Members of OPEC+ are maintaining adherence to the agreed framework and U.S. shale producers have kept production essentially unchanged since the middle of last year, even with the recovery in oil demand and prices. (Source: Shutterstock.com)

[Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

The price of Brent crude oil ended the week at $66.44 after closing the previous week at $66.11. The price of Brent crude oil fell back on April 30 after reaching $68.05 the day before. The price of WTI had a similar path ending the week at $63.49 after closing the previous week at $62.14 and reaching $65.01 on April 29.

The price movement is somewhat reflective of the differences in the pace of recovery being seen across the world. The U.S. economy continues to show signs of a robust recovery with growth for the first quarter being reported at 6.4% on an annualized basis. The growth was underpinned, in part, by the strength of the consumers and pent-up demand and the means to address the demand. During the first quarter, consumers increased spending by 10.7%. The strength of the consumer was further illustrated by the savings rate jumping to 21% from 12% in fourth-quarter 2020. In contrast, the economies of the Eurozone fell back into recession with its largest economy—Germany—declining by 1.7% with respect to fourth-quarter 2020.

There remains the concern of inflation in the U.S. and the risk that the Federal Reserve will need to tighten and to raise interest rates much sooner than expected. We still hold that this risk has been overhyped. There is no doubt that prices of commodities have increased, and that prices of material and finished goods are increasing. However, we hold that the price increases are the result in the mismatch in demand and supply, stemming from an accelerating demand associated with the reopening of economies, which has not been fully met by supply because of lags in investment and issues across supply chains. As such, the lag in supply will be naturally resolved by typical market forces. Therefore, raising rates and stifling economic recovery does not seem to be the appropriate policy remedy—and one we do not think the Federal Reserve will take any time soon.

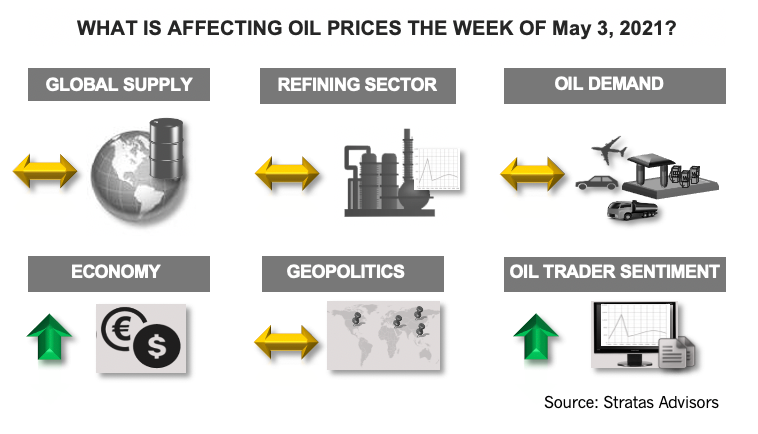

The supply/demand fundamentals for oil continue to look solid. From a supply perspective, members of OPEC+ are maintaining adherence to the agreed framework, and U.S. shale producers have kept production essentially unchanged since the middle of last year, even with the recovery in oil demand and prices. From a demand perspective, the U.S. is on pace to return to pre-COVID levels in the third quarter of the year. There is some risk associated with European demand if the projected recovery in Europe demand does not come into fruition. While the risk associated with COVID-19 is being diminished with the rollout of the vaccines ramping up, the risk associated with a lack of sufficient fiscal and monetary support still exists. Obviously, there are also demand risks associated with India. At this time, we are expecting that the downturn in Indian demand will last at least one more month, and that the impact in demand could be in the range of 600,000 bbl/d. On this basis, global demand for second-quarter 2021 would average some 300,000 bbl/d less than our current forecast. However, even with this reduction, we expect the demand growth to outpace the supply growth.

About the Author:

John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Optimizing Direct Air Capture Similar to Recovering Spilled Wine

2024-09-20 - Direct air capture technologies are technically and financially challenging, but efforts are underway to change that.

Offshore Guyana: ‘The Place to Spend Money’

2024-07-09 - Exxon Mobil, Hess and CNOOC are prepared to pump as much as $105 billion into the vast potential of the Stabroek Block.

Endeavor Energy Founder Autry Stephens Dies at 86

2024-08-16 - Stephens created a legacy in the Permian Basin that Endeavor said will continue to shape the future of the company.

Superior Sees Executive Leadership Changes

2024-08-15 - Superior Energy Services’ president, CEO and chairman Brian Moore is retiring, and his roles are to be split between the two people succeeding him.

CEO: Baker Hughes Lands $3.5B in New Contracts in ‘Age of Gas’

2024-07-26 - Baker Hughes revised down its global upstream spending outlook for the year due to “North American softness” with oil activity recovery in second half unlikely to materialize, President and CEO Lorenzo Simonelli said.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.