Key Points: Bloomberg scrapes show us that gas field production was lower by a bit more than 190 million cubic feet per day (MMcf/d) or nearly 1.3 billion cubic feet (Bcf) for the week. Demand fell in all major categories (4.6 Bcf/d or 32.2 Bcf for the week), even as export market flows to Mexico grew by 0.04 Bcf/d. Canadian imports also rose by 0.08 Bcf/d.

Based on our analysis, we expect the U.S. Energy Information Administration (EIA) to report a 137 Bcf withdrawal for the report week ended March 1 (a pull on par with the five-year average value of 130 Bcf and a consensus whisper expectation of 140 Bcf).

Natural gas markets have been volatile this winter. The colder-than-usual November and the low natural gas inventories entering winter had caused natural gas prices to reach $4.50 per million British thermal units (MMBtu). We note that the natural gas futures prices for April are staying below $3/MMBtu. However, the spot prices at Henry Hub have reached $4.25/MMBtu as of March 4 this week. That’s been a good run, and from this level, we think the forward outlook is more neutral than positive.

Lastly, by the end of winter’s heating season on March 31, we do not expect the winter exit storage to dip below 1,145 Bcf given current expectations for LNG export flows and normal withdrawals for the remaining four weeks of winter.

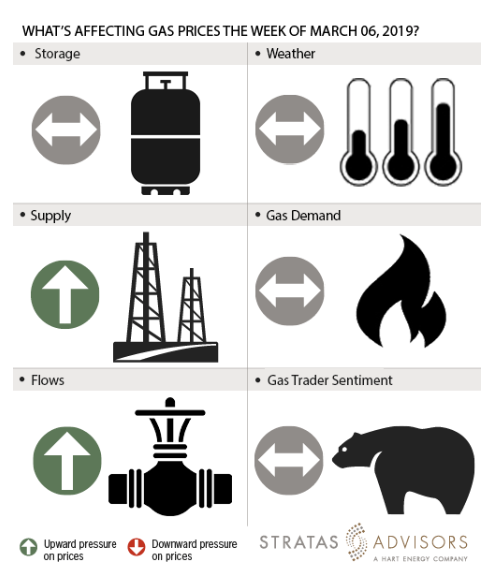

Storage: Neutral

We estimate a storage withdrawal of 137 Bcf will be reported by EIA this week for the week ended March 1. This value is comparable to the five-year average value of 130 Bcf. The classic withdrawal season is coming to an end on March 31 and if we see normal withdrawals over the entire period, we do not expect the inventory levels to fall below 1.1 Tcf. If severe weather lasts beyond March then it is possible that withdrawals continue after March 31 as well. But that situation appears unlikely as NOAA temperature forecasts already indicate a warming trend. All in, we see storage changes being a neutral driver for gas prices this week.

Weather: Neutral

Heating demand appears to have weakened given that we are close to the end of the winter season. Along with that, NOAA’s eight-to-14-day short term temperature forecasts to March 14 shows that warmer temperatures will prevail through the populous regions of Texas and areas east of the Mississippi River while temperatures should remain below normal over the Midwest and less-populous Rockies and low-gas demand centers on the West Coast. Accordingly, we see weather as being a neutral driver for gas prices this week.

Supply: Positive

Average dry gas production fell to 85.07 Bcf/d for the report week vs. 85.26 Bcf/d in the prior week. We believe this decrease could be related to freeze-offs in West Texas. Winter weather that moved in over the weekend has been impacting performance in the Permian according to press reports citing freeze-offs. All in, we expect supply dynamics will offer positive pressure to this week’s price activity.

Demand: Neutral

Although demand fell in all major categories for the report week ended March 1, we infer from Bloomberg data that the demand is going to increase for the current week. For the first three days of the current week, demand from industrial, power generation and residential/commercial factors is higher by 10 Bcf/d when compared to the same period of the report week. We believe that the bearish decrease in demand for the report week should be seen in light of the bullish increase in demand for the current week. So we see a neutral effect from demand-side drivers.

Flows: Positive

The upset conditions continue in the Pacific Northwest resulting from the outage at the Enbridge Westcoast natural gas pipeline system that shut off flows on one of the two pipeline paths supplying Washington State. Pricing agencies and media reports are showing that border region natural gas spot prices at Sumas, Wash., have reached $200/MMBtu. Prices quickly dropped back to $16/MMBtu but still remain highest in the country, and that is pulling gas from the Rockies and supporting gas prices in the Western U.S. and Canadian gas markets this week.

Trader Sentiment: Neutral

Despite the U.S. Federal Government shutdown being over, it is expected that the data reports by the Commodity Futures Trading Commission (CFTC) will show only lagging data until March 8. We will resume our analytical coverage of CFTC data when the agency resumes reporting CFTC data that are contemporaneous with the other data in these weekly analyses. Accordingly, we expect the trader sentiment to be neutral for the report week.

Recommended Reading

Chevron Launches New Hydraulic Fluid for Marine, Construction Use

2024-09-10 - Chevron said its Clarity Bio EliteSyn AW hydraulic fluid meets or exceeds the biodegradation, toxicity and bioaccumulation limits set by government regulations.

No Good Vibrations: Neo Oiltools’ Solution to Vibrational Drilling Problems

2024-09-10 - Vibrations cause plenty of costly issues when drilling downhole, but Neo Oiltool’s NeoTork combats these issues, enhancing efficiency and reducing costs.

International, Tech Drive NOV’s 2Q Growth Amid US E&P Headwinds

2024-07-29 - Despite a U.S. drilling slowdown, slightly offset by Permian Basin activity, NOV saw overall second-quarter revenue grow by 6%, although second-half 2024 challenges remain in North America.

Drowning in Produced Water: E&Ps Seek Economic Ways to Handle Water Surge

2024-07-01 - Strained disposal limits push beneficial reuse to the forefront for produced water management.

TGS Awarded 2D Survey in the Sumatra Basin

2024-09-09 - TGS’ Sumatra Basin seismic acquisition is expected to be completed by the end of 2024.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.