(Source: Shutterstock.com)

[Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

Just two weeks ago, Royal Dutch Shell Plc announced a plan to offer for sale seven refineries around and, surprisingly, last week announced the decision to close the Convent refinery in Louisiana.

Convent is better positioned than the other six refineries Shell is offering for sale. Given the way this decision unfolded, however, it is possible that none of these variables were as important as Shell’s need to address its financial position—and to indicate to the equity markets that Shell is being proactive in positioning itself for the future.

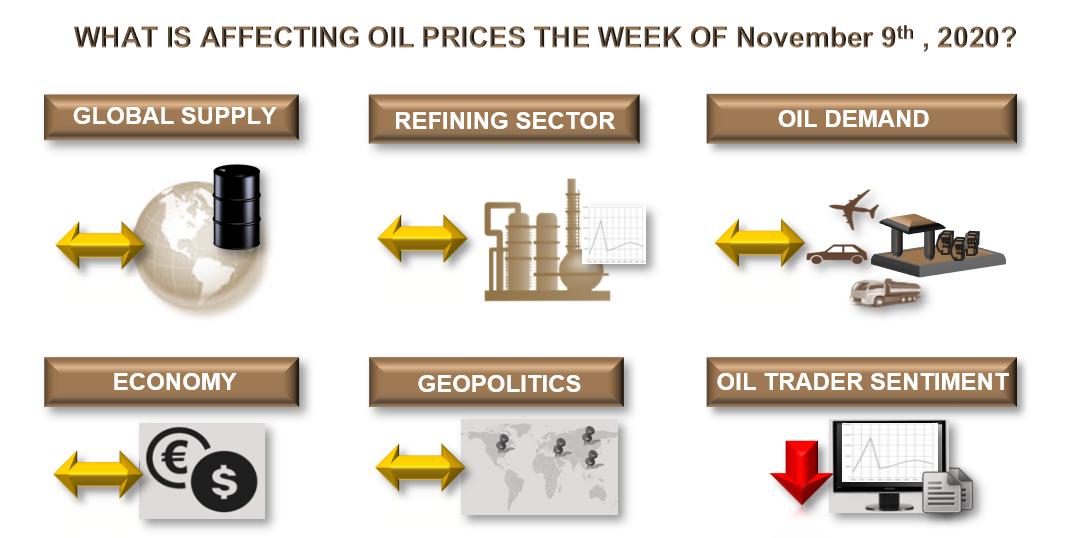

Global Supply—Neutral

Rumors about alleged conversations between Russia and Saudi Arabia prior to the upcoming OPEC+ meeting continued last week. This development is important because it would consolidate diverging views into a single approach—especially in light of Russia’s Energy Minister as a few weeks ago still signaling the intent to continue with the plan to pump more oil to markets as of January.

For the upcoming we expect this variable to be neutral with respect to oil prices.

Geopolitics—Neutral

There are reports of alleged Israeli incursions in Palestinian settlements that could create tension in the region, but considering the most recent agreements in between Israel and some Arab-countries (facilitated by the use of Israel pipeline that adds an option for reaching the Mediterranean market), such pressures will be less impactful than in the past.

We see this variable as neutral for this week.

Economy—Neutral

The U.S. unemployment rate continues to recover when compared to the large collapse seen in March. However, perceptions about the rest of the global economy vary.

We see the net impact of this variable as neutral for oil prices this week.

Oil Demand—Neutral

Oil consumption around the world is holding up despite the ongoing presence of COVID. U.S. demand continues to be strong for diesel, whereas gasoline remains within 90% of the five-year average range.

Asian demand has recovered in general except for jet fuel. Cold-weather conditions in northern Japan have recently underpinned kerosene consumption, which lends support to distillate spreads in general.

For the upcoming week, we expect this variable to be neutral.

Refining sector—Neutral

After the decline in crude prices during the last days of October, prices recovered ground last week, which negatively impacted refining margins across all the regions. From a wider perspective, refining margins have remained to hover in a relatively stable range over the last six weeks.

For the upcoming week expect this variable to have a neutral impact on oil prices.

Oil Trader Sentiment—Negative

Open interest for all relevant oil contracts increased last week, which reflects that participants are being attracted to take additional positions for both crude and products, in order to leverage the upcoming OPEC+ announcements, as well as seasonal patterns and potential developments with regards to a COVID vaccine.

For the upcoming week, we expect oil trader sentiment to be a negative variable for oil prices.

About the Author:

Jaime Brito is vice president at Stratas Advisors with over 24 years of experience on refining economics and market strategies for the oil industry. He is responsible for managing the refining and crude-related services, as well as completing consulting.

Recommended Reading

NextDecade Appoints Former Exxon Mobil Executive Tarik Skeik as COO

2024-07-25 - Tarik Skeik will take up NextDecade's COO reins roughly two months after the company disclosed it had doubts about remaining a “going concern.”

Silver Hill Closes Fourth Oil, Gas Fund with $1.13B in Commitments

2024-07-31 - Silver Hill’s portfolio consists of operations across 55,000 net acres in East Texas and North Louisiana and 86,000 net acres in North Dakota.

Chevron Moving HQ, CEO from California to Houston

2024-08-02 - Chevron Chairman and CEO Mike Wirth and Vice Chairman Mark Nelson will relocate to Houston, where much of Chevron’s other top leadership is already based.

LSB Industries’ Chairman of Board Retires, Replaced by CEO

2024-08-15 - Richard Roedel, LSB Industries Inc.’s chairman of the board of directors, is retiring from his position effective immediately.

SPATCO Energy Exits RF Investment Fund

2024-08-15 - RF investment Partners said it invested in SPATCO Energy Solution’s $230 million continuation fund, which was led by Kian Capital Partners and Apogem Capital.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.