2015 was a year was a year most energy industry players were glad to see disappear in the rearview mir- ror. The downturn that began midway through 2014 continued with com- modity prices falling to nadirs early this year before the current, modest uptick began.

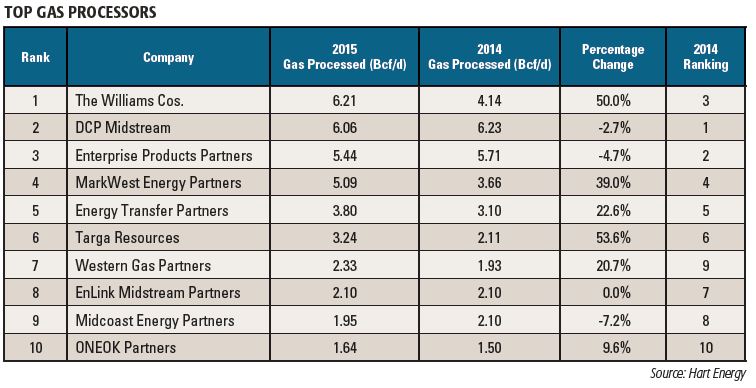

The repercussions of that down- turn—M&A deals and corporate restructurings—impacted the results of the ninth annual rankings of the sector’s largest natural gas processors and top NGL producers by Midstream Business. The Williams Cos. Inc. moved to the top of the gas processor rankings, passing perennial top player DCP Midstream LLC following Williams’ acquisition of Access Midstream Partners, which closed in February 2015.

DCP held the top spot in each of the previous eight surveys.

Williams reported that it processed 6.21 billion cubic feet per day (Bcf/d) in 2015, a 50% increase from the prior year. Meanwhile, DCP’s average volume dropped to 6.06 Bcf/d, a 3% decrease, following several corporate retrench- ments spurred by the downturn. Enterprise Products Partners, ranked No. 2 in the 2014 survey, finished in the show position at 5.44 Bcf/d, a 4.7% decline from the previous year.

MarkWest Energy Partners—also part of a major 2015 acquisition when it was consolidated into Marathon Petroleum’s MPLX LP unit—remained at No. 4, although its gas volume surged to an average 5.09 Bcf/d.

Targa Resources Corp., following the roll-up of its MLP into its parent firm, recorded the largest percentage gain, about 54%, among the survey’s major gas processors. Its average volume surged to 3.24 Bcf/d. Targa’s restructuring followed the model of Kinder Morgan’s 2014 sim- plification of

Three of the top 10 gas processors recorded volume declines from the prior year while one, EnLink Midstream Partners, was flat with a year-to-year average of 2.1 Bcf/d.

The survey’s results are based on all volumes processed and produced at companies’ processing plants and fractionators for the preceding calendar year. Our results are tabulated the fol- lowing year to allow for final accounting of figures provided by companies or published in annual financial reports.

NGL producers

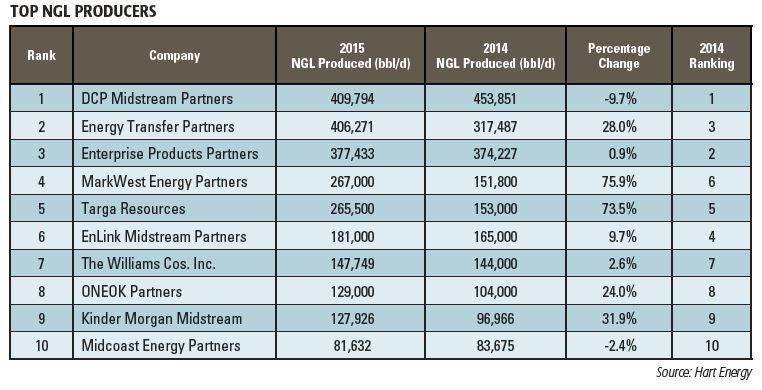

In the gas liquids category, DCP retained its top ranking for the ninth consecutive year at 409,794 barrels per day (bbl/d), although that number marked a nearly 10% drop from 2014. Energy Transfer Partners moved up a notch in the ranking to No. 2 from No. 3 in 2014 with a 28% increase in volumes to 406,271 bbl/d. It passed Enterprise, which reported a rise to 377,433 bbl/d.

MarkWest reported the largest per- centage increase in NGL volumes, climb- ing to 267,000 bbl/d from 151,800 bbl/d in 2014. It rose to the No. 4 spot from No. 6 in the prior year following its combination with MPLX.

Two of the top NGL producers had volume declines while Enterprise marked a slim 1% increase.

Aside from acquisition deals or corporate restructurings, the largest determinant in rankings for both categories was where the players are most active. The Permian Basin remained a comparative hotbed of industry activ- ity—although it, too, showed volume declines from 2014. The Marcellus and Utica plays in Appalachia also had comparatively brisk production, which translated into strong gas processing and NGL volumes.

Looking ahead

Although 2015 was a tough year, the future looks bright for U.S. gas pro- cessors, according to estimates pub- lished by the U.S. Energy Information Administration (EIA) at the end of the third quarter. The agency projects domestic gas production will continue to rise through at least 2040 as devel- opment of the unconventional shale plays continues.

EIA’s reference case for 2020 proj- ects domestic gas production to rise to 82.2 Bcf/d from 79 Bcf/d in 2015— which was an all-time record. Surging gas output in the Appalachian plays, Oklahoma and North Dakota helped lift gas output in 2015.

NGL output will continue to rise, given the gas liquids-rich nature of the shale plays. The EIA projected NGL output in 2017 will rise to 4.33 mil- lion barrels per day (MMbbl/d) from 3.86 MMbbl/d in 2015.

What happens to the ethane market will sway that projection, the agency noted. Slack ethane demand, coupled with surging ethane production from the shale plays, forced most NGL gas processors to reject large volumes of ethane back into residue gas sent into the gas transmission system. The EIA projected that new ethane cracking capacity will begin to come online in 2017, increasing demand.

“Ethane production, which was constrained by lack of demand and low prices in recent years, is expected to reject large volumes of ethane back into residue gas sent into the gas transmission system. The EIA explained. “Forecast natural gas plant ethane production increases by 300,000 bbl/d between 2015 and 2017, accounting for two-thirds

of total … production growth.”

Hart Energy has made every reasonable effort to ensure the veracity of this infor- mation. Neither Hart Energy, Midstream Business nor any other party involved in the presentation of this material will be held liable for any errors or omissions.

Recommended Reading

US Drillers Cut Oil, Gas Rigs for Fifth Week in Six, Baker Hughes Says

2024-09-20 - U.S. energy firms this week resumed cutting the number of oil and natural gas rigs after adding rigs last week.

Western Haynesville Wildcats’ Output Up as Comstock Loosens Chokes

2024-09-19 - Comstock Resources reported this summer that it is gaining a better understanding of the formations’ pressure regime and how best to produce its “Waynesville” wells.

August Well Permits Rebound in August, led by the Permian Basin

2024-09-18 - Analysis by Evercore ISI shows approved well permits in the Permian Basin, Marcellus and Eagle Ford shales and the Bakken were up month-over-month and compared to 2023.

Kolibri Global Drills First Three SCOOP Wells in Tishomingo Field

2024-09-18 - Kolibri Global Energy reported drilling the three wells in an average 14 days, beating its estimated 20-day drilling schedule.

Permian Resources Closes $820MM Bolt-on of Oxy’s Delaware Assets

2024-09-17 - The Permian Resources acquisition includes about 29,500 net acres, 9,900 net royalty acres and average production of 15,000 boe/d from Occidental Petroleum’s assets in Reeves County, Texas.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.