Comments made by Russian President Vladimir Putin on Oct. 22 are the clearest signal yet from Russia that it is ready to continue with unprecedented output cuts in the face of a sluggish oil market beset. (Source: Shutterstock.com; image of Russian President Vladimir Putin by Dimitrije Ostojic / Shutterstock.com)

[Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

Last week saw contradictory statements from OPEC’s technical committee with regards to how to address the upcoming market unbalance. But Russian President Vladimir Putin expressed that the current OPEC+ plan is currently an appropriate approach and if needed, producers should consider production adjustments.

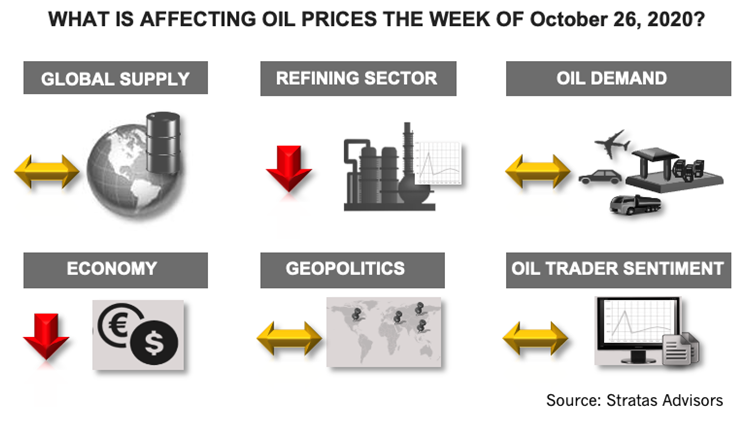

Global Supply—Neutral

While last week’s U.S. crude supply reduction is bullish for oil prices, the impact is offset by additional production from Libya coming online (as the result of the peace agreement signed last week). As such, we expect this variable to be a neutral factor for this week.

Geopolitics—Neutral

The most recent agreements reached by Israel with several countries could have important implications contingent upon the final position of Saudi Arabia. For this week we see this variable as neutral.

Economy—Negative

In the short-term, we expect this variable to be negative until there is the passing of a new stimulus package. While this development still remains, a possibility is not likely to occur before the upcoming presidential election.

Oil Demand—Neutral

The new lockdowns imposed in France and the continuous reports of additional infections throughout Italy, the U.K., and other countries bodes ill for crude prices this week.

Overall, oil consumption is remaining as resilient as possible in light of the COVID challenge, but it is difficult to see how this variable can play a positive role for prices this week. Therefore, we keep this variable as a neutral contribution to oil prices this week.

Refining Sector—Negative

Renewed lockdown orders in specific locations of Europe and Asia impacted refined product prices around the world, which translated into lower refining margins across all regions. The short-term picture bodes ill for refiners, given the demand concerns associated with the potential for a major rebound in COVID cases during the winter months, which will stifle product demand.

We expect this variable to be negative for this week.

Oil Trader Sentiment—Neutral

Open interest for the Light Sweet Nymex contract was 3% down, while the managed net statistics show an average increase of 15% with long positions increasing with respect to short positions. Meanwhile, open interest for the RBOB and USLD contracts were basically unchanged versus last week (a variation of less than 1%).

For the upcoming week, we expect this variable to be neutral for crude prices.

About the Author:

Jaime Brito is vice president at Stratas Advisors with over 24 years of experience on refining economics and market strategies for the oil industry. He is responsible for managing the refining and crude-related services, as well as completing consulting.

Recommended Reading

E&P Highlights: Sep. 2, 2024

2024-09-03 - Here's a roundup of the latest E&P headlines, with Valeura increasing production at their Nong Yao C development and Oceaneering securing several contracts in the U.K. North Sea.

Breakthroughs in the Energy Industry’s Contact Sport, Geophysics

2024-09-05 - At the 2024 IMAGE Conference, Shell’s Bill Langin showcased how industry advances in seismic technology has unlocked key areas in the Gulf of Mexico.

Interoil to Boost Production in Ecopetrol Fields

2024-09-03 - Interoil will reopen shut-in wells at three onshore fields, which are under contract by Ecopetrol.

Chevron Boosts Oil, NatGas Recovery in Gulf of Mexico

2024-09-03 - Chevron’s Jack/St. Malo and Tahiti facilities have produced 400 MMboe and 500 MMboe, respectively.

CNOOC Makes Ultra-deepwater Discovery in the Pearl River Mouth Basin

2024-09-11 - CNOOC drilled a natural gas well in the ultra-deepwater area of the Liwan 4-1 structure in the Pearl River Mouth Basin. The well marks the first major breakthrough in China’s ultra-deepwater carbonate exploration.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.