This excerpt is from a report that is available to subscribers of Stratas Advisors’ Short-Term Price Outlook service.

OPEC and its allies’ ability to adhere to the agreed upon output levels, combined with the pace of U.S. shale production growth will be the key determining factors for prices over the next two years. Currently OPEC has extended the production deal agreed to in 2016 through the end of 2018 and appears to be setting the stage to extend the timeline for ending the deal even further. Despite recent comments from a few OPEC members that the deal has not yet accomplished its aims we believe that the risk is rising that the group decides to scale back, either officially or unofficially, its commitment to managing production in the face of strong growth from the U.S.

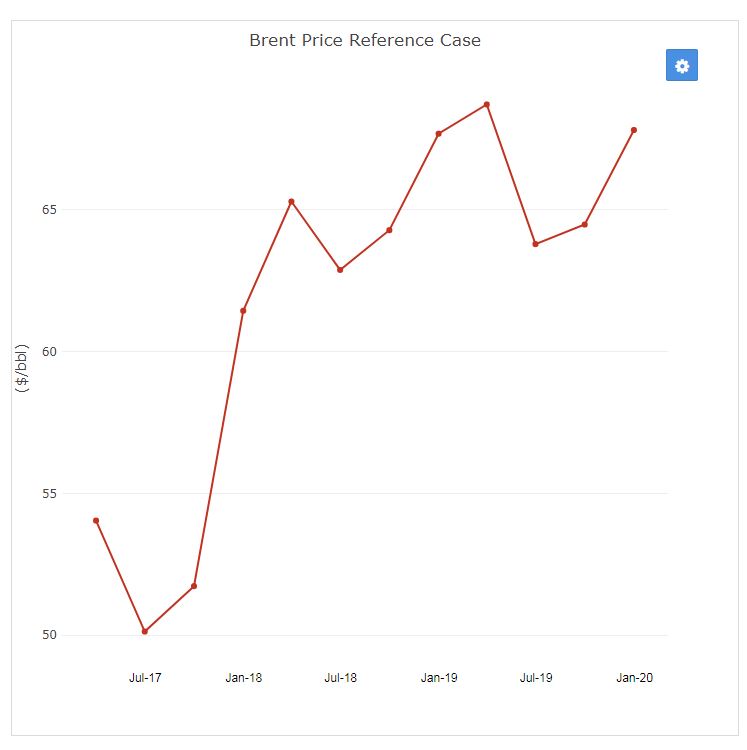

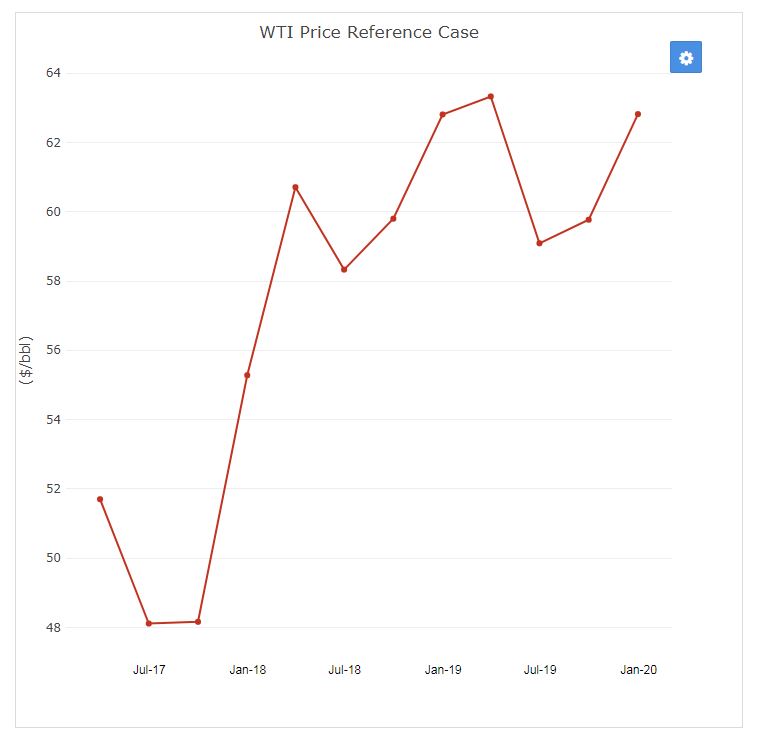

It is our expectation that Brent will average $65.02/bbl in 2018 before increasing to an average $66.19/bbl in 2019. WTI will average $60.41/bbl in 2018 and $61.25/bbl in 2019. These prices are predicated on the OPEC production agreement holding through end-2018 with minor slippage starting June 2018. Crude oil demand will grow approximately 1.1 MMbbl/din 2018 and 2019.

Economy: According to the World Bank, global GDP growth accelerated to 3 percent in 2017 from 2.4 percent in 2016. All major regions are experiencing growth for the first time since the financial crisis. Looking ahead, the World Bank expects global GDP growth of 3.1 percent in 2018 before slowing slightly to 3 percent in 2019. Growth from 2016 was driven by favorable financing costs, rising profits, and improved business sentiment across all economies. However, politics is an increasing risk to future growth. Despite a period of low prices, many governments failed to aggressively reduce energy subsidies and now that prices are rising government finances are again constrained. Constrained government finances will reduce investment in infrastructure which will then likely trickle through to restrict private investment. On top of this, US president Donald Trump has enacted tariffs on aluminum and steel imports as well as levies on up to $60 billion against Chinese goods. While the immediate reaction from China was muted, there remains the potential for escalation, a risk to global economic activity.

Geopolitics: As global oversupply is slowly reduced geopolitics are wielding more influence on prices. 2018 is shaping up to be a volatile year, which could reflect on prices. After months of increasingly fiery rhetoric between the US and North Korea there was a sudden shift on the part of North Korea, with Pyongyang proposing meetings between Kim Jong-un and South Korean president Moon Jae-in in late April. Additionally, concerns remain around the stability of the White House and future decisions around maintaining the Iran nuclear deal. President Trump has threatened several times to end the deal completely although it is unclear to what extent other signatories to the deal would go along with this. Markets will also closely watch the tone taken by White House officials after the appointment of John Bolton, a notoriously hawkish foreign policy figure, as national security advisor.

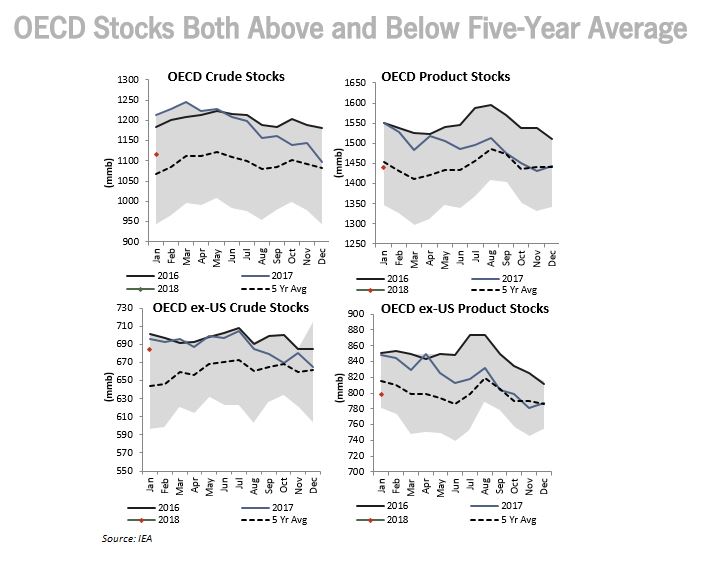

OECD Stocks Both Above and Below Five-Year Average

OECD crude stocks are currently only 39 million barrels above the five-year average, while product stocks are actually 15 million barrels below the five-year average. Presumably OPEC should be declaring success and taking a victory lap. However, recent comments from major members indicate they feel there is still plenty of work to be done to rebalance markets. In a way, they’re right. The current five-year average for crude and product stocks is inflated by three years of oversupply, effectively reducing the amount of drainage needed to declare balance. Comparing today’s numbers to the five-year average as of 2015 (average of stock levels from 2010-2014) the oversupply is still apparent. Crude stocks as of January 2018 were 163 million barrels above the 2015 five-year average while product stocks are 12 million barrels above the 2015 five-year average. Looking at the numbers from this perspective there is some support to the argument for extending the OPEC deal. The question then becomes, how will OPEC’s smaller members feel constraining production even longer? Will they consider extra revenues worth the wait?

Recommended Reading

Kosmos’ Stars Shine Bright in 2Q

2024-08-08 - With the startups of Jubilee Southeast and Winterfell, Kosmos Energy is halfway to achieving its production goal.

The EPC Market Keeps Its Head Above Water

2024-08-06 - While offshore investments are rising, particularly in deepwater fields, challenges persist due to project delays and inflation, according to Westwood analysis.

Nabors’ High-spec Rigs Help Keep Lower 48 Revenue Stable in 2Q

2024-07-25 - Nabors’ second quarter EBITDA was down 1% quarter-over-quarter but the company sees signs of increased drilling activity in international markets the second half of the year.

Wood Mackenzie: OFS Costs Expected to Decline 10% in 2024

2024-07-30 - As service companies anticipate a slowdown in Lower 48 activity, analysts at Wood Mackenzie say efficiency gains, not price reductions, will drive down well costs and equipment demand.

Hess Seeks Partnership for Suriname Block 59

2024-08-22 - Hess Corp. is seeking a new partner or partners to join in Suriname’s offshore Block 59 after Exxon Mobil and Equinor each gave up their one-third interests last month.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.