Drilling for oil, as seen here in Oklahoma, must co-exist with alternative sources such as wind for power gen (for charging EVs). Both will be needed to meet energy demand. (Source: Hart Energy)

[Editor's note: A version of this story appears in the July 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

The history of the energy industry can sometimes be ironic. In June 1752, Benjamin Franklin proved lightning’s link to electricity during a thunderstorm in Philadelphia. More than a century later, in August 1859, Col. Edwin Drake launched the U.S. oil age with his well in Titusville, northwest Pennsylvania, and the nascent auto industry soon switched from electric motors to gasoline refined from crude.

difference”

between demand

growth in the West

and in developing

economies, said

Anna Mikulska,

a non-resident

fellow at Rice

University and

senior fellow at

the University of

Pennsylvania’s

Kleinman Center

for Energy Policy.

Today, what’s old is new again, for experts think that in the future, electricity will replace the internal combustion engine for most transportation options. Meanwhile, economists at the Kleinman Center for Energy Policy at the University of Pennsylvania recently published a study looking at oil’s future, comparing the many different projections on when global oil demand will peak.

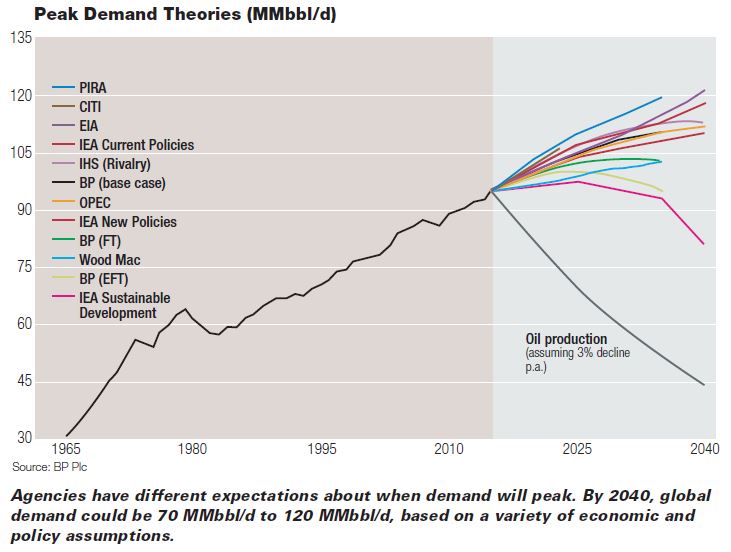

Experts agree: The world is at the start of a Great Energy Transition from oil to other forms of energy. Oil will still be used in 20 or 30 years, but it will account for a smaller percentage of the whole energy mix. The extent of this transition, its timeline and what it could mean for oil producers is a matter of serious debate. Although most sources have two or three scenarios, a general consensus is emerging that global oil demand will peak between 2030 and 2040, certainly by 2050, followed by a plateau and then a long tail.

The International Energy Agency (IEA) is the source most often cited by the majors, academics and others when they look into the crystal ball. In IEA’s sustainable development scenario, “which is a scenario that is fully in line with the Paris Agreement, we think determined policy interventions to address climate change lead to a peak in global oil demand around 2020, at 97 MMbbl/d [million barrels per day].”

IEA revises its scenarios frequently. Another of its sustainable development scenarios postulated that oil demand will peak at a higher level, about 104.7 MMbbl/d, as soon as 2023. Tellingly, the agency said, “Demand peaks in nearly all countries before 2030.”

No one is saying there will not be a peak. The question is when will it occur, and by that time, how much oil will the world still need each day?

The majors are starting to prepare for this transition, given intensifying government mandates and investor pressure to reduce methane emissions and support alternatives like electric vehicles (EVs). Many U.S. independents aren’t so sure. Besides, they’re focused on making money and reducing costs right now, amid a historic bounty of oil production, which could last another 40 years.

A decade ago when people mentioned The Great Energy Transition, they meant the grand shift to natural gas for power generation and land transportation, which conveniently matched up with the shale revolution that unlocked vast U.S. gas reserves and led to LNG exports.

__________________________________________________________________________________________________

RELATED:

“Energy Stocks And The Environment” featured in the June 2019 issue of Oil and Gas Investor

__________________________________________________________________________________________________

Today the definition is changing. When gas prices plummeted, E&Ps refocused on oil, which turned out to be a boon: millions of barrels are being produced in record-setting numbers with amazing financial and geopolitical effects. This newfound oil bounty changed the global oil game.

At the same time it has energized the anti-fossil fuel movement, which is motivated by dire forecasts of weather disasters and recent warnings about millions of species facing extinction. The coming shift away from fossil fuels is going to be as much about government policies and public sentiment, as it is about the availability of alternatives like EVs. The Energy Information Administration estimates 29% of greenhouse gases come from power generation and another 29% come from transportation. These are the two biggest battlegrounds in the energy transition.

Our purpose here is not to debate climate change. What is clear, however, is that the perception around climate change is causing a big stir: Governments and auto manufacturers around the world are setting stricter goals to reduce emissions, if not eliminate the use of fossil fuels altogether. The world is embarking on a low-carbon diet.

As one source pointed out, if oil demand does peak in 20 years, the majors need to study the dynamics of this and make plans; their business is on the line. Then too, a peak doesn’t mean oil demand falls off a cliff. A transition to other fuels will take decades thanks to the huge scale of global energy consumption, so oil needs to be found to meet that demand, not to mention offsetting resource depletion.

“A significant energy transition is underway,” says ExxonMobil Corp., whose website has a large section devoted to its long-term energy outlook. “More electric cars and efficiency improvements in conventional engines will likely lead to a peak in liquid fuels use by the world’s light-duty vehicle fleet by 2030. However, oil will continue to play a leading role in the world’s energy mix, driven by commercial transportation and the chemical industry.”

BP Plc concurs. “Our view is that the world is in an energy transition,” said Mark Finley, BP’s Washington, D.C.-based economist, speaking at the annual Howard Weil energy conference in April. In BP’s latest annual energy outlook, released this past February, the company took a scenario approach, looking at various outcomes to 2040. Back in 2011, BP had predicted oil demand would reach 102 MMbbl/d by 2030—in reality it could reach that level next year or in 2021. It’s already at 100 MMbbl/d now.

While explaining its scenarios for peak demand, the BP outlook also sounded a cautionary note. “Much of the popular debate is centered on when oil demand is likely to peak. A cottage industry of oil executives and industry experts has developed that is trading guesses of when oil demand will peak: 2025, 2035, 2040. This focus on dating the peak in oil demand seems misguided for at least two reasons.

“First, no one knows; the range of uncertainty is huge. Small changes in assumptions about the myriad factors determining oil demand, such as GDP growth or the rate of improvement in vehicle efficiency, can generate very different paths.

“Second, and more importantly, this focus on the expected timing of the peak attaches significance to this point, as if once oil stops growing it is likely to trigger a sharp discontinuity in behavior: oil consumption will start declining dramatically or investment in new oil production will cease.

“Beware soothsayers who say they know when oil demand will peak.”

Wall Street Chimes In

Equity analysts who cover the energy sector also have begun to weigh in on this topic. “Although peak demand is a compelling concept, the likelihood of it happening within the next decade seems highly unlikely, and debatable for the decade beyond that,” said energy analyst Neil Beveridge, in his recent Bernstein Research report on Chinese oil demand, one of the largest single factors that impact every demand scenario.

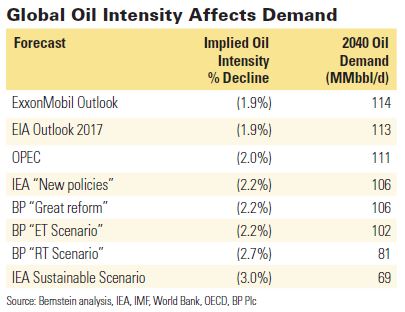

“Longer term, we will reach peak oil demand before we reach peak supply; growth from emerging markets will propel oil demand to nearly 108MMbll/d,” Beveridge wrote. “The secular decline in oil intensity will ultimately cause demand to peak however, but not until after 2030.” Oil intensity is an important metric in every economy. It is the number of barrels of oil needed to move the needle on GDP per capita, taking into account urbanization and technology changes such as use of EVs.

“Oil may be out of favor and facing a crisis of perception,” he said. “But if demand continues to increase, and reinvestment stays low, it seems inescapable that there is at least one more super cycle in the industry to come.”

In April, a Gaffney Cline report said that as the oil and gas industry faces an impending energy transition, it will have to compete or face negative consequences.

“The carbon intensity of oil and gas will be a key metric (the amount of CO2 equivalent emissions per unit of energy produced), which can be used proactively to make informed choices now,” the firm said. “As implementation of carbon solutions and the reductions they achieve will take many years, a lack of timely action could result in higher compliance costs, price discounts for carbon intensive oil and gas, cancellation of supply contracts and even stranded reserves.”

Demand Trends Today

This year global demand will pass the key threshold of 100 MMbbl/d. Most sources estimate that by year-end, it will have risen by another 1.2 to 1.4 MMbbl/d over last year’s level, when demand rose by about 1.3%, to 99.9 MMbbl/d.

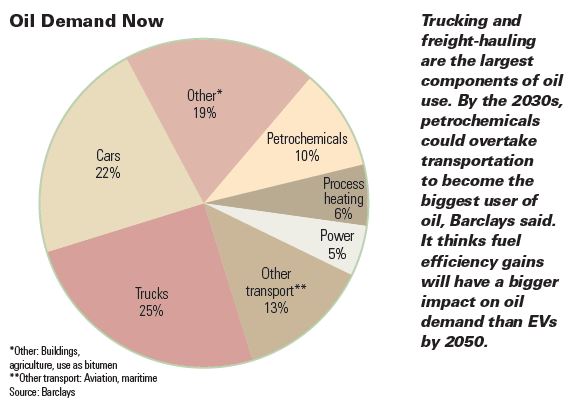

Demand is a function of many factors, chief among them oil prices and GDP growth, with government policies sprinkled in. Projections of the peak rely on dozens of conflicting assumptions about future government mandates, changes in vehicle engines and other technologies, demographics or the number of people driving or traveling by plane, the amount of goods that need to be trucked or shipped in growing economies, and growth in the petrochemical industry vs. an emerging global trend to ban plastics.

For 150 years, demand has increased steadily, most recently averaging a growth pace of at least 1 MMbbl/d annually. That pace may slow down, but growth will still occur, observers say.

Demand grew very fast at times in the past, with different statistics depending on the time period used. It grew 25% between 1980 and 2000 as more economies expanded their middle class. During a tighter time frame of 2000 to 2010, it rose by 12%. When economies in the developing world, especially in China and India, took off, demand climbed by 4.9 MMbbl/d between 2003 and 2006.

All in, global demand has risen about 30% during the past 20 years, but the next 20 are crucial, according to a Barclay’s report on peak demand released in May. “Reliance on oil is to peak in 2030-2035, if countries stick to their low-carbon pledges. Based on current policies, the most likely outcome is that oil demand stagnates out to 2050, as increased use of petrochemicals offsets the electrification of transportation,” the firm said.

Peak Predictions

What of the peak? Everyone has an opinion, but perhaps no group has more at stake than OPEC. This past September, when OPEC released its 2018 World Oil Outlook, it predicted a steady rise in global oil demand, to 111.7 MMbbl/d by 2040, from about 99.2 million in 2018.

is analogous to

changing what

horses are fed

and importing

new fodder,” said

Mark P. Mills,

senior fellow at

The Manhattan

Institute.

Consultancy DNV GL thinks the peak will occur in 2023. Royal Dutch Shell Plc has said by the late 2020s. Crude oil trader Trafigura expects a peak by 2030 and that the shift to EVs and renewables will happen faster than many people think. Equinor’s latest outlook said 2030. BP’s most recent annual energy outlook said the mid-2030s.

Bernstein analyst Neil Beveridge wrote that he expects robust oil demand growth to continue until 2021, with demand peaking between 2030 and 2035.

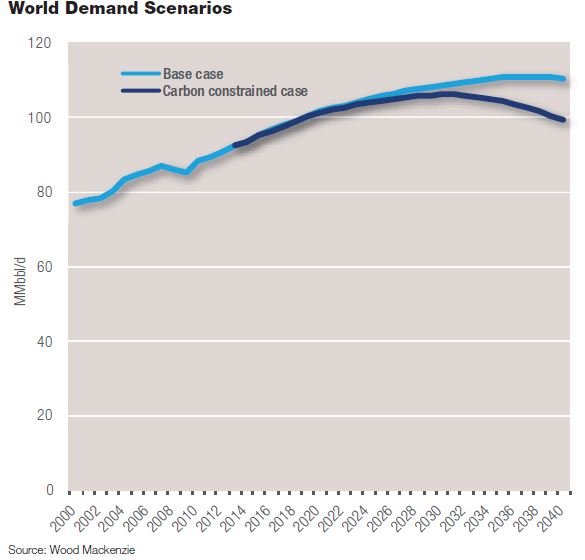

McKinsey & Co.’s latest model foresees a peak in demand growth in the early 2030s, but by 2035, in its base case, E&P companies will still need to add 43 MMbbl/d of new oil production, it said, to offset production declines.

Wood Mackenzie has also studied the topic, pointing to areas where demand will fall and others where it will increase. “Demand for oil in developed countries will revert to a structural decline by 2020, wiping out about 4 MMbbl/d by 2035,” said a WoodMac report.

“In contrast, developing economies will increase their demand for oil by about 16 MMbbl/d by 2035. While transportation demand will flat line around 2030, we forecast continued growth in overall global oil demand supported by the petrochemical sector. Nonetheless, the prospect of peak oil demand is very real.”

Linda Giesecke, research director for WoodMac‘s Americas Refining & Oil Markets unit, put this into perspective. “The good news is peak demand is not going to happen any time soon. We’re now at about 100 MMbbl/d. The bad news is we see a plateau by 2035 or shortly thereafter, at about 111 MMbbl/d, starting to ease off after that,” she told Oil and Gas Investor.

“If we were to look at the trend since 2000 and extend it, we’d be at 125 MMbbl/d, but instead, we project 110 to 111. About 60% of that is for transportation, including trucks, ships and planes. What’s interesting is the growth in transport goes up to maybe 65 MMbbl/d during the next 20 years, whereas petrochemical use grows to 19 MMbbl/d, or by 60%. (That could slow down though as China becomes more mature in its use of plastics).”

In the IEA’s New Policies Scenario (government policies that are already in place as well as those that have been announced, without speculating as to how policy might evolve in the future), oil demand does not peak prior to 2040.

“The amount of oil used for passenger vehicles reaches a peak around the mid-2020s. This occurs despite an 80% expansion in the global car fleet from today to over 2 billion vehicles by 2040. The peak is mainly due to efficiency gains but also because of fuel switching and continued rapid growth in the electric vehicle fleet.

“We project 300 million electric cars on the road by 2040, 4 million electric buses and more than 700 million electric motorcycles. China leads the way in electric mobility: over 40% of the electric cars in the world are in China in 2040, as well as nearly 60% of the electric buses.”

The IEA added that increases from other sectors will keep oil demand on a rising trajectory to 106 MMbbl/d by 2040. Production of petrochemicals is the largest source of growth, adding around 5 MMbbl/d, the agency said. “This is closely followed by rising consumption for trucks (fuel efficiency policies cover over 80% of global light-duty vehicle sales today, but only 50% of global heavy-duty vehicle sales), for aviation and for shipping, despite strong energy efficiency improvements.”

Naturally there are skeptics among all the people looking at peak demand. Mark P. Mills, senior fellow at The Manhattan Institute, a think tank, is one.

“Let’s put this in perspective. Labeling matters; words matter,” he told Oil and Gas Investor. “This Great Energy Transition is like going from horses to cars. If it’s true, you can’t fight it. If it’s not true, the world will find out soon enough. I don’t dispute the rise of alternative fuels, but I do dispute that they would replace oil at scale as a primary fuel source.

“We still use stone, bricks and concrete, all of which date from antiquity, and we do so because they are optimal, not because they are old. Hydrocarbons are, so far, optimal ways to power most of what society needs and wants.

“When the world’s poorest 1 billion people increase their energy use to just 15% of the per-capita level of the developed countries, global energy consumption will rise by the equivalent of adding an entire United States of demand,” he said.

Fundamentally, this debate is about every country’s economy continuing to advance for years to come, with oil demand linked to GDP growth. The trick is these economies must become greener while still being able to move millions of people and tons of goods.

The New Mobility

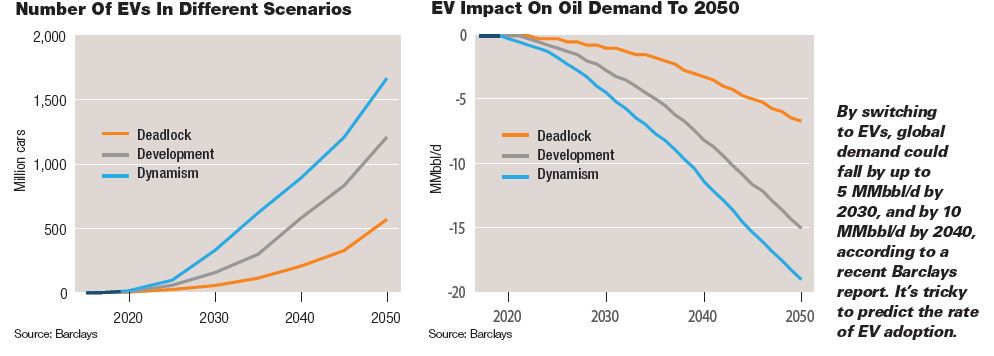

Much of the demand outlook hinges on how many people will drive in the future, and in what kind of vehicle. One IEA scenario said EVs will make up only 20% of car sales by 2040, when the expected 300 million EVs in use would then displace just 3.3 MMbbl/d of oil. In an April Barclay’s report on this topic, analyst Nicholas Potter estimated that if EVs make up a third of the fleet by 2040, that would cut oil demand by 9 MMbbl/d (and, by 3.5 MMbbl/d as soon as 2025).

“Optimists forecast that the number of EVs in the world will rise from today’s nearly 4 million to 400 million in two decades,” said Mills’ report for The Manhattan Institute.

“This sounds counterintuitive, but the numbers are straightforward. There are about 1 billion automobiles today, and they use about 30% of the world’s oil. (Heavy trucks, aviation, petrochemicals, heat, etc. use the rest.) By 2040, there would be an estimated 2 billion cars in the world. Four hundred million EVs would thus amount to 20% of all the cars on the road—which would replace about 6% of petroleum demand,” the report said.

This is an old debate that has been rekindled by new technology. IHS CERAWeek co-chairman Daniel Yergin weighed in on this very topic in his 2011 book, The Quest. He noted that when cars first appeared in the 1890s, most were electric, and Thomas Edison was busy trying to make it so. But in 1893, the first gasoline-powered car was built in the U.S. When oil was discovered in abundance in the early 1900s from Pennsylvania to Texas and Oklahoma, well, the rest is history. Autos with an internal combustion engine won out over electrics—after all, they had a big advantage: they didn’t need to be cranked to get started.

“But the return of the electric car—in this case fueled not only by its battery but by government policies—is restarting the race,” Yergin wrote in The Quest.

“If the electric car proves itself competitive, or at least in some circumstances, that outcome will reshape the energy world. That is not the only competitor. The race is also on to develop biofuels—to ‘grow’ oil rather than drill for it. All this sets a very big question: Can the electric car or biofuels depose petroleum from its position as king of the realm of transportation?

“Of one thing we can be pretty certain: The world’s appetite for energy in the years ahead will grow enormously. The absolute numbers are staggering.”

The global car manufacturing industry is making, or soon will, plenty of EVs. (Today they make up about 2% to 3% of the fleet.) GM, Ford, VW, Mercedes, BMW, Toyota, Kia, Aston-Martin, and many more are getting on board.

Some say the transition away from the internal combustion engine could get nasty. Consumers who love their gasoline-powered cars and trucks can get up in arms as more EVs infiltrate the fleet. The media has reported about irate traditional drivers keying EVs parked at charging stations, or purposefully blocking their access. In places as disparate as Arizona and Quebec, it is now illegal for the driver of a car with an internal combustion engine to park in, or block, an EV parking space. Fines will be imposed on violators.

sees global

demand reach a

plateau in 2035,

starting to ease

off after that, said

Linda Giesecke,

research director,

Americas, refining

and oil markets.

Wood Mackenzie found that by 2035, some 15% to 20% of all miles traveled globally by cars, trucks, buses and bikes will use electric motors instead of gasoline or diesel. “We expect 5 MMbbl/d to be displaced by EVs in 2040, primarily from cars, but we’ve assumed some in the trucking sector,” said WoodMac’s Giesecke.

Experts point to China as the biggest unknown. Bernstein’s Beveridge thinks China’s vehicle fleet will double from 200 million units today to 400 million by 2030, and that will be a net function of car sales minus what he calls “the scrappage rate.” On the other hand, the Chinese are very committed to electric vehicles and are leading the world in terms of manufacturing and adoption of EVs.

“Driving an EV is analogous to changing what horses are fed and importing new fodder,” said Mills. For every problem it solves, another crops up. For one, the U.S. would have to import batteries and battery components, and figure out how to recycle them or safely discard them.

If batteries are used to make electricity, that’s another problem of scale. “Some $200,000 worth of Tesla batteries, which would weigh over 20,000 pounds, are needed to store the energy equivalent of one barrel of oil,” he said in his report.

Still, the impetus toward EVs is gaining momentum. In March, 16 global automakers and seven states announced they are kicking off a multiplatform U.S. campaign, “Drive Change. Drive Electric.” Its purpose is to increase EV use throughout the Northeast. “Transforming mobility requires more than a large numbers of high-quality cars,” said Mitch Bainwol, president and CEO of the Alliance of Automobile Manufacturers, which represents 12 of the automakers backing the campaign.

Some countries are already making headway in their great energy transition. Norway, albeit a small market for vehicles, said that in March 2019, EVs outsold gasoline and diesel models for the first time, accounting for 58.4% of all vehicle sales in that month. Norway’s government has set an ambitious goal to stop selling new gas and diesel passenger cars and vans by 2025.

But demographics cut both ways—more people in the world, but not necessarily more who drive, Mills pointed out.

“The IEA forecast has as much raw net new oil demand growth in the next 20 years as there is oil in the ground. The wildcard for me is not the next big revolution in transportation such as self-driving cars—that won’t reduce demand,” said Mills. “But in 20 years, there will be more people under the age of 16 and more over the age of 75 who don’t drive, than all the rest of the people in the middle who do drive,” he said.

“Also, people who talk about peak demand fail to take into account air taxis or self-flying or other things yet to be invented. If 10% of the population could afford to do that, you’d see a significant increase in oil demand, because after all, it takes more energy to lift something into the air than to move it horizontally on the ground.

“My point here is not to play speculative games … but what engineers may do to create new forms of energy demand is not on anybody’s radar.”

Studying The Studies

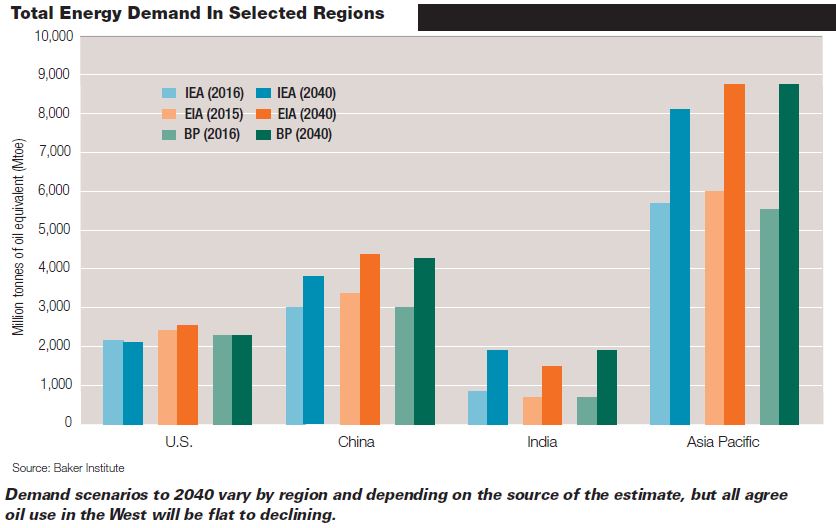

About a year ago, economists at The Baker Institute for Public Policy at Rice University, Houston, analyzed the 20-year demand outlook by comparing data, assumptions and projections from the 2018 versions of the IEA, EIA and BP energy outlooks, these three being the sources most often cited by other experts. They looked at general trends derived from the “business as usual” scenarios in each case.

“When you look at the different outlooks, predicting the future accurately is never going to happen, but it helps us to think about what the trends are and what factors that drive demand are happening now,” said Anna Mikulska, a senior fellow with the Baker Institute and a visiting fellow at the University of Pennsylvania’s Kleinman Center for Energy Policy.

“The one thing we definitely noticed in all the studies is the stark difference between what is happening in the OECD and the more developed economies. It is a story of two worlds,” she told Oil and Gas Investor.

“In the OECD, energy demand is driven by efficiency and using more renewables, whereas in the developing world, they are using more crude oil. Looking out 20 years, you do see the growth in crude demand is not as strong as it was in the past. But growth is most pronounced in India and Southeast Asia. China will overtake the U.S. as the largest consumer of oil but India’s growth rate is now faster.

“We do see growth in demand for oil as a feedstock for petrochemicals.”

Future Demand

One of the most important factors is that the current global population of more than 7 billion is expected to rise to 9 billion by 2040—and all these additional people will inevitably need to use more oil, especially in the rapidly growing economies of the non-OECD or developing countries. Oil use is directly tied to rising GDP.

The world will be hungrier for all forms of energy in the future; primary energy demand is estimated to rise by a third between 2015 and 2040, with the bulk of this increase occurring in the rapidly developing economies. OPEC said oil will remain the fuel with the largest market share through 2040.

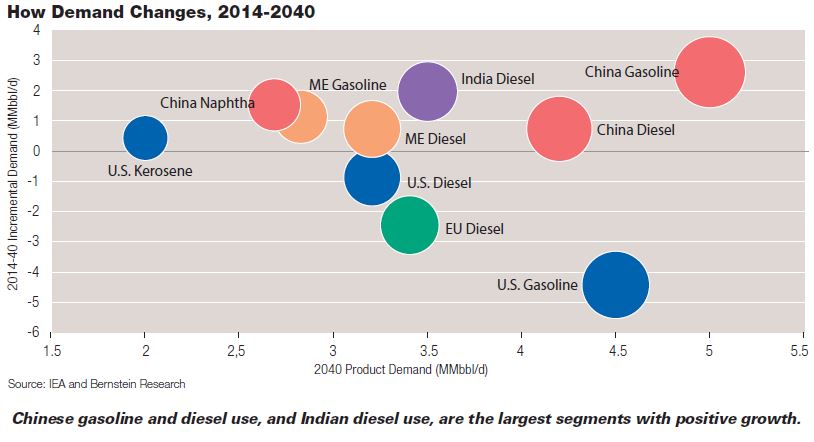

Demand will be fueled by the non-OECD countries as more people enter the middle class and drive and fly, more trucks need to transport increased consumer goods to them, and petrochemical demand increases by 4.5 MMbbl/d to 2040. As night follows day, more plastic means more products to buy, which means more trucks and ships will be moving goods to and from every country.

The IEA and World Bank, among others, peg oil demand in 2040 being as much as 110 MMbbl/d, having increased by an average 1.88 MMbbl/d every five years between 2020 and 2040. During this period India’s usage is predicted to rise 20% from current consumption of about 5 MMbbl/d. Demand in the rest of Southeast Asia (ex-China) is expected to rise 40% from about 4.8 MMbbl/d currently. China will account for about 20 million barrels of that.

Batteries, Utilities And Other Trends

However all these trends play out, getting away from emissions is the goal, regardless of the fuel used. The goal, one source told Oil and Gas Investor, is not to see the end of oil. “I tell my students the goal should not be to replace fossil fuels. It should be to decarbonize those fuels or reduce their emissions,” said Mikulska, who teaches at the University of Pennsylvania. That is where additional research should focus, she said.

To that end, the Environmental Law Institute in Washington, D.C., has published a new book titled, “Legal Pathways to Deep Decarbonization in the United States.” It identifies more than 1,000 options to reduce U.S. greenhouse gases by at least 80% from 1990 levels, by 2050. These legal options involve federal, state and local law, as well as private governance.

Calls for carbon capture and storage are growing louder, a tactic that Occidental Petroleum Corp. CEO Vicki Hollub is promoting for the Permian Basin. Alaska Sen. Lisa Murkowski and West Virginia Sen. Joe Manchin, both from oil producing states, recently introduced a bill asking the Department of Energy to do more on CCS research.

Murkowksi has also introduced a bill asking for more R&D budget for batteries, saying she fears U.S. dependence on lithium imports from adversarial countries, calling this an Achilles heel. Testifying before her Senate committee in February, battery analyst Simon Moores said his group, Benchmark Mineral Intelligence, was tracking 70 “mega” battery factories being built globally—46 of these are in China; just five in the U.S.

Many states have already set ambitious targets to reduce fossil fuel use in electricity generation, and in turn this may affect adoption of EVs as well. New Mexico has declared 50% of its power gen shall be emissions-free by 2030 and 100% will be by 2040. Nevada’s governor signed a bill recently calling for the state’s power to be 50% emissions-free by 2030 and 100% by 2050. California and Hawaii have similarly tough targets.

But even as U.S. utilities are under pressure to reduce their carbon emissions in power gen, they are warming up to the idea of EVs, which will need to be charged overnight, ultimately increasing power demand. Duke Energy Corp., for one, recently asked North Carolina regulators for permission to build $76 million worth of EV chargers, the largest investment by a utility in EV infrastructure in the Southeast so far. Meanwhile, the state’s governor has set a statewide target for EV sales, calling for thousands more zero-emissions vehicles by 2025.

Duke proposes to install almost 2,500 chargers over the next three years. Last year, AEP announced a $10 million incentive program to get 375 charging stations installed throughout its Ohio service area.

Plastics

Oil plays a small role in petrochemical demand compared to natural gas, but in this arena as well, trends could be changing: There is a growing worldwide movement to reduce or entirely ban the use of plastics. But despite this, in a report titled, The Future of Petrochemicals, the IEA said that plastics will displace transport fuels as the main driver for crude oil demand in the future, with petrochemicals making up more than 33% of oil demand growth globally from now to 2030.

It said plastics demand will drive half of global oil demand growth by 2050, raising oil demand by 7 MMbbl/d by 2030. The IEA said it intended to report on plastics and other sectors of the global energy industry that receive less attention than oil and gas.

A Rebound Effect

It may be premature to deliver a eulogy for the oil and gas industry now. The Great Energy Transition could take two or three decades, maybe longer. But make no mistake, the energy industry is trying to decipher the tea leaves, and institutional investors are demanding that companies outline how peak oil demand will change their corporate strategies.

“Hydrocarbons—oil, natural gas and coal—are the world’s principal energy resource today and will continue to be so in the foreseeable future,” said The Manhattan Institute’s Mills. “Wind turbines, solar arrays and batteries, meanwhile, constitute a small source of energy and physics dictates that they will remain so. Meanwhile, there is simply no possibility that the world is undergoing—or can undergo—a near-term transition to a ‘new energy economy,’” he said.

BP noted that if peak demand causes oil prices to fall, that in turn will cause oil demand to rise again, which will motivate producers. “The response of U.S. oil demand to the recent period of low prices highlights an important issue when considering the likely profile of demand, once global oil demand peaks,” the company said. “If the peaking in oil demand (or even just the prospect of peaking) causes prices to fall, this is likely to trigger a so-called ‘rebound effect,’ in which falling prices stimulate higher demand.”

Bernstein’s Beveridge concluded that the bottom line is that if the oil age does peak in 2030-2035, producers will still need to prove up additional reserves, in light of the level of demand then (likely more than today’s level of 100 MMbbl/d), to offset the decline curve of existing production.

“While we don’t foresee any shortage of resources, the cost to develop these will require a higher oil price than the forward curve projects, which leads us to conclude that there is still more gas left in the tank, and oil-linked equities can still be a good investment over the coming decade,” Beveridge said.

Leslie Haines can be reached at lhaines@hartenergy.com.

Recommended Reading

Kosmos’ Stars Shine Bright in 2Q

2024-08-08 - With the startups of Jubilee Southeast and Winterfell, Kosmos Energy is halfway to achieving its production goal.

Petrobras to Add Two FPSOs Offshore Brazil in Second-half 2024

2024-08-12 - Petrobras will bring online 280,000 bbl/d of production capacity in the second-half 2024 with the addition of two FPSOs offshore Brazil.

Exxon Surprises with Smaller FPSO for Guyana’s Hammerhead Project

2024-07-19 - Exxon Mobil Corp. announced plans for its seventh development offshore Guyana, Hammerhead, which will add 120,000 bbl/d to 180,000 bbl/d of production capacity starting in 2029.

Hess Seeks Partnership for Suriname Block 59

2024-08-22 - Hess Corp. is seeking a new partner or partners to join in Suriname’s offshore Block 59 after Exxon Mobil and Equinor each gave up their one-third interests last month.

E&P Highlights: Aug. 5, 2024

2024-08-05 - Here’s a roundup of the latest E&P headlines, including new oil discoveries and an implementation of AI technology in operations offshore United Arab Emirates.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.