Working natural gas in storage volumes could be on the low side as a new heating season begins. (Source: Shutterstock/Zivica Kerkez)

Natural gas has long been a global commodity, but until recently the U.S. was largely sheltered from this global market. Instead, the U.S. natural gas market was for the most part self-contained, aside from Canadian imports via pipeline and small amounts of liquefied natural gas (LNG) imports.

Domestic gas prices were primarily dependent on seasonal demand for heating and cooling. Most of the time, the easiest way to determine natural gas storage levels in the U.S. was to ask, “How’s the weather?”

However, since the dramatic increase in domestic production of gas resulted in the U.S. exporting large quantities of LNG, the U.S. has entered the global market in a major way. It’s gotten to the point that, while one of the key questions regarding gas storage levels still concerns the weather, now it isn’t just about the weather in the U.S. but also in Europe and Asia.

“More and more we have to look at the global picture and what the weather might be like in Europe and Asia. It's becoming more important for the U.S. to focus on global markets,” Terry Ciliske, principal at En*Vantage Inc., told Midstream Business.

As U.S. LNG exports continue to increase, that increases the number of drivers from around the world that impact domestic markets, including U.S. gas storage injections and withdrawals. This makes it more difficult to forecast natural gas storage levels, even on a short-term basis.

En*Vantage estimates that natural gas storage levels will be about 3.7 trillion cubic feet (Tcf) by the end of the summer. However, the more global nature of the U.S. gas market means it’s more difficult to have a firm hold on natural gas storage predictions.

“My biggest concern over the next few months is what could occur with LNG exports. The arb on LNG is continuing to get compressed, and prices in the Asian markets are more or less holding steady,” Ciliske said.

He noted that while there have been some discussions about China backing off of LNG imports, En*Vantage believes that there is flawed tracking data on some ships. “The way we run our numbers, we haven't seen a fall-off on net Chinese LNG imports.”

Ciliske added that there are also concerns over the sustainability of the European LNG market.

“Storage capacity in Europe was at over 70% full in June, and based on the data I’m looking at going back a decade, we’re not quite at record levels from a percentage standpoint—but we’re close. If things continue to deteriorate, then it would not surprise me to see U.S. export levels start to come down. If that’s the case, then you’ll start to change the end-of-season storage levels fairly dramatically.”

Record pace

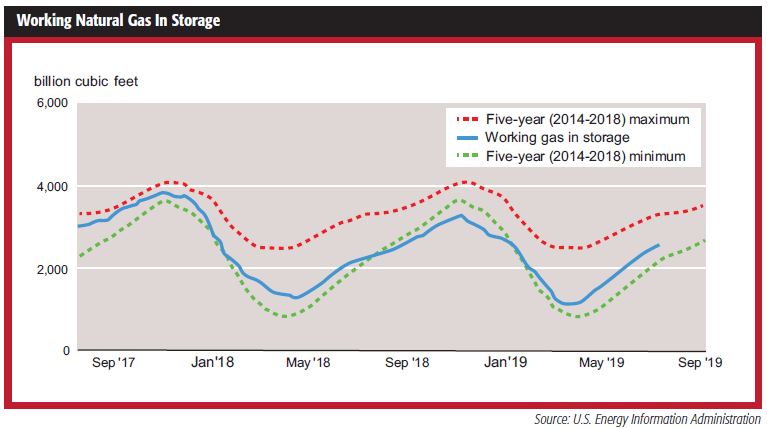

From a domestic point of view, overall power generation demand was tempered this summer. According to the U.S. Energy Information Administration (EIA), the first four months of the storage injection season saw an average of 98 billion cubic feet (Bcf) of gas injections. The cumulative net injections were about 41% higher than the five-year average—and at a record pace.

Part of this record pace involves the fact that there was an extremely low storage level coming out of the 2018-19 winter heating season, with only 1.137 Tcf of gas in storage, with working gas stocks 30% lower than the five-year average, according to the EIA.

“The 2018–19 heating season had the lowest level of working gas stocks in the United States for this time of year since 2014, when working gas stocks ended the 2013–14 heating season at 837 Bcf because of multiple, intense cold snaps,” the EIA said in a research note.

Despite the stagnant cooling demand that impacted gas markets at the start of the cooling season, U.S. natural gas demand is up due to increased power generation use.

“We have not seen the highs like we did last year. We’ve had a bunch of coal-fired power plant shutdowns and have added a lot of gas-fired power generation year-over-year. These are helping to absorb volumes, plus the low prices that we’re seeing in the field are sufficiently low enough to pick up some incremental load in certain sectors of the country in place of coal. In areas like the Permian where gas is essentially free—and assuming there’s sufficient transmission to local power plants—local generation is running pretty strongly, aside from holding back what they need for peak day reserves,” Ciliske said.

An aspect that has been overlooked when it comes to peak cooling days is that gas will be consumed at a much higher rate than during non-peak days. This isn’t just because there’s increased demand, but because as you go up the power demand curve, more gas is consumed.

Typically, power generators will operate their newest and most-efficient units, but at peak demand they will use most of their capacity—including older power plants—to meet demand. These older units aren’t as efficient as newer ones and may require up to twice as much gas on a burn cycle.

“If we get extremely hot temperatures, then price doesn’t matter as much because utilities will run everything. In the middle of August with high temperatures, nothing is going to get shut down, so prices can rise and there’s not as much demand elasticity for natural gas in the middle of August based on price. It's strictly a function of weather,” he said.

Permian capacity

The completion of several new pipeline projects could prove to be a wild card when it comes to gas storage levels this fall. Ciliske said that Kinder Morgan’s Gulf Coast Express Pipeline will transport up to 2 Bcf/d of natural gas from the Permian Basin to the Gulf Coast.

“There’s gas that’s available in the Permian that’s not currently going to market, so we could see a pop in production as soon as that line starts filling. Flared gas or shut-in gas will seek its way outward, and that will result in the basis getting much tighter in the Permian,” he said.

“What should happen is that if netbacks aren’t atrocious, these volumes will make their way into this system. You’ll then see a reduction of gas flow going north out of the Permian since they’ll get better netbacks going east to the Gulf Coast,” he said.

This has the potential to add another 50 to 100 Bcf of natural gas into storage inventories by driving the basis down in South Texas.

Good news/bad news

Pipeline exports to Mexico are a good news/bad news scenario for the U.S. gas market since there is a chance that these volumes could displace LNG that’s currently making its way from the U.S. to Mexico.

According to Ciliske, Mexico isn’t turning out to be the savior for the U.S. natural gas market that it was expected to be several years ago. While Mexican gas production is drastically decreasing and U.S. natural gas and LNG exports to Mexico have increased, demand for gas in Mexico isn’t growing as much as it was expected to.

“Over the last five to seven years, we’ve seen U.S. natural gas export volumes to Mexico go from about 2 Bcf/d to about 5.5 Bcf/d. The perception is demand is growing, but that’s not right.

“Ninety percent of that load increase is because Mexico’s natural gas production has been declining. Their demand has grown a little, but all we’ve done is increase our market share because their production declined. People tend to think that since we have this export capacity that demand will grow with it, and I’m not sure that’s the case,” he said.

Old drivers

While global factors have increased in importance, hot weather still plays an important part in determining how much gas will be in storage by the end of the summer. Not only do these high temperatures increase cooling demand, they also have an adverse effect on alternative energy—specifically wind-power generation.

“We have all of this wind power around the country, but the amount of output is very low in the peak of the summer because a lot of times when it gets hot, the wind dies down,” Ciliske said.

He added that other forms of alternative energy struggle in hot weather. The most surprising of these is solar power, because solar panels produce substantially less power as temperatures increase. For example, if temperatures are between 100 to 105 degrees, solar panel power output could degrade by as much as 15% to 20%.

Cooling demand may have been a bit slow to come on strong this summer, but the potential for a large overhang isn’t quite as strong because of legacy declines in shale gas wells, Ciliske said.

“We’ve dropped off a little in drilling, but the amount of drilling that needs to occur just to maintain deliverability continues to rise, and we’re now seeing the legacy declines in shales. We have to replace about 2.5 Bcf/d every month, so a lot of the drilling is going to replace the declines rather than growing the supply base. You’re seeing the growth rate of crude and natural gas flattening out and slowing down. We’re running faster and faster to stay in place,” he said.

The overall drilled and uncompleted well count is about flat or even down a bit, yet the Permian Basin remains an area of growth for U.S. producers. There are still a lot of drilled and uncompleted (DUC) wells to bring online in the Permian Basin. The largest percentage of these wells are oil wells, which means they won’t have as much of an impact on gas storage, but there will be some sort of impact as more gas wells in the region are completed.

Hard sale

Despite all of the changes in the gas industry, natural gas storage projects remain a hard sell. Ciliske noted that new gas storage projects haven’t been attractive since about 2010. However, as renewables take a larger piece of the power market, they also add a lot of price volatility. This in turn increases volatility for gas supply and demand. This supply and demand volatility makes it pretty tough economically for storage facilities unless they’re in key markets, such as the Northeast.

“The Northeast can be an attractive market for new storage facilities since operators are having so much trouble getting new pipelines built in the region. However, I think it’s more likely that LNG will help supplement storage capacity, especially if the Jones Act is waived,” he said.

The Jones Act requires U.S.-built vessels with U.S. crews to haul cargoes between domestic ports.

Even without the Jones Act being waived, LNG has served as a synthetic type of gas storage system, Ciliske said.

“We saw this last winter when prices spiked pretty steeply along the Eastern Seaboard and deliveries into the Cheniere LNG hub dropped way off. If producers have LNG sitting in tanks to fulfill orders they can reroute that gas into the U.S. marketplace instead, which dampens some of the volatility and puts pressure on storage values,” he explained.

It may be harder to tell where storage levels are headed because of all of the changes in the marketplace, but one thing remains the same: Storage levels remain a great mechanism for being able to see where gas prices could head unless stocks can either be replenished or storage overhangs can be quickly cleared.

Recommended Reading

Not Sweating DeepSeek: Exxon, Chevron Plow Ahead on Data Center Power

2025-02-02 - The launch of the energy-efficient DeepSeek chatbot roiled tech and power markets in late January. But supermajors Exxon Mobil and Chevron continue to field intense demand for data-center power supply, driven by AI technology customers.

BlackRock CEO: US Headed for More Inflation in Short Term

2025-03-11 - AI is likely to cause a period of deflation, Larry Fink, founder and CEO of the investment giant BlackRock, said at CERAWeek.

Transocean President, COO to Assume CEO Position in 2Q25

2025-02-19 - Transocean Ltd. announced a CEO succession plan on Feb. 18 in which President and COO Keelan Adamson will take the reins of the company as its chief executive in the second quarter of 2025.

Ovintiv Names Terri King as Independent Board Member

2025-01-28 - Ovintiv Inc. has named former ConocoPhillips Chief Commercial Officer Terri King as a new independent member of its board of directors effective Jan. 31.

Independence Contract Drilling Emerges from Chapter 11 Bankruptcy

2025-01-21 - Independence Contract Drilling eliminated more than $197 million of convertible debt in the restructuring process.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.