Stephen Pratt, senior associate and Permian analyst at Enverus Intelligence Research during Hart Energy’s 2023 Executive Oil Conference and Exhibition in Midland, Texas. (Source: Hart Energy)

As the core of the Permian Basin gets drilled up, E&Ps are eyeing deeper and fringier zones to fuel years of incremental drilling runway.

The overall number of top-quality drilling locations—often called Tier 1 inventory locations—across the North American shale patch is dwindling due to rising drilling and completion costs and declining well productivity.

Last year, energy analytics firm Enverus Intelligence Research estimated there were 125,000 remaining undeveloped locations across North America that are able to break even below a $40/bbl WTI price.

But the firm recently reduced its estimates to around 75,000 Tier 1 locations, at a sub-$45/bbl WTI price, due to cost and productivity headwinds.

“The pervasive cost inflation, as well as productivity degradation, we’ve seen over the last couple of years really drove about a 45% reduction in our estimates of Tier 1 inventory,” said Stephen Pratt, senior associate and Permian analyst at Enverus, during Hart Energy’s 2023 Executive Oil Conference and Exhibition in Midland, Texas.

“We also raised our cost of supply by about $5 to $10 higher year-over-year when compared to 2022,” he said.

RELATED

Analysts: Top-Tier Drilling Inventory Shrinking as Well Costs Rise

Plugging the Permian

The Permian Basin, already the U.S. Lower 48’s top oil-producing region, will continue to play a key role for operators as North American shale plays mature.

Of those, approximately 75,000 undeveloped Tier 1 drilling locations remaining across the continent; 75% are within the Permian’s Midland and Delaware basins, according to Enverus.

“The next lowest low-cost oil play, the Eagle Ford, holds only about 10% [of remaining Tier 1 inventory],” Pratt said.

Enverus estimates that the Midland Basin, much of which has been scooped up at premium prices by the largest majors and super-independents, holds approximately 10 years of remaining high-quality inventory.

The Delaware Basin, a more fragmented and less developed play, is estimated to hold around 15 years of remaining high-quality locations.

“We believe the Delaware core holds really the bulk or the majority of that high-quality remaining resource across the entirety of the basin,” Pratt said.

Enverus still sees some upside in maturing oil plays outside of the Permian Basin. The Bakken Shale and the SCOOP-STACK play are each estimated to hold around three to four years of remaining high-quality inventory.

The Eagle Ford Shale and the Denver-Julesburg Basin are each estimated to hold approximately nine years of remaining high-quality resource.

RELATED

WoodMac: Top-tier Permian Inventory Scarce, ‘Extremely Expensive’

To core or to explore?

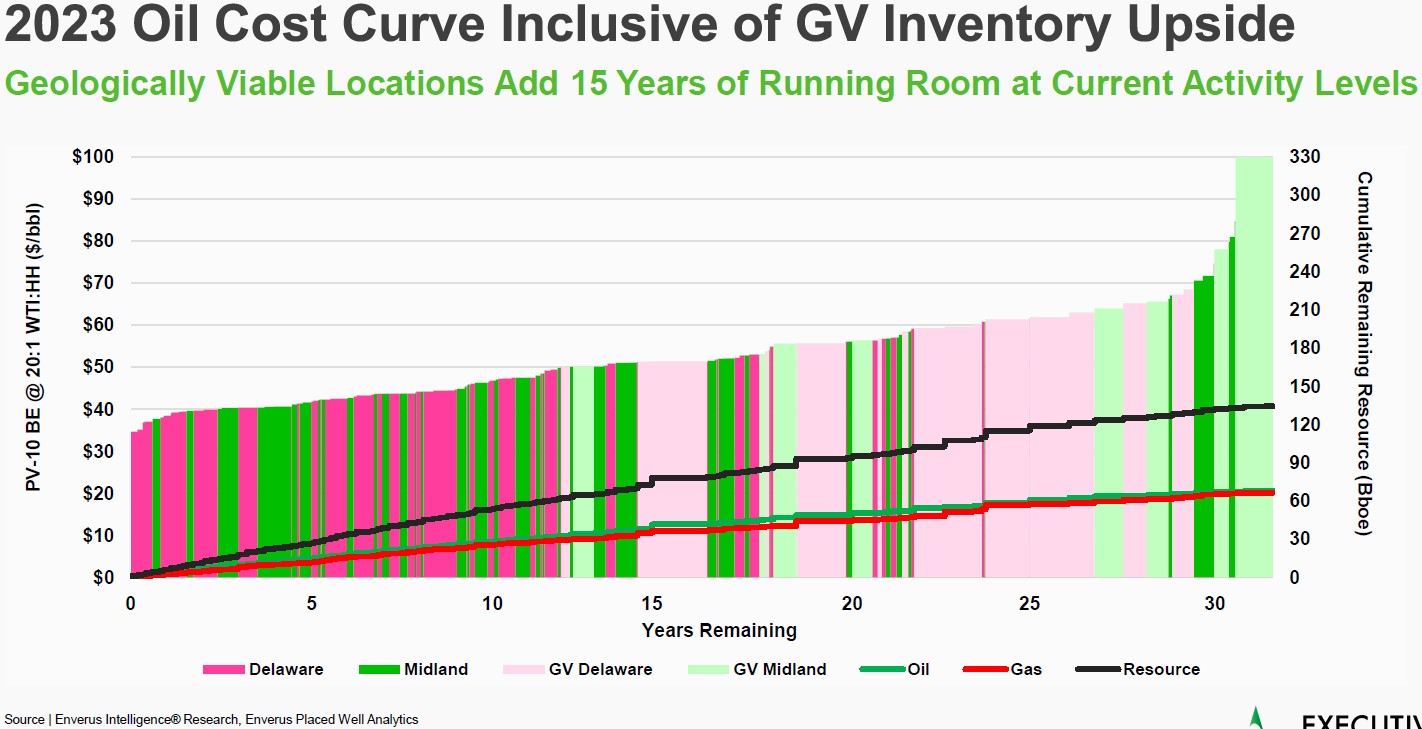

Operators and experts see several years of high-quality drilling runway remaining in the core of the Midland and Delaware basins. But Enverus also sees upside from geologically-viable inventory in more extensional, fringier portions of both basins.

“From a high level, the incorporation of geologically viable inventory in the Delaware adds roughly about 55,000 additional locations—but sitting much higher on the cost curve compared to what’s been proven to date,” Pratt said.

Secondary targets, including the Avalon formation and the deeper Wolfcamp C formation, make up around two-thirds of the 55,000 incremental Delaware locations, he said.

Enverus also finds unproven upside from geologically viable inventory in the Midland Basin.

“In total, we added an additional 25,000 locations in the Midland Basin, average breakeven in the range of about [$70/bbl to $80/bbl],” Pratt said. “So, certainly sitting much higher on the cost curve when compared to what’s been proven to date.”

With primary Spraberry and Wolfcamp targets already heavily developed, the Middle Spraberry and Wolfcamp D formations show the most geologically viable promise in the Midland Basin, per Enverus’ analysis.

Layering in the incremental 80,000 geologically viable future locations in the Permian could extend the basin’s life from around 17 years based on what’s been proven to date, up to around 32 years. “So, effectively doubling the life of the basin,” Pratt said.

“These locations obviously sit much higher on the cost curve but certainly extend the life of the basin quite dramatically,” he said. “With that being said, these locations certainly recover less oil—but we do believe they provide incremental barrels as we approach maturity in the basin.”

Recommended Reading

US Drillers Cut Oil, Gas Rigs for Fifth Week in Six, Baker Hughes Says

2024-09-20 - U.S. energy firms this week resumed cutting the number of oil and natural gas rigs after adding rigs last week.

Western Haynesville Wildcats’ Output Up as Comstock Loosens Chokes

2024-09-19 - Comstock Resources reported this summer that it is gaining a better understanding of the formations’ pressure regime and how best to produce its “Waynesville” wells.

August Well Permits Rebound in August, led by the Permian Basin

2024-09-18 - Analysis by Evercore ISI shows approved well permits in the Permian Basin, Marcellus and Eagle Ford shales and the Bakken were up month-over-month and compared to 2023.

Kolibri Global Drills First Three SCOOP Wells in Tishomingo Field

2024-09-18 - Kolibri Global Energy reported drilling the three wells in an average 14 days, beating its estimated 20-day drilling schedule.

Permian Resources Closes $820MM Bolt-on of Oxy’s Delaware Assets

2024-09-17 - The Permian Resources acquisition includes about 29,500 net acres, 9,900 net royalty acres and average production of 15,000 boe/d from Occidental Petroleum’s assets in Reeves County, Texas.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.