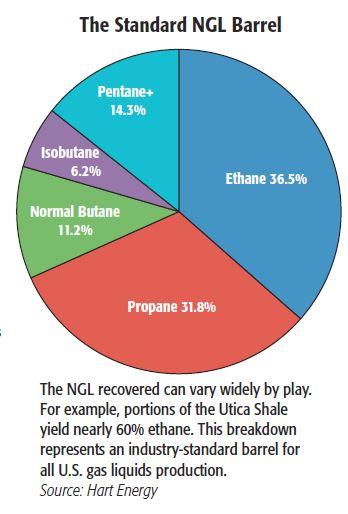

The shale boom blessed the U.S. with abundant, and unexpected, flows of crude oil and natural gas. The unconventional plays also supplied abundant new production of those middling, not quite a gas-not quite a liquid hydrocarbons lumped together as gas liquids, or NGL.

Question: What to do with them?

Answer: Almost anything you want.

Ethane, propane, normal and isobutane, and condensate provide the indispensable petrochemical building blocks that make modern life possible. Without them, society would be chopping down trees, quarrying rocks and shearing sheep to create vital items needed for everyday life. The plastics and scores of petrochemicals produced from NGL appear everywhere.

Look around you now and you’ll see lots of NGL-based polyethylene, polypropylene, polystyrene, polymethyl methacrylate—and who knows what else. Even the clothes you have on probably contain cloth woven from fibers of Dacron, polyester or nylon. Need to drive somewhere? Your vehicle’s fuel will contain NGL, and the ethylene glycol in its radiator keeps the cooling system safe from freezing on cold winter nights.

All this can be overwhelming; maybe you feel a headache coming on so you reach for a bottle (made of high-density polyethylene) filled with ibuprofen pills. Ibuprofen? That’s C13H18O2, and yet another NGL-based petrochemical. Modern chemistry can snip a carbon atom here, add an OH radical there, and create useful products that do all sorts of things.

Big and bigger

NGL and the petrochemicals created from them are a big U.S. business that’s about to get bigger. Their impact on the midstream already has been major. For ethane alone, “the combined new cracking capacity and new exports could total half-million barrels per day [bbl/d] of new demand,” Anthony Scott, managing director of analytics and consulting for BTU Analytics, told Midstream Business. The U.S. Energy Information Administration (EIA) estimated domestic ethane demand averaged 1.1 million barrels per day (MMbbl/d) in 2016 and predicted it will rise to 1.21 MMbbl/d for 2017. Next year, the EIA projected in its most recent Short-Term Energy Outlook that U.S. ethane demand will hit 1.4 MMbbl/d. Stratas Advisors projected that by 2025, U.S. ethane crackers could require around 1.9 MMbbl/d.

Scott said BTU Analytics sees these favorable trends in the NGL sector:

• Increased production and stagnant domestic demand has resulted in growing exports to balance the market—as well as ethane rejection into the natural gas stream.

• New ethane demand from large greenfield crackers, as well as international exports, is imminent, and will provide price uplift above the natural gas floor over the next few years.

• U.S. LPG is increasingly exported, aided by new terminal capacity.

• NGL production from the Appalachian plays will continue to grow and now makes up about 20% of U.S. NGL production.

Rising prices

Rising demand will cause NGL prices to increase 32% during 2017, joining an upswing in crude oil (27%) and natural gas (34%), according to Mizuho Securities USA Inc. However, ethane prices fell sharply as the year began with scheduled turnarounds at three steam crackers. Mizuho’s forecast is based on assumptions of higher oil prices—which will impact the price of naphtha, an alternative petrochemical feedstock— and rising ethane demand growth from the petrochemical sector. Mizuho cited S&P Global Platts analytics, which projects ethane demand growth to increase 15% year-over-year to 1.2 MMbbl/d.

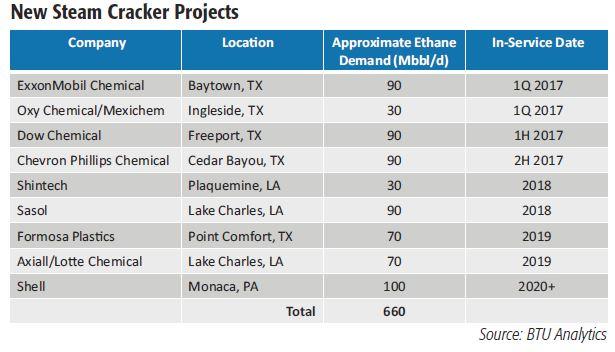

In its recent report, “Top 10 Upstream & Midstream Energy Themes in 2017,” Mizuho mentioned five Gulf Coast petrochemical plants expected to be in service in late-2016 and through 2017 that will add 333,000 bbl/d of ethane consumption. Through 2022, a total of 11 plants will boost demand by 763,000 bbl/d, it said.

Yet with their multiple uses and markets, NGL usually amount to an upstream afterthought, noted Jennifer Van Dinter, manager of NGL analytics for S&P Global’s Platts Analytics unit.

“We have a chance for even more growth in supply, and we’re going to have to figure out what we’re going to do with it,” Van Dinter told Midstream Business. “Most of the time, producers are not targeting NGL; they’re going after gas or they’re going after oil. But NGL are something you have to deal with. You’re not making the decision to go after them—but they’re going to come anyway. It’s something we all have to think about and we have to find a way to utilize them in the most productive and efficient ways.”

That swelling tide of new NGL in the last decade as the shale gale whirled up caught the industry off guard and NGL prices plummeted, particularly for ethane. Those low prices caught the eye of petrochemical firms who saw wide differentials between gas liquids and naphtha as a profit-making opportunity. 2011 and 2012 had multiple announcements for new stream cracking plants that convert ethane into the olefin ethylene, the feedstock for polyethylene, one of the most common plastics around that’s used to make milk jugs, combs, shampoo bottles, grocery sacks and who knows what else.

RBN Energy estimated in a recent report that some 1.8 MMbbl/d of feedstocks flow into ethane crackers. Feedstocks costs can vary, as well as a plant’s ability to switch between ethane, propane, butane or naphtha for its furnaces.

Widening the margin

“And every day, decisions are made for each steam cracker on which feedstock—or mix of them—would provide the plant’s owner with the highest margins,” the report added. “Within each petchem company, these decisions are optimized by staffs of analysts and technicians using sophisticated and complex mathematical models that consider every nuance of a specific ethylene plants’ physical capabilities.”

Feedstock cost is critical since the polyethylene pellets used to make all those consumer products are a commodity. And the big advantage U.S. cracking plants enjoy with ethane is the low-cost feedstock in the world right now.

Many of those multibillion dollar plants announced five or six years ago are nearing completion in the next few months, a “first wave,” as some industry observers call it, of new steam cracking capacity. Together, they will have a significant impact on the energy and petrochemical industries, according to Kendall Puig, director of research at East Daley Capital, who tracks NGL trends for the research firm.

“Everyone’s looking at the upcoming petrochemical buildout, and the thing to watch is that some of these projects continue to be pushed back and delayed,” Puig told Midstream Business. “The growth may be more gradual than many people expected as they have been pushed back to the end of 2017 and into 2018.

“These are not economic delays,” she noted. “There were delays in Louisiana, for example, due to weather and general employment delays.” Skilled welders, pipefitters and other crafts were scarce around the Gulf Coast. “This whole buildout is happening in a pretty small area, and it has affected the labor force there.”

Close by the new crackers are Cheniere’s still unfinished Sabine Pass LNG terminal, other LNG projects and buildouts of related midstream infrastructure, including pipelines, fractionators and terminals. Also, new NGL export facilities have gone in, such as the recently expanded Morgan’s Point terminal on the Houston Ship Channel operated by Enterprise Products Partners LP. Enterprise added the ability to handle refrigerated ethane last year to its growing volumes of propane and butane exports.

The outlier

The bulk of the new cracking capacity will go onstream within the energy industry’s Gulf Coast hub with one notable exception: Shell’s new cracker will be the outlier, to be built outside Pittsburgh. It also will be the largest of the active projects, requiring 100,000 bbl/d of ethane when it enters service, maybe in 2020. Timing is yet to be determined, Royal Dutch Shell Plc CEO Ben van Beurden told investors in February.

“We are still working our way through some of the permits that we need to have, but that’s just the normal state of affairs that you will have in any project. But I think by the end of the year, certainly in 2018, we will be in significant investment mode. We haven’t announced exactly when it will start up, but expect that to be not any more this decade because it is a very large greenfield project.”

A “second wave” of greenfield crackers could include an Ohio plant. PTT Global Chemical told state authorities in January it will make a final investment decision by the end of March on a Belmont County, Ohio, location—across the Ohio River from Wheeling, W.Va.

BTU Analytics  counts nine ethane crackers under construction in the U.S. currently with the first two scheduled to enter service in first-quarter 2017. ExxonMobil Chemical is putting the finishing touches on a plant at Baytown, Texas, that will require 90,000 bbl/d of feedstock. Oxy Chemical and Mexichem are closing in on the start-up of a 30,000 bbl/d cracker at Ingleside, Texas, also scheduled for the first quarter.

counts nine ethane crackers under construction in the U.S. currently with the first two scheduled to enter service in first-quarter 2017. ExxonMobil Chemical is putting the finishing touches on a plant at Baytown, Texas, that will require 90,000 bbl/d of feedstock. Oxy Chemical and Mexichem are closing in on the start-up of a 30,000 bbl/d cracker at Ingleside, Texas, also scheduled for the first quarter.

There may be more cracking capacity in that second wave coming later, Greg Haas, director of inte-grated oil and gas for Hart Energy’s Stratas Advisors, told Midstream Business. “We have 20 projects on our list but some of them will never happen,” he added. At this point it’s not clear which will get built and which will be shelved.

“We’re probably over-announcing ethylene plants and we’re under-recovering ethane right now, but soon the ethane plants will come online and soon more recovery will be made from de-ethanizers,” Haas said.

The other new ethane market has been exports. Creation of a seaborne ethane business from scratch took a while—compared to pipeline exports to feed Canada’s Nova Chemical complex in Ontario via Sunoco Logistics’ Mariner West system—but finally got underway in early 2016. INEOS, a dominant player in Europe’s petrochemical industry, converted steam crackers in Norway and Scotland to ethane from naphtha and began exporting from Sunoco’s Marcus Hook terminal outside Philadelphia.

On the Texas coast, Enterprise Products Partners began ethane exports from Morgan’s Point later in 2015, serving three crackers in India operated by Reliance Industries Ltd.

The crude uptick

Current NGL production causes concern by some analysts since overall oil and gas production has declined due to the drop in commodity prices. But an uptick in crude production, with its NGL-rich associated gas, is helping things. “Perhaps by the time the second wave of ethane construction is com-pleted, the recovery of wet gas production will have happened and we will be at much higher levels,” Haas said.

“We’re seeing a lot of associated gas production in the Permian, and it’s coming on at the right time,” Scott noted.

“Wet gas output will underperform prior peaks for a few years, but ethane will not follow suit,” Haas added. “Lower wet gas supply does slow ethane growth, but recall we are rejecting several hundred thousand barrels of ethane per day because the economics aren’t right. We expect rejection of uneconomic ethane to persist even amid falling wet gas output. But as demand and exports rise, more profitable recovery from processing plants and de-ethanizers will boost ethane volumes pretty nicely.”

Van Dinter agreed. “We’re seeing that the liquids content in the gas in a lot of regions that we focus on has been a little bit higher than we were anticipating. So the question, ultimately, is will that be sustainable? This gives us a bit of a cushion going into 2017. We don’t feel like it will be as tight of a market as we thought it might be 18 months or two years ago.”

Those plants coming on now received a go-ahead because of the attractive spread between the price of naphtha, based on crude oil, and ethane, based on natural gas, a spread that narrowed sharply during the commodity price drop that started in late 2014.

“But the ethane margin has strengthened again,” Van Dinter added. “There’s competition, worldwide, between naphtha crackers overseas vs. ethane crackers in the U.S. We’re seeing ethane going back into the lead right now in terms of the cracking margin.”

Propane and more

Ethane isn’t the only NGL story, of course. Propane, along with both normal and isobutane, has been in greater supply and has found new markets—particularly abroad. The U.S. has become a significant propane exporter.

Ethane isn’t the only NGL story, of course. Propane, along with both normal and isobutane, has been in greater supply and has found new markets—particularly abroad. The U.S. has become a significant propane exporter.

“We’re seeing 1 million barrels per day of propane exports now; that’s not a trivial amount at all,” Van Dinter said.

Besides its use as a cooking and motor fuel, propane—like its ethane cousin—has substantial petrochemical demand. Propane can be an alternative in producing ethylene, as well as source of propylene and multiple other olefins.

A ramp-up in export terminal capacity may have hit a lull, according to Haas. “For some time, we have been indicating we may be overbuilt on send-out capacity for LPG exports through marine terminals,” he said. “We have a lot of capacity in propane and butane exports, and we’ve built up some capacity of ethane exports. Then along came the price crash. Our bias is toward slightly lower propane exports because of tightening wet gas production and rising competition from the Middle East and elsewhere.”

Haas noted propane inventories are high and any modest increase in exports could be covered by a drawdown in stocks if NGL production remains flat or declines.

Petrochemical firms have been adding propane dehydrogenation (PDH) capacity, but there are indications that the niche may be overbuilt too. BASF postponed a proposed propylene plant at its Freeport, Texas, operation last year. However, Formosa Plastics and Enterprise Products are moving ahead with new PDH units.

PDH plants

Formosa’s PDH plant at Point  Comfort, Texas, was scheduled to go online as 2017 began. The 23,000-bbl/d plant will produce 1.32 billion pounds per year of propylene. Enterprise said in a recent investor presentation that it moved ahead after competing PDH projects were cancelled or indefinitely delayed. It told analysts that propylene supplies have declined as ethylene crackers have switched to ethane from propane, that international demand for propylene has created “attractive export opportunities” and that “low prices do not mean low margins in the propylene business; spreads do not necessarily contract.”

Comfort, Texas, was scheduled to go online as 2017 began. The 23,000-bbl/d plant will produce 1.32 billion pounds per year of propylene. Enterprise said in a recent investor presentation that it moved ahead after competing PDH projects were cancelled or indefinitely delayed. It told analysts that propylene supplies have declined as ethylene crackers have switched to ethane from propane, that international demand for propylene has created “attractive export opportunities” and that “low prices do not mean low margins in the propylene business; spreads do not necessarily contract.”

Its new PDH operation outside Houston will require 30,000 bbl/d of propane to produce 1.65 billion pounds per year of propylene. Commissioning has been schedule for the second quarter, the company said.

The butanes

Enterprise announced earlier this year it plans to construct a new  isobutene dehydrogenation (IBDH) unit at the Mont Belvieu, Texas, NGL hub that will have the capability to produce 425,000 tons per year of isobutylene. Start-up is expected in fourth-quarter 2019. The isobutylene produced by the plant will provide the feedstock to fill underutilized capacity at Enterprise’s existing downstream octane enhancement and petrochemical facilities, the firm said in the announcement.

isobutene dehydrogenation (IBDH) unit at the Mont Belvieu, Texas, NGL hub that will have the capability to produce 425,000 tons per year of isobutylene. Start-up is expected in fourth-quarter 2019. The isobutylene produced by the plant will provide the feedstock to fill underutilized capacity at Enterprise’s existing downstream octane enhancement and petrochemical facilities, the firm said in the announcement.

Enterprise told investors in a recent presentation that the new IBDH operation would provide “substantial growth in our butane value chain.”

Stratas Advisors noted in a recent report that balance, and sourcing, of normal and isobutane “are particularly complex.” It added that growth potential for the two NGL is more limited than that of ethane and propane.

In addition to providing feedstock for multiple petrochemicals and LP gas, butane sees significant demand for blending into winter-grade gasoline since butane’s quicker vaporization makes starting easier on cold winter mornings. Magellan Midstream Partners LP is among the midstream operators to pursue the butane blending business. It recently announced a joint venture (JV) with Colonial Pipeline, Powder Springs JV, that will provide butane blending at Colonial’s Atlanta petroleum products hub starting in early 2017. Another market for isobutane is as a refrigerant, backing out Freon due to environmental concerns.

Looking ahead

The new cracking capacity and growing exports give the NGL business, overall, a bright future—a decided improvement from the last several years of oversupply and weak pricing. Supply and demand finally may be coming into balance. But an important question lingers: Where will all that product go? Domestic consumption is likely to rise slightly and gasoline demand—and the related butane blending business— may actually decline.

The answer probably lies abroad. Take LPG, for example. It’s a popular motor and cooking fuel in many countries but not in the U.S.

“I think you can look at transitioning some vehicle fleets over to propane but it won’t happen overnight,” Van Dinter said. “In some cases you’ll need support from the government so that you have the infrastructure in place to make it economical.” She mentioned Japan and South Korea as two nations that make comparatively wide use of LPG to fuel cars and trucks.

Domestic use of LPG for cooking and heating is comparatively limited due to the nation’s extensive natural gas pipeline grid.

“2017 and 2018 are going to be critical years in terms of growth of petrochemical demand,” Van Dinter said. “We do see exports being an integral component in terms of the net LPG market. We don’t anticipate there is enough demand here to absorb all of the propane we’re going to produce. LPG exports overseas are continuing to move as well, that has been a big concern—if the world could absorb the propane and butane that the U.S. is producing.” There was pullback in exports last fall, “but recent numbers are looking at lot stronger.”

East Daley’s Puig also looks overseas for new markets.

“I think almost all of the incremental polyethylene from these new crackers is going to the export market, not the domestic market,” she said. “Asia and Latin America are the targets for that polyethylene. Demand in those regions is growing but not at the rate that’s needed. I think there will be a glut in the short term.”

The new U.S. cracking capacity faces competition from new Middle East plants, particularly in Saudi Arabia. “My understanding is that new capacity is using heavier NGL and naphtha. But it’s headed for the same export markets,” Puig added.

Haas suggested there may be new, underexplored markets that could be opened to U.S. petrochemical markets. For example, “once you have an ethane terminal, it’s not that hard to liquefy ethylene and export it.”

Van Dinter also pointed to developing nations that have great prospects as new NGL markets.

“Africa is a market that has not been tapped, but I don’t know if it’s ready to be developed yet,” she said. “And there are parts of Latin America where you could potentially expand exports of LPG.”

So what to do with NGL? We may not know all the answers yet.

Paul Hart can be reached at pdhart@hartenergy.com or 713-260-6427.

Recommended Reading

Baseline Energy Opens New Uinta Basin Power Generator Facility

2024-09-24 - Baseline Energy Services’ facility in the Uinta Basin plans to support the region’s mobile power generator fleet with a range of maintenance and repair services.

Quantum Backs Tug Hill Team in New E&P Vickery Energy

2024-09-24 - Quantum Capital Group is backing the executives behind Tug Hill, which sold to EQT Corp. for $5.2 billion, in a new Appalachian Basin company Vickery Energy Partners.

VTX Energy Quickly Ramps to 42,000 bbl/d in Southern Delaware Basin

2024-09-24 - VTX Energy’s founder was previously among the leadership that built and sold an adjacent southern Delaware operator, Brigham Resources, for $2.6 billion.

E&P Highlights: Sept. 23, 2024

2024-09-23 - Here's a roundup of the latest E&P headlines, including Turkey receiving its first floating LNG platform and a partnership between SLB and Aramco.

US Drillers Cut Oil, Gas Rigs for Fifth Week in Six, Baker Hughes Says

2024-09-20 - U.S. energy firms this week resumed cutting the number of oil and natural gas rigs after adding rigs last week.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.