For shale producers, 2023 was a monumental year in terms of news flow. Thematically, public investors continued to focus on free cash generation and returns of capital to shareholders while considering the future of inventory depth. Public companies touted benefits of longer lateral designs as average lateral lengths observed across shale plays increased 3% in the Permian, 8% in the Eagle Ford and 1% in the Bakken.

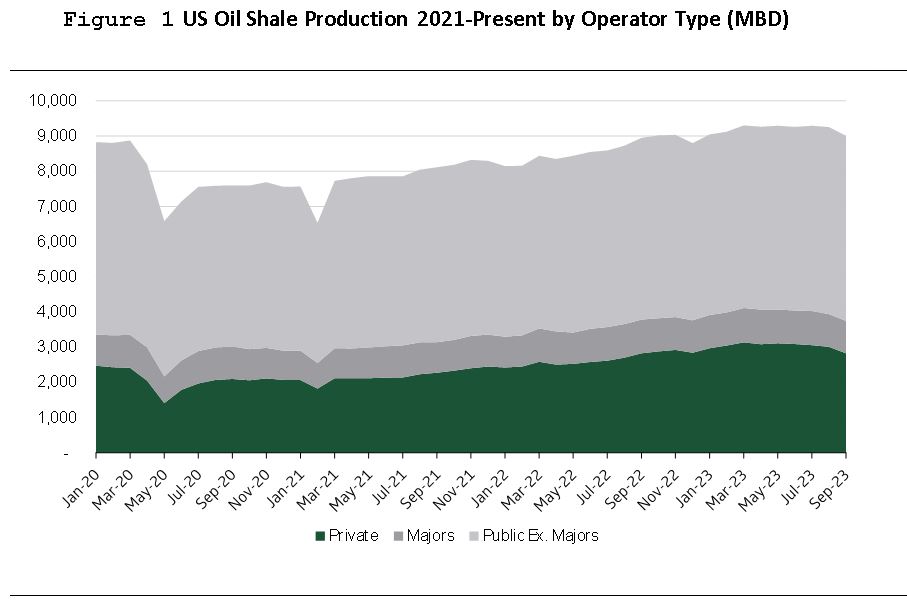

Coincidentally, for the first time in several years, oil productivity per-foot on average actually increased by 3% across all U.S. shale plays, following a relatively dramatic drop in per-foot productivity from 2021 to 2022. With most companies continuing to communicate relative maintenance programs, the market has responded with relative surprise to U.S. shale oil growth, now trending up 9% year-over-year as of the third quarter while the rig count on average has declined roughly 5% on average YTD and 20% since the beginning of the year.

At the end of the day, this dynamic is roughly half-explained by the growth witnessed in the private market as operators likely look to monetize to publics, while also benefitting from improved well performance, cycle times and enhanced well designs. Indeed, shale operators have improved operating efficiency while facing the narrative of limited inventory life.

Most public investors have scrutinized shale oil inventory depth and questioned the long-term sustainability of high return of capital profiles while weighing the risk of acquisitions. On the other hand, we have witnessed majors such as Chevron and Exxon Mobil taking four public names off the board—Pioneer Natural Resources, Denbury, PDC Energy, and Hess Corp.—albeit using all-equity takeout mechanisms with scant premiums.

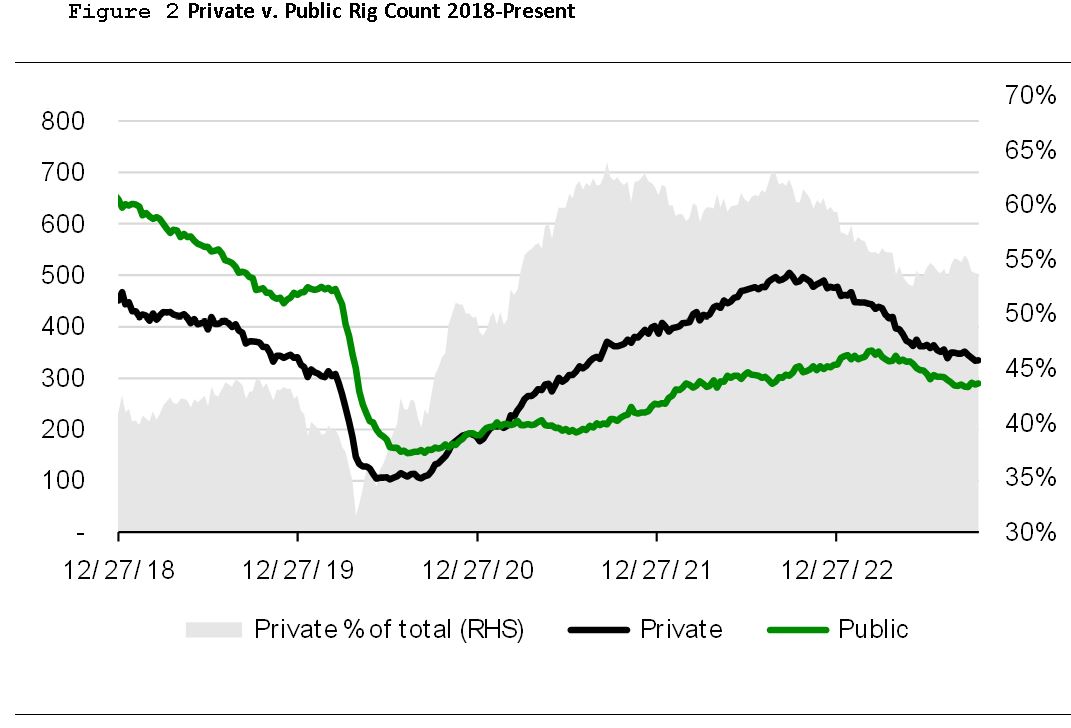

Indeed, the romance of large takeout premiums from majors is likely a relic of the past, but at the same time, the volatility around U.S. oil production growth should continue to decrease over time. Private-to-public consolidation has typically resulted in rig rationalization to augment near-term free cash. Considering that private operators contributed to roughly 5% of the 9% oil shale growth, the setup for U.S. oil production in 2024 will be heavily influenced by a marked shift in private operator market share that dropped from 60% at the beginning of 2023 to 52%, following a 32% decline in private rigs YTD versus 8% for public companies.

After averaging roughly 59% of the rig count since late 2020, the decline in private operator activity should have a noted impact on continued shale oil growth, particularly as publics continue to consolidate names like CrownQuest, Forge, Advance Energy and others, all meaningful players in the private Permian arena.

The path forward for U.S. shale in the public arena will inevitably now take the form of smaller bolt-on deals to replace inventory as limited opportunities in the private space remain for scale, with all eyes on the fates of names like Endeavor Energy. As the era of public-for-private consolidation theoretically comes to a near-term end, public names will now dictate the path of U.S. oil growth once again with an increased focus on development efficiencies, high-grading and inventory management.

As the world digests surprisingly robust U.S. oil production once again, along with several other global macro factors, it is fair to argue that one relatively bearish variable—private company shale growth—was significantly diminished heading into 2024.

Oil prices receded from north of $93/bbl at the end of September to about $72/bbl by mid-December, providing an interesting starting point for how U.S. public operators choose to behave that will be more heavily influenced by the majors’ activities.

Ultimately, the 2023 wave of consolidation should prove to have ongoing impact on domestic industry capital restraint, a critical goal of the investing public since late 2018. At the same time, the productivity gains experienced in 2023 provide a compelling backdrop for domestic shale and the conversion of lower tier inventory to higher tiers that will only be further informed by proclamations from larger players such as Exxon look to dramatically increase recoveries in the Permian as their footprint has grown through acquisition. The 2024 U.S. oil shale chapter should indeed prove to be a page-turner.

David Deckelbaum is managing director for sustainability and energy transition at TD Cowen. He is based in New York City.

Recommended Reading

Salunda, Intellilift Enter Pact to Optimize Automation in Well Construction

2024-08-21 - The agreement was signed following a successful pilot trial integrating Intellilift’s digital technologies with Salunda’s patented camera and wearable red zone monitoring solutions on a drilling rig.

International, Tech Drive NOV’s 2Q Growth Amid US E&P Headwinds

2024-07-29 - Despite a U.S. drilling slowdown, slightly offset by Permian Basin activity, NOV saw overall second-quarter revenue grow by 6%, although second-half 2024 challenges remain in North America.

Transocean Contracted for Ultra-deepwater Drillship Offshore India

2024-09-04 - Transocean’s $123 million deepwater drillship will begin operations in the second quarter of 2026.

How Generative AI Liberates Data to Streamline Decisions

2024-07-22 - When combined with industrial data management, generative AI can allow processes to be more effective and scalable.

AI & Generative AI Now Standard in Oil & Gas Solutions

2024-07-25 - From predictive maintenance to production optimization, AI is ushering in a new era for oil and gas.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.