(Source: Hart Energy/Shutterstock.com)

[Editor's note: A version of this story appears in the February 2020 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Free cash flow (FCF) is often viewed as a destination akin to the Promised Land. Once a certain inflection point has been crossed, the hope is for a growing wedge of FCF as output moves higher, commodity prices stay constant and economies of scale kick in to keep costs down. But the world doesn’t always work that way. And much can depend on where an E&P is on the path to the Promised Land.

A recent heightened focus on FCF reflects the unease among some investors with the host of underlying inputs used to value E&Ps historically. E&P analysis has at times focused on net asset value (NAV), enterprise value-to-EBITDA (EV-to-EBITDA) and debt-adjusted cash flow per share growth, to name a few. In turn, these relied on other variables: rig counts, production growth, commodity prices, etc.

As investors, and especially generalist investors, have sought to bring clarity to E&P performance, some have turned to the basic elements of FCF as a minimalist marker.

“If an E&P is able to hold production flat year-over-year and—all other things being equal—generate a certain amount of operating FCF, then a generalist investor can say the E&P created value,” explained one industry observer, who termed FCF the “metric of last resort.”

FCF a pre-requisite?

Moreover, for an industry that has underperformed the broader market for most of the decade, it is free cash flow that has in some cases become a first check—or potentially even a pre-requisite—for reviewing investments in energy. But analysts caution against FCF being used in isolation. Rather, FCF can often be of greater use when employed with other metrics to round out the overall picture of an E&P.

While FCF may be in vogue, that’s no reason to play down the importance of other industry metrics, such as NAV, EV-to-EBITDA, return on equity (ROE) or invested capital (ROIC), according to David Deckelbaum, CFA, senior analyst at Cowen covering the E&P sector. For one thing, it’s not as if free-cash-flow yields are currently the primary valuation metric on which the E&P sector trades, he said.

“Currently, I wouldn’t say the stocks necessarily trade on FCF yields,” Deckelbaum said. “First, FCF is not being generated in substantial amounts by the E&P sector. And, second, I think there are other attributes that are important to the oil and gas investment story. FCF yield is more of a coincidental metric. It can be more of a pre-requisite before considering other metrics.”

NAV still important

“I think NAV is still important—certainly as it relates to developed booked reserves, if not undeveloped resource,” continued Deckelbaum. “Also, I think EV-to-EBITDA multiples are still relevant. And other return metrics, such as ROE and ROIC, can end up being important ways for E&P names to distinguish themselves. You’d rather have a unique story if you’re not generating FCF.”

With West Texas Intermediate (WTI) prices in the low to mid-$50s per barrel (bbl) range, “probably 60% or more of the investable universe is capable of generating FCF in 2020,” estimated Deckelbaum. “And that number could potentially be skewed higher if companies go toward maintenance mode. But most E&Ps are already in or near maintenance mode, so it would be unlikely to move materially higher.”

Not surprisingly, large-cap E&Ps have a lead in attaining FCF generation. At Cowen’s $54/bbl crude price forecast for 2020, roughly 80% of Deckelbaum’s large-cap coverage is projected to be FCF generative. Including small- and mid-cap (SMID) names covered by Cowen senior analyst Gabe Daoud, a total of 22 of 31 names, or roughly 70% of all coverage, are projected to generate FCF in 2020.

Cowen’s underlying assumptions are that its large-cap names under its coverage spend just 90% of cash flow in 2020, contributing to a year-over-year decline in industry capex of about 13%. Small-cap names are expected to both outspend and underspend cash flow but on average spend in line with cash flow. Industry analysts generally point to a deceleration in U.S. production growth due to lower 2020 capex.

With investor sentiment so depressed late last year, “I think you have a better chance of being rewarded right now for a respectable FCF yield vs. trying to achieve some measure of production growth,” said Deckelbaum. “In a perfect world, if you were highly FCF generative and growing, you’d probably get credit. But, at this point, a stock is going to be much more highly rewarded by FCF than growth.”

FCF as part of a balance

So, with seemingly few investors clamoring for growth, is free cash flow alone—rather than some sort of balance—now the key objective of energy investors? After all, for at least a temporary period of time, FCF can typically be attained by simply cutting capex and letting existing wells flow to bring in cash. But, in an industry deeply characterized by depletion, such a strategy is quick to take its toll.

Deckelbaum points to a three-pronged strategy for E&Ps, which would likely comprise 5% repeatable production growth, a 5% FCF yield and a 0.5 turn, or a little higher, in terms of EBITDA-to-net debt.

If the leverage metric seems austere, he said, the reason is that “if an E&P has credit coming due in the near term, there’s skepticism in the market that you’re going to be able to refinance it elegantly.”

Of course, not all E&Ps are at a more mature stage of their life cycle where they can balance out growth, FCF and debt maturities. Through no fault of their own, the growth of some E&Ps may have been disrupted from what was planned to be an expansion to critical mass and, in time, FCF. One such E&P caught out by market moves was Centennial Resource Development Inc., noted Daoud.

“Centennial used to trade at a premium to other midcap names,” he recalled. “The company wanted to get to critical mass, to reach an appropriate scale of over 60,000 barrels per day at that time. Typically, an E&P needs to grow to a certain level and then over time see its base decline rate become more moderate. From there, an E&P can potentially start thinking about throwing off some free cash flow.”

‘No man’s land’

“In late 2018, when oil went from over $60/ bbl to roughly $46/bbl, Centennial made a decision to rein in capital and steer away from a heavy growth ramp,” continued Daoud. “But it’s still trying to play catch-up and narrow its cash outspend despite not growing its oil production as fast as it was a couple of years ago. Investors view the company as being in a ‘no man’s land’ type of bucket, with no growth or free cash flow.”

In Cowen’s view, who stands out as recent winners in delivering the FCF desired by many investors?

Deckelbaum points to Noble Energy Inc. and Diamondback Energy Inc., while Daoud favors Parsley Energy Inc. and WPX Energy Inc.

“Noble Energy offers a high single-digit FCF yield in 2020 and 2021,” said Deckelbaum. “It has world-class assets that it’s expanding at Leviathan and other projects offshore Israel that are highly FCF generative. We think FCF continues to grow in 2022. It’s a unique FCF story that checks a lot of the boxes for investors. Noble’s differentiated asset base in the Eastern Med sets up a repeatable FCF stream.

“In the Permian, Diamondback has the capacity to sustain a high single-digit compound annual growth rate of production over the next five years, while making moves to sustain a 2% dividend yield, assuming an increase this year,” according to Deckelbaum. “This would make the stock competitive with the broader S&P 500,” given a dividend raise, a 6% FCF yield in 2020 and a pristine balance sheet.

A “merger of equals” among SMID-cap names is one way some E&Ps may generate attractive FCF in the near term, according to Daoud. The Cowen analyst cited Parsley Energy, his top pick, as an example.

In Parsley’s case, its acquisition of Jagged Peak Energy has set the stage for a markedly improved FCF profile, said Daoud. Plans are to slow down activity and reduce well costs at the former Jagged Peak operations, freeing up cash. With other synergies, the combined company is forecast to generate some $100- to $200 million of FCF, up substantially from a standalone $50- to $100 million in 2020, he said.

Bottom line: A FCF wedge for Parsley of about 2% in 2020 rises to roughly 4% in 2021, as oil production grows by over 10% this year and 5% to 10% in 2021, and a recently initiated dividend is increased.

Daoud’s price target for Parsley is $29 per share. His other most favored stock, WPX Energy, recently made a $2.5 billion acquisition of Felix Energy. His WPX target price is $18 per share.

‘Compelling’ valuation

Similar to Parsley’s ability to augment free cash flow by acquiring Jagged Peak, Daoud also pointed to the merger of PDC Energy Inc. and SRC Energy Inc. in Wattenberg Field in Colorado. PDC plans, he said, call for “a slowing down of activity on SRC acreage and taking out lots of costs, largely in general and administrative expenses. Pro forma, PDC should generate over $200 million in FCF next year on our numbers.”

Bottom line: PDC offers a 10% FCF yield, based on a $200 million FCF estimate for 2020, which is likely to “only grow in 2021 and beyond.” At an EV-to-2020 EBITDA multiple of around 2.5x, the PDC valuation is “compelling,” even allowing for a typical Wattenberg discount.

Daoud struck a note of caution as to some smaller E&Ps with higher debt levels, such as QEP Resources Inc.

“QEP is expected to generate FCF in 2020, which on its market cap is a pretty attractive FCF yield. But relative to its enterprise value, it’s not that attractive. That’s the problem with some smaller names. The FCF they’re generating is not enough to make a dent in upcoming debt maturities. QEP’s first maturity is a $400 million note coming due in 2021.”

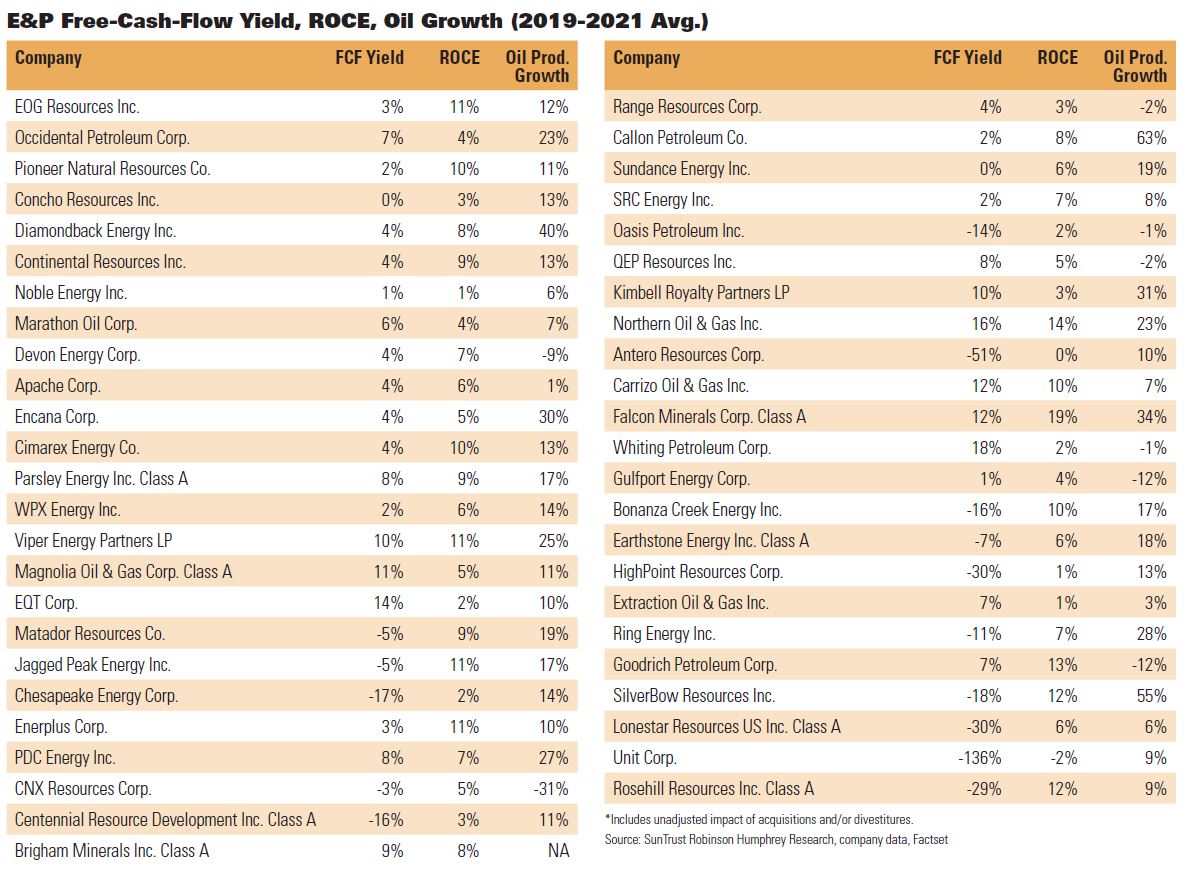

To provide context for investors, analysts at SunTrust Robinson Humphrey show FCF projections with accompanying data on the individual E&Ps’ return on capital employed and oil production growth. “Any of these E&Ps can be temporarily FCF generative; the question is whether you can do it on a sustainable basis,” observed Neal Dingmann, managing director, E&P research.

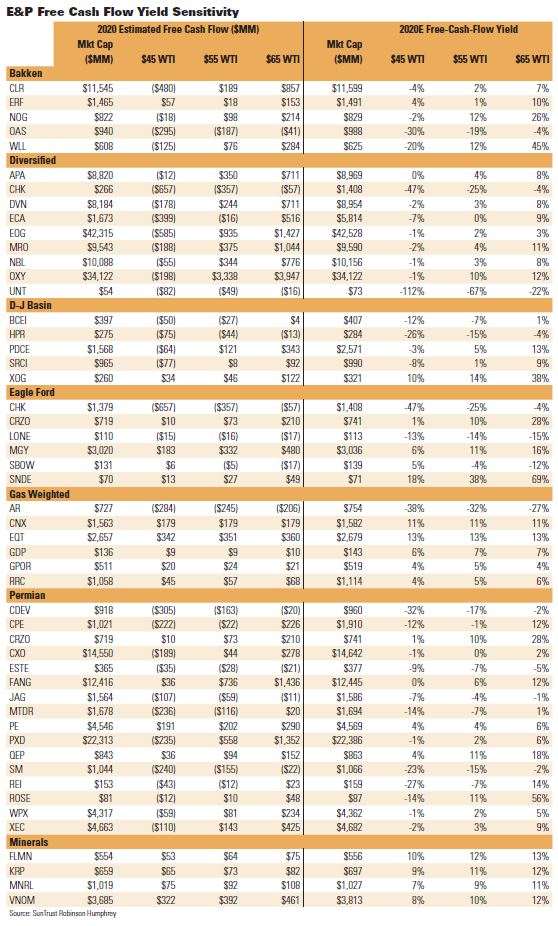

SunTrust E&P analyst Dingmann and managing director Welles Fitzpatrick project some 30 out of 49 E&Ps under their coverage generate free cash flow at a WTI price of $55/bbl. However, FCF is sensitive to variations in commodity prices (plus critical production levels), and at a WTI price of $45/bbl, the number of E&Ps generating FCF falls to roughly half of that at $55/bbl.

Conversely, if crude prices can be sustained at $55/bbl or higher, the often “range-bound” results of E&Ps recently may turn to delivering FCF in line with investor demands, said Dingmann. “Investors are demanding FCF. For a while we heard it, but they weren’t demanding it like they are now. Most of our coverage can deliver FCF and some growth if the 12-month strip is $52.50 or above.”

‘Extreme fatigue’ on energy

The increasing use of free cash flow as a key metric partially reflects “extreme fatigue” among remaining buy-side energy players, as well as an attempt to reach out to generalist investors, according to Fitzpatrick. If trying to schedule E&P meetings with institutional investors in New York or Boston, and an E&P is not yet generating FCF, the meetings “may not even be under consideration,” he said.

“Investors don’t necessarily trust slides showing internal rates of return [IRR], and everyone knows you can play with NAVs,” he said. “But if you can hold production flat, throw off a high single-digit FCF and demonstrate a decade of running room, that symbolizes a real company to a generalist investor. It’s a short cut. It cuts through much of the fog.”

What is problematic is a tendency to apply similar standards to both early stage E&Ps and more mature large cap names—say, for instance, Bonanza Creek Energy and Diamondback Energy Inc. “FCF is being thrown out as if it was almost a ‘universal rule,’ regardless of the portion of the life cycle that an E&P may be in, which can be a little frustrating,” commented Fitzpatrick.

“The problem is that the size, and where they are in the life cycle of an E&P, can make it very challenging for some E&Ps,” added Dingmann. “For example, Centennial Development has great acreage, but the stock has traded way down because it’s been outspending. If it could have had an extra year or two under its belt right now, I think it would be a much different story.”

Ultimately, “commodity price and timing are two of the bigger factors E&Ps are facing,” he commented.

Fine-tuning factors

As investor priorities evolve, E&Ps have tried to fine-tune the mix of factors driving stock performance.

Dingmann cited Matt Gallagher, CEO of Parsley Energy, whose strategy has been to combine a number of factors that in aggregate offer returns to investors of around 15%. In varying amounts, the 15% may be made up of shareholder returns (dividends and share buybacks), a free-cash-flow yield and production growth. For instance, the mix could be 3% to 4% shareholder returns, 5% FCF yield and 7% to 8% growth.

“Whatever the combination ends up being, it will add up to 15%,” said Dingmann. “They’re doing that without being too specific and painting themselves into a corner.”

Parsley Energy and WPX Energy were both held out by Dingmann as having crossed an inflection point where, due to scale, generating FCF tends to become less arduous. Other smaller E&Ps, “because of where they are in the cycle, probably need to outspend for another two years to get to that inflection point. But they may not get the opportunity if they have to keep close to cash flow neutrality.”

How do you rate the risk-reward of playing an E&P with FCF on the rise vs. a proven player, like, ConocoPhillips Co., which has the visibility of shareholder returns for many years to come?

“I’m more apt to play those that are past an inflection point—say, Parsley, WPX and Noble Energy—because they give me comfort they’ll not only continue to generate FCF in an lower commodity price environment, but, in addition, they’ll offer greater upside to crude prices if the commodity does go up,” said Dingmann. “Every dollar above $52 to $53 per barrel drops right to the bottom line.”

With market conditions reflecting more macro- and catalyst-driven events, fundamentals have been less of a factor, creating opportunities to pick up top stocks at cheap values, observed Fitzpatrick.

More macro-driven events

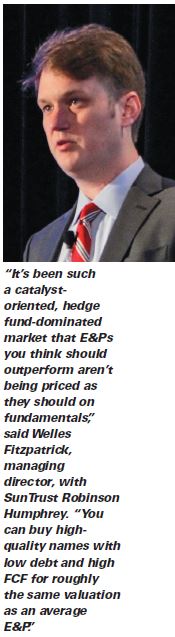

“It’s been such a catalyst-oriented, hedge fund-dominated market that E&Ps you think should outperform aren’t being priced as they should on fundamentals,” he said. “You have so few people with books built on fundamentals that all these names have become jumbled up. You can buy high-quality names with low debt and high FCF for roughly the same valuation as an average E&P.”

Fitzpatrick pointed to PDC Energy as having a valuation that is “crazy, trading at a high single-digit FCF yield, low double-digit cash flow per share growth on a year-over-year basis and just 2.5x EV-to-2020 EBITDA. It’s a fantastic company. And there are other high-quality names that don’t have you stepping that far out on the risk curve that are on sale with other E&Ps with more severe debt issues.”

Market trends over the past few years have created a backdrop “where stock picking has enjoyed the most target-rich environment it has had in some time,” said Fitzpatrick.

For Dingmann, favored names are Diamondback Energy, Continental Resources Inc. and Parsley Energy. Fitzpatrick favors PDC Energy and Brigham Minerals Inc., a play on minerals. “It has world-class acreage. If you have a long-term, positive view of U.S. shale, Brigham is the easiest way to sleep at night,” said Fitzpatrick.

Resisting FCF calls

Not all E&Ps have tried chasing the herd, however, in terms of free cash flow generation. Some E&Ps have preserved earlier strategies rather than bow to premature calls to generate FCF, said Dingmann.

“Matador Resources Co. is very upfront about it. They will tell you, ‘We won’t be FCF positive until about January of 2022,’” he said. “They say that to maximize returns of their investments—comprising not only an upstream investment, but also a material midstream investment named San Mateo—they need to outspend cash flow. They don’t make any bones about it. They‘re being very honest.”

Likewise, in a December “meet and greet” in New York, large-cap EOG Resources Inc. “did not succumb to analyst-investor pressure for high near-term FCF yield and shareholder returns, including stock buybacks, given its belief it is too early in its operations cycle,” noted Dingmann. “We believe many long- only investors remain on the sidelines until higher FCF and shareholder returns are seen.”

Other analysts have discussed how to balance the advantages of maintenance, growth and returns. For example, a Bernstein report estimated that, by moving to a maintenance capex level set to keep production flat, EOG would generate as much as $17 billion of incremental FCF over the next six years.

Reasons offered by Bernstein as to why EOG would continue to prioritize growth included: a different long-term view of the industry, including greater emphasis on NAV or incremental IRR; a desire by EOG to keep its organization intact, given its unique culture, technology, etc.; and an observation that “those companies transitioning to lower growth/buybacks haven’t been massively rewarded.”

SIDEBAR:

Felix Acquistion Adds FCF

Tulsa, Okla.-based WPX Energy Inc. announced a $2.5 billion purchase of Felix Energy in a deal described as being “accretive on all important metrics.” These included earnings per share, cash flow per share, net asset value and return on capital employed. Importantly, WPX also disclosed initiation of a dividend and pointed analysts to data supporting significant free-cash-flow (FCF) growth.

The purchase involved production from Felix in the Delaware Basin that is expected to grow to 60,000 barrels of oil equivalent per day (boe/d) at closing. The transaction will add some 1,500 locations, raising total Permian locations to more than 4,900 locations. Assuming $30,000 per flowing boe for the 60,000 boe/d, the transaction values the undeveloped acreage at less than $12,000 per acre.

Cowen senior analyst Gabe Daoud estimated that the pro forma company would generate almost $180 million in FCF in 2020, well above the nearly $60 million it would generate on a standalone basis. Free cash flow in 2021 was forecast to rise to just under $525 million, representing a 9% FCF yield on a Dec. 12, 2019, closing price of $10.91 per share, as compared to a standalone FCF estimate of under $140 million.

In addition, WPX stated it would pay a 10 cents per share dividend on an annualized basis upon initiation.

Others were similarly upbeat. In Credit Suisse’s recent report, “Uncovering a Hidden Gem,” E&P research analyst Betty Jiang forecast FCF generated by the combined company would double from $200 million to roughly $400 million in 2021 at $55/bbl. This would support “WPX’s vision of delivering both sustainable shareholder returns and growth,” according to the report.

Credit Suisse said the resultant 7% to 10% FCF yield was notable in that this milestone would be achieved in late 2021 with the Felix acquisition vs. what had been a projected standalone timetable of 2024. In similar manner, the Felix transaction was expected to allow WPX to attain a double-digit return on capital metric more than two years earlier than the prior target of 2024.

Also of interest was that the “slowback” choke management strategy used by Felix led to wells having lower IP rates but outperforming over the longer term through maximizing reservoir pressure. This is now expected to result in a 30% or lower base decline rate by year-end 2023, some six to 12 months ahead of prior expectations.

The Felix transaction price consists of $900 million in cash and $1.6 billion in WPX stock issued to the seller, subject to closing adjustments. WPX plans to fund the cash portion through issuance of $900 million of senior notes on an opportunistic basis. WPX has a commitment from Barclays in connection with the transaction and has full access to a $1.5 billion revolving credit facility.

WPX expects to add two members from EnCap Investments LP, who founded Felix Energy, to its board.

Topic du jour

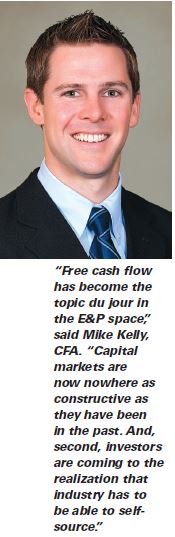

“FCF has become the topic du jour in the E&P space,” said Mike Kelly, CFA, the former head of E&P research at Seaport Global Securities LLC. “I think it’s important for a couple of reasons. One, the capital markets are now nowhere as constructive as they have been in the past. And, second, investors are coming to the realization that industry has to be able to self-source at this point.”

After years of rapidly growing U.S. supply—and outspending cash flow on the part of E&Ps—it’s unrealistic to think “you can just go out there and plug any outspend by raising money on Wall Street,” he continued. “That’s no longer the case. Investors are insisting, ‘I need to know today—not two years out—that you have a FCF yield.”

Admittedly, the industry faces a tradeoff between having high growth rates and lofty levels of FCF, said Kelly. “It’s hard to do both. One of the things we’ve done is to see who has above-average levels of both FCF and growth. That’s where you want to be. You can’t just look at FCF in a vacuum. FCF may not be the most important variable, but I think it ranks among the top three.”

Different paradigm

If free-cash-flow economics swing within a $10/bbl band—with relative few E&Ps generating FCF at sub-$50 levels, but almost all FCF positive at $60/bbl—do E&Ps add rigs if crude reaches the top end of the range?

“I do think the industry is now operating on a different paradigm,” observed Kelly. “I don’t think E&Ps are going to be eager to add rigs to the equation. People are beginning to compete on FCF yield. And if that’s the metric, you hurt yourself on that yardstick if you add a rig back. They’re more likely to issue dividends, or buy back stock or pay down their debt.”

In terms of favored stocks, “I still think it makes sense to own the E&Ps that are going to get there in a couple of years in a meaningful way, and still have really great growth profiles and great economics,” commented Kelly. “To me, Diamondback Energy, Parsley Energy and WPX Energy fit that mold. I’d prefer owning them over those with slower growth and a stronger FCF yield today.”

Obviously, most strategies involve some “give-and-take,” said Kelly. “If you want to isolate FCF, you can do that. But you may be doing that at the expense of growth, and you may be doing that at the expense of building out your inventory or attaining other goals. There are consequences of focusing solely on FCF. You can’t score highly on all fronts at the same time.”

But for the moment, FCF is “in vogue,” and it may be the necessary lure to attract generalist investors.

“The energy industry has to make sense to a generalist,” said Kelly, who is moving to Northern Oil & Gas Inc., which owns nonop properties mainly in the Williston Basin. “Energy has to make itself more comparable to other industries. For a few years it got a pass, and had its own set of rules, but now they’re being re-written to make the industry accountable to the same rules as other sectors.”

Recommended Reading

E&P Highlights: July 1, 2024

2024-07-01 - Here’s a roundup of the latest E&P headlines, including the Israeli government approving increased gas export at the Leviathan Field and Equinor winning a FEED contract for the all-electric Fram Sør Field.

E&P Highlights: Sep. 2, 2024

2024-09-03 - Here's a roundup of the latest E&P headlines, with Valeura increasing production at their Nong Yao C development and Oceaneering securing several contracts in the U.K. North Sea.

Chevron’s Gulf of Mexico Anchor Project Begins Production

2024-08-12 - Chevron and TotalEnergies’ $5.7 billion floating production unit has a gross capacity of 75,000 bbl/d and 28 MMcf/d.

Chevron Boosts Oil, NatGas Recovery in Gulf of Mexico

2024-09-03 - Chevron’s Jack/St. Malo and Tahiti facilities have produced 400 MMboe and 500 MMboe, respectively.

CNOOC’s Bohai Bay Well Achieves High Yield

2024-07-11 - CNOOC’s Bozhong 19-6 Condensate Gas Field D1 well, the first ultra-deep well in China’s Bohai Bay, is currently producing approximately 6,300 boe/d.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.