The movement of oil prices has been negatively correlated with the movement of COVID-19 cases, according to Stratas Advisors noted in its latest forecast. However, the question now is how much longer will crude prices remain on the upward trend? (Source: Shutterstock.com)

[Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

As we expected, crude prices continued going up last week, but more moderately than the prior week. The price of Brent crude ended the week at $84.92 after closing the previous week at $82.58. The price of WTI ended the week at $82.66 after closing the previous week at $79.59.

The movement of oil prices has been negatively correlated with the movement of COVID-19 cases—when COVID cases are increasing, oil prices have weakened and when COVID-19 cases have been waning, oil prices have strengthened. When COVID-19 cases started moving upwards and peaked in the beginning of September, oil prices went from $77 down to $65. With the subsequent decline in COVID-19 cases, oil prices have rebounded to new highs. So, the question now is how much longer will crude prices remain on the upward trend?

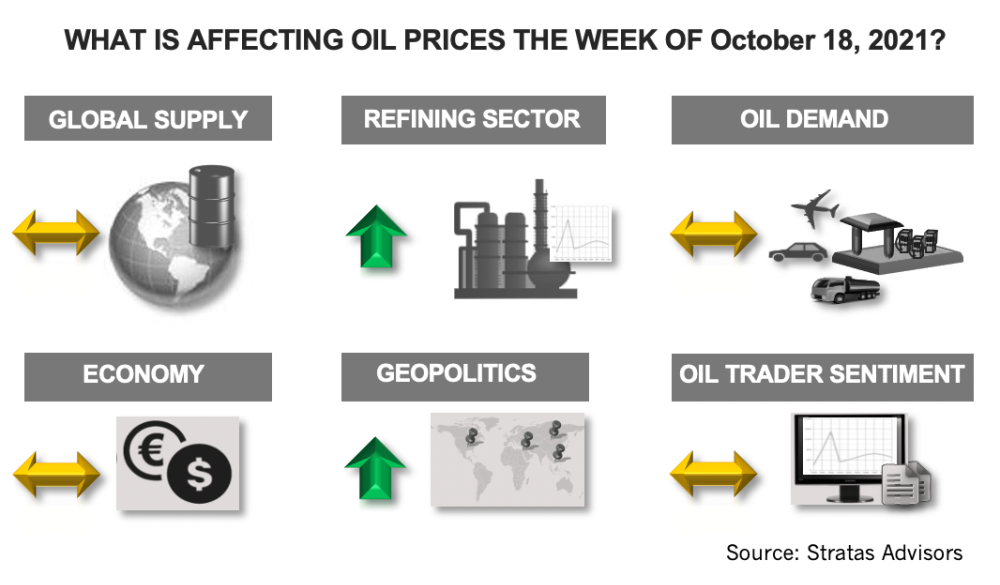

While the news about COVID-19 and supply/demand fundamentals remain favorable, we do see other factors that will moderate oil prices, including the following:

- We still hold the view that OPEC+ is comfortable with prices being around the $80 level but does not want prices to spike—nor does OPEC+ want to lose market share. OPEC+ will continue to monitor demand—and the pace of increases in non-OPEC supply, including US shale producers—as well as the oil price. As such, we think OPEC+ will add supply, when required, to achieve these goals. From a global perspective, we are forecasting that crude supply in fourth-quarter 2021 will be 5.60 million bbl/d more than in fourth-quarter 2020. In comparison with third-quarter 2021, supply in fourth-quarter 2021 is forecasted to be greater by 1.75 million bbl/d.

- OPEC supply to increase by 0.560 million bbl/d

- Non-OPEC supply to increase by 1.19 million bbl/d

- U.S. production to increase by 0.500 million bbl/d

- The global economy remains fragile with the U.S. and Europe facing monetary and fiscal challenges, which provide the potential for policy stumbles and disappointments. Additionally, there are still supply chain issues that are not only affecting consumers, but manufacturing sectors, including the automotive sector. For example, on Oct. 15, Toyota announced that it is reducing its global production by some 15% in November because of a chip shortage.

- Besides higher oil prices, the global economy is dealing with elevated natural gas and coal prices. Additionally, major economies, such as China and India, are facing energy shortages, which are requiring rationing and restrictions. While countries are taking steps to address the shortages, including the increase in coal production, it will take time.

- Last week, the U.S. Dollar Index declined slightly (93.95 versus 94.1). However, we are still expecting that the U.S. Dollar Index will continue to increase through the rest of the year and will approach 96.00.

For the upcoming week, we are expecting that crude prices will move sideways, in part, because traders are pulling back some from the bullish sentiment that has been increasing during the prior month. And the above factors will moderate the upward trend of oil prices during last quarter of this year.

About the Author:

John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

TGS Releases Illinois Basin Carbon Storage Assessment

2024-09-03 - TGS’ assessment is intended to help energy companies and environmental stakeholders make informed, data-driven decisions for carbon storage projects.

STRYDE Awarded Seismic Supply Contracts in Mexico

2024-09-03 - STRYDE was awarded two seismic node supply contracts in Mexico, the company’s first projects in the country.

PakEnergy Plows Ahead with New SCADA Solution

2024-09-17 - After acquiring Plow Technologies, home of the OnPing SCADA platform, PakEnergy looks to enhance its remote monitoring solutions.

SLB Launches New GenAI Platform Lumi

2024-09-17 - Lumi’s machine learning capabilities will be used to enhance SLB’s Delfi digital platform offering for better automation and operational efficiencies.

Honeywell Bags Air Products’ LNG Process, Equipment Business for $1.8B

2024-07-10 - Honeywell is growing its energy transition services offerings with the acquisition of Air Products’ LNG process technology and equipment business for $1.81 billion.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.