwriters of its public offering of 7.27 million units have exercised an option to purchase an additional 1 million common units at $16.50 per unit.

Trafigura Appoints Holtum to CEO, Weir Appointed Chairman

2024-09-24 - Richard Holtum will assume the CEO position on Jan. 1, 2025, and current CEO Jeremy Weir will assume his new position as chairman of the board.

Diamondback to Sell $2.2B in Shares Held by Endeavor Stockholders

2024-09-20 - Diamondback Energy, which closed its $26 billion merger with Endeavor Energy Resources on Sept. 13, said the gross proceeds from the share’s sale will be approximately $2.2 billion.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.