Hart Energy

U.S. Silica Holdings Inc. (NYSE: SLCA) pulled the trigger on its second acquisition of the year with a sand producer in Texas and says it’s close to additional deals as the company takes advantage of its strong balance sheet during the downturn.

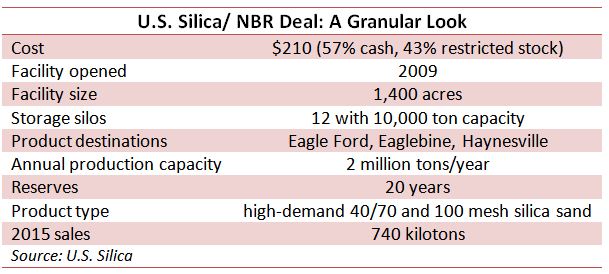

U.S. Silica said July 18 that it would buy the NBR Sand Unit from privately owned New Birmingham Inc. for $210 million. The price includes 57% cash and 43% restricted stock.

Located in Tyler, Texas, NBR has access to prolific shales within the state. It operates a single sand mine and plant that has the capacity to produce more than 2 million tons of fine-grade frack sand per year.

The East Texas facility currently sells its products free on board (FOB) to customers that primarily drill and complete wells in nearby basins.

It’s the second purchase by U.S. Silica in 2016. In May, the company completed the purchase of a fully permitted, 327-acre parcel of land adjacent to its silica sand mine and plant in Ottawa, Ill.

“NBR is just the kind of asset we’ve been patiently looking to acquire,” said Bryan Shinn, U.S. Silica’s president and CEO.

Shinn said that even though the NBR unit is a significant purchase for the company, “we’re not done with M&A by any means.”

Shinn said on a conference call that the company has a strong pipeline of additional opportunities.

“We like the Permian, parts of the Midcontinent and some things in the Northeast as well,” he said. “And we’ll continue to look for what I call ‘game changers’ in terms of technology.”

However, he warned that deals are often binary matters—they either happen or do not.

“Even though we’re fairly far along in discussions, you never know when it’s going to close or if it’s going to close,” he said. “I would certainly expect we’ll close additional opportunities here.”

The company expects the NBR acquisition to be accretive in 2016.

Tudor, Pickering, Holt & Co. (TPH) noted that NBR Sand started as a recreational sand producer for golf courses before realizing its sand was suitable for fracking.

“It’s an all-trucking operation [no rail] and the company improved its loadout and storage infrastructure in recent years,” TPH said. “It sits best positioned to sell into the Haynesville, Scoop/Stack and Eagle Ford. We continue to like frack sand pricing prospects in 2017 [and beyond].”

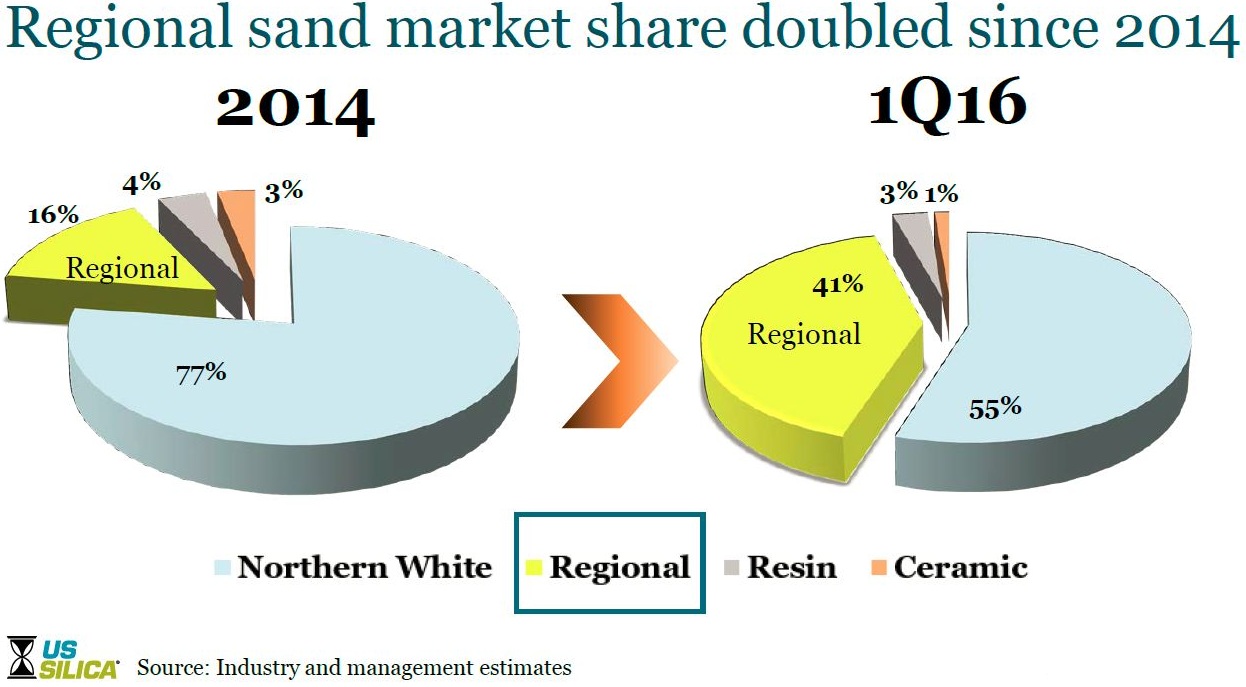

Shinn noted that the regional sand market has doubled since the downturn began in 2015.

“This acquisition squares up nicely with recent industry trends in which E&Ps are shifting their completion designs to more slickwater fluid systems that use fine-grade regional sand products,” he said.

Marc Bianchi, an analyst at Cowen and Co., said NBR is an attractive sand mine similar to the company’s Cadre mind. Shinn noted that unlike Cadre, rock won’t have to be pulverized to create sand, and Cadre’s production is a coarser grade. U.S. Silica acquired the 800 million tons per annum (mtpa) Cadre mine in July 2014 for a net $84 million. Shinn said NBR has the same potential but is twice as large.

“Lower-cost, finer-grade regional and brown sands are increasingly used in the Permian and a portion of Eagle Ford,” Bianchi said. “Post the NBR sand acquisition, SLCA will have 8.3 mtpa of white sand and 2.8 mtpa of regional/brown sand capacity.

Bianchi said that regional/brown sand is lower quality compared to white sand, though finer brown sand is increasingly used in Texas. However, he wasn’t convinced that a $14 per ton contribution margin was possible without additional information.

Brad Handler, and equity analyst for Jefferies, said that NBR’s upside is the potential synergies from logistics and expanding access to the Permian.

NBR Sand's mine-hours suggest activity is down 45% from its peak in fourth-quarter 2014.

“This is in contrast to total regional sand mine activity down just 4% from four-quarter 2014,” Handler said. “We believe this underperformance is due to the lack of access to Permian completion market as discussed above.”

The majority of other regional sand mines are within trucking distance of the Permian Basin.

Shinn, however, said during his press call that the company is acquiring low-cost assets that have been profitable through the cycle.

Once completely integrated into U.S. Silica's market-leading operating, sales and distribution platforms, the company expects to generate EPS accretion of 20 cents to 30 cents in 2017.

The NBR acquisition is expected to close in August following regulatory approvals, U.S. Silica said.

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Rice: EQT Walking the Walk on Natgas Emissions, Despite Politics

2024-09-20 - Methane emissions are falling in parts of the world as companies such as EQT, led by CEO Toby Rice, make strides to reduce emissions in their operations, although the task is not without challenges.

Romito: Beware the Environmental NGO ‘Emissions Police’

2024-08-22 - Non-governmental organizations are effectively functioning as an unchecked extension of the executive branch.

Startup Syzygy Sets Out to Shake Up Refining, Chemicals

2024-09-04 - Syzygy is developing combustion-free photoreactors that use light instead of heat as an energy source to produce zero- and low-emissions hydrogen and other chemicals.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.