Bloomberg scrapes imply gas field production was 940 MMcf/d lower when compared to the past week, but imports from Canada increased by 1.16 Bcf while Mexico exports also increased by 1.08 Bcf.

Our analysis leads us to expect the EIA to report later this week that there was a 222 Bcf withdrawal for the week ended Jan. 25 (higher than the current 191 Bcf whisper consensus withdrawal expectation and higher than the five-year average withdrawal of 154 Bcf)

The report week started on a quiet note on the demand side due to Monday being a holiday in the U.S. (Martin Luther King Day). Between then and now, natural gas prices have been declining even despite withdrawals increasing and production decreasing marginally. Storage levels, which at winter’s start were at their historical lowest, now falls within five-year average levels and are actually above year ago levels. Consistently high production and above normal winter temperature forecasts have been reassuring to market participants and are suggestive that gas storage will not run dry before end of winter.

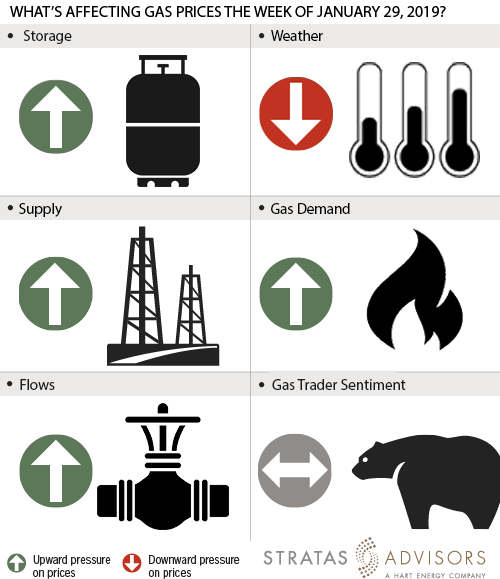

Supply: Positive

Average field supply has decreased slightly for the week ended Jan. 25. The weekly average dry gas production increased from 85.14 Bcf/d to 84.19 Bcf/d. There were no reported freeze-offs or delayed LNG import deliveries this week. But we think freeze-offs may be coming to Appalachia later this week which will show up in next week’s report. Accordingly, supply will likely offer a slightly positive pressure to this week’s price activity.

Weather: Negative

Natural gas prices have taken a downfall due to forecasts of warm weather prevailing in February. While a polar vortex is settling in the upper Midwest currently, storage appears ample to handle this demand and the latest 6-10 day NOAA forecasts show a warming trend for the Midwestern consuming area. Natural gas prices as of press time today are at $3.06/MMBtu. The highest spot prices for the month of January has been $3.61/MMBtu. We expect weather to offer a negative pressure to this week’s price activity. Future trading prices for February has fallen to $2.95/MMBtu.

Trader Sentiment: Neutral

The CFTC Jan. 18 Commitment of Traders data is unavailable due to government shutdown. We believe the trader sentiment will be neutral for this week’s natural gas market.

Storage: Positive

We estimate a storage withdrawal of 222 Bcf will be reported by EIA this week for the week ended Jan 25. In our prior forecast, we estimated a gas withdrawal of 76 Bcf for the week ended Jan. 11, which was in-line with the consensus at that time. We were close to the actual value of 81 Bcf. Our 222 Bcf withdrawal expectation for this week is higher than the five-year average value of 154 Bcf for the same week. At over 200 Bcf of withdraw, This week’s report is likely to be one of the largest of the season. We see storage changes as positive driver this week.

Demand: Positive

The cold front during the past week has resulted in higher residential and commercial than previous week. Week-on-week, the average residential and commercial demand has risen by a whopping 7.07 Bcf/d or 49 Bcf. The power generation and industrial use demand marginally increased by 1.5 Bcf/d or 10.5 Bcf. Accordingly, we think that demand will offer a positive effect on the prices this week. This strong winter-related demand growth is being followed by another vortex this week with temperatures expected to reach in the minus-50 Fahrenheit range in the upper Midwestern population centers around Minneapolis through Chicago.

Flows: Positive

We see Flows as a potential positive driver for prices this week because of the pipeline explosion in Ohio that is currently disrupting normal supply flows in the region. A 30-in. natural gas pipeline belonging to the Texas Eastern system burst in Ohio on Jan. 21. The operators restarted the pipeline in the reverse direction to serve customers in Kentucky and Tennessee.

Recommended Reading

Permian’s LandBridge Prices IPO Below Range at $17/Share, Raising $247MM

2024-06-30 - Houston-based LandBridge, which manages some 220,000 surface acres in the Permian Basin, kicked off trading at $19 per share, more than 10% above its listing price.

Steve Gray to Retire from Range Resources’ Board

2024-08-26 - Steve Gray, a member of Range Resources Corp.’s board of directors since 2018, will depart on Oct. 1.

Offshore Guyana: ‘The Place to Spend Money’

2024-07-09 - Exxon Mobil, Hess and CNOOC are prepared to pump as much as $105 billion into the vast potential of the Stabroek Block.

Liberty Energy Warns of ‘Softer’ E&P Activity to Finish 2024

2024-07-18 - Service company Liberty Energy Inc. upped its EBITDA 12% quarter over quarter but sees signs of slowing drilling activity and completions in the second half of the year.

Chevron Moving HQ, CEO from California to Houston

2024-08-02 - Chevron Chairman and CEO Mike Wirth and Vice Chairman Mark Nelson will relocate to Houston, where much of Chevron’s other top leadership is already based.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.