Stratas Advisors does not expect any announcement of an increase in supply at the upcoming OPEC+ meeting scheduled for Dec. 4. Instead, Stratas expects that OPEC+ will continue with a strategy to protect a $90 oil price, the firm wrote in its latest oil price forecast. (Source: Shutterstock.com)

Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

The price of Brent crude ended the week at $83.63 after closing the previous week at $87.74. The price of WTI ended the week at $76.28 after closing the previous week $80.11.

We continue to hold to our view that we initially put forward in early October that the price of Brent crude will average around $90 during the fourth quarter of this year. Additionally, we expect that the price of Brent crude will remain, for the most part, in the channel between $85 and $95 because of upside resistance coupled with downside support. We do not see any development on the horizon that changes our view.

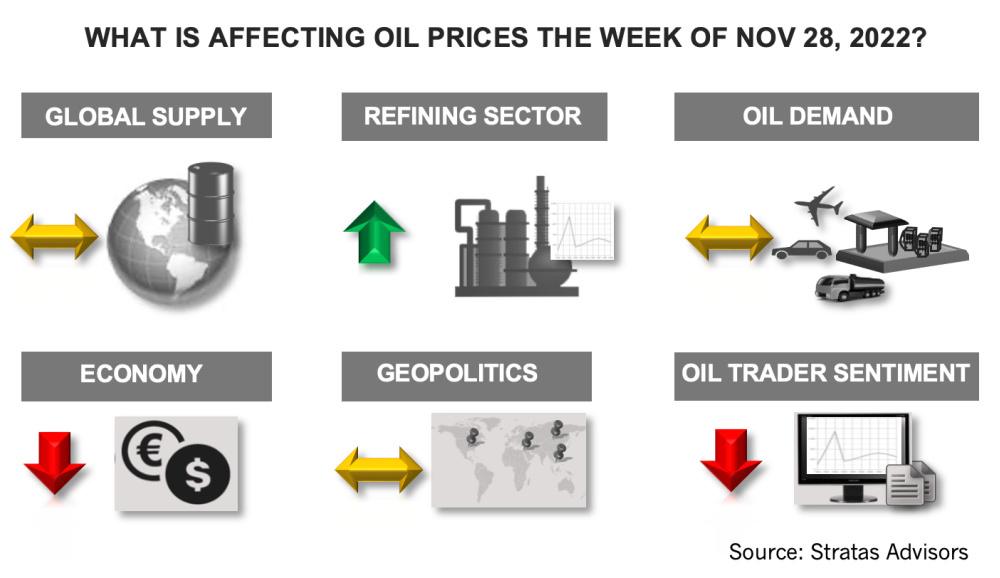

- As part of this forecast is the expectation that OPEC+ will continue to manage supply to align with demand considering the production capabilities of OPEC+ members. The next OPEC+ meeting is scheduled for Dec. 4. At the beginning of last week there was some noise about members of OPEC+ considering a 500,000 bbl/d increase, but this was quickly knocked down by Saudi Arabia stating that the current cut of 2 million bbl/d by OPEC+ will remain until the end of 2023. We do not expect any announcement of an increase in supply at the upcoming meeting. Instead, we are expecting that OPEC+ will continue with a strategy to protect a $90 oil price.

- Over the weekend, a geopolitical development that has direct impact on the oil market occurred with the Biden Administration easing some of the oil-related sanctions on Venezuela, which will allow Chevron to initiate limited oil production in Venezuela. We are expecting that the impact on the oil markets—especially in the short-term—will have limited impact and any substantial increase in production will require more time and more capital investments. In our view, the action by the Biden Administration is as much about the concerns about the exodus of some seven-million people from Venezuela as concerns about oil supply.

- We have been putting forth the view for months that additional sanctions (including a price cap) on Russian oil exports will be of limited effectiveness; however, the possibility of additional sanctions creates uncertainty and the basis for a risk premium, which otherwise would not be part of oil prices. Recent reports indicate that Europe is considering a cap between $65/bbl and $70/bbl, which is not much below current market prices for Russian crude. The proposed price illustrates the dilemma faced by Europe and its allies in that sanctions that will actually impact Russia’s oil exports are likely to have a major negative impact on the economies of Europe as well as the global economy.

- In our latest quarterly update of our global outlook for the oil markets, we are forecasting that global oil demand in the fourth quarter will increase by 1.1 million bbl/d in comparison to the third quarter. On average, we are forecasting that global demand will increase by 2.2 million bbl/d in 2022 and 2.55 million bbl/d in 2023.

With respect to this week, we are expecting that oil prices will stabilize with oil getting close to being oversold and oil traders significantly reducing their net long positions in the previous week.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Gulfport Energy to Offer $500MM Senior Notes Due 2029

2024-09-03 - Gulfport Energy Corp. also commenced a tender offer to purchase for cash its 8.0% senior notes due 2026.

ONEOK Offers $7B in Notes to Fund EnLink, Medallion Midstream Deals

2024-09-11 - ONEOK intends to use the proceeds to fund its previously announced acquisition of Global Infrastructure Partners’ interest in midstream companies EnLink and Medallion.

Kosmos to Repay Debt with $500MM Senior Notes Offer

2024-09-11 - Kosmos Energy’s offering will be used to fund a portion of its 7.125% senior notes due 2026, 7.750% senior notes due 2027 and 7.500% senior notes due 2028.

Upstream, Midstream Dividends Declared in the Week of July 8, 2024

2024-07-11 - Here is a selection of upstream and midstream dividends declared in the week of July 8.

Solaris Stock Jumps 40% On $200MM Acquisition of Distributed Power Provider

2024-07-11 - With the acquisition of distributed power provider Mobile Energy Rentals, oilfield services player Solaris sees opportunity to grow in industries outside of the oil patch—data centers, in particular.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.