U.S. shale players are focused on maintaining operational efficiency in oil and gas fields amid market uncertainty. (Source: Shutterstock.com)

Record low Henry Hub gas prices, the Coronavirus’ unexpected hit on global oil demand and persistent pressures from shareholders show the year is off to another rocky start for U.S. shale producers.

Rig counts have fallen along with completions activity in just about all U.S. land basins, except the Permian Basin, an implication of weaker frac activity, according to Artem Abramov, head of shale research for Rystad Energy.

In a webinar this week, he noted the number of active horizontal oil rigs fell by 25% last year with some liquid-rich basins laying down more rigs than others. Oklahoma, home of the SCOOP/STACK play, has seen its horizontal rig count fall by about 50% since August. However, he said, the Bakken, Denver-Julesburg and Eagle Ford “activity remains relatively close to the historical record levels.”

This comes as activity in the Permian sees capital flow into the oilier Northern Midland and Delaware New Mexico instead of the gassier Southern Midland and Western Delaware on the Texas side of the basin.

“We think 2020 will be quite a challenging year for the industry,” Abramov said. “There is a lot of uncertainty about what kind of activity guidance [and] capital guidance we’ll see from the companies. Despite that fact we believe that one thing is quite certain, this year will see continued focus of the industry on operational efficiency not necessarily productivity gains.”

Here’s a look at some of the trends Rystad Energy is seeing:

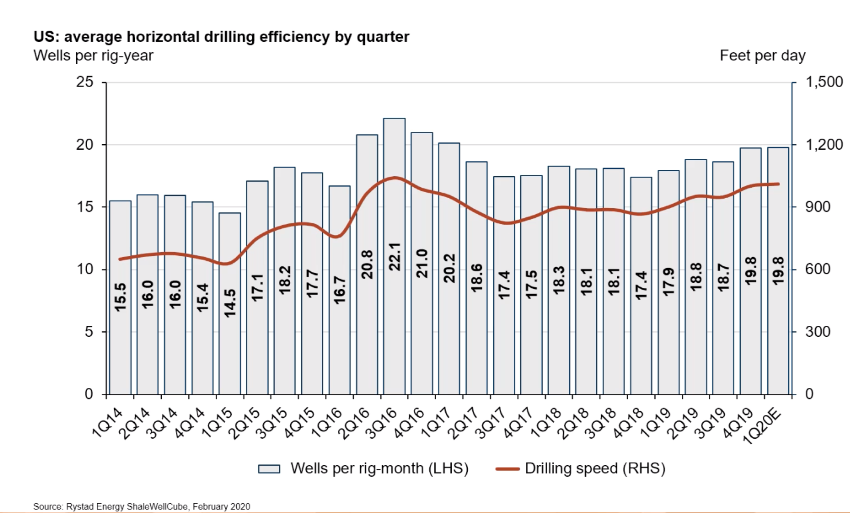

- Improved drilling efficiency with an average 1,000 feet being drilled per day in all basins, which reduces the number of rigs needed to drill the same number of wells for the same footage.

- More horizontal wells per pad as the Permian catches up to other basins. “Our expectation is we will see an increase in share of large-scale projects,” Abramov said. “One of the drivers behind this fundamental improvement in the drilling efficiency is continued increase in the share of pad drilling and also the increase in average pad size, average project size.”

- Preference for pure slickwater jobs over hybrid and gel-based continues to grow, accounting for nearly 70% as of late 2019. That’s up from 53% in fourth-quarter 2018.

- Zipper fracture stimulation dominance, representing more than 80% of the market.

However, Abramov said simultaneous fracs (simul-frac) could drive further completion efficiency this year. Stimulation via simultaneous operations allows frac fluid to be redirected with little downtime between a new wellbore and one that has just been fractured, he explained.

Early pioneers of simul-frac are “quoting average frac speeds exceeding 3,000 ft of lateral per day even with very intensive completions,” he said. “In many cases, they are able to pump fluids downhole [at] a rate of 140-160 barrels per minute and almost without downtime.”

QEP Resources Inc. is among the companies using the technique and seeing benefits in the Northern Midland Basin. The company averaged 4.2 million pounds of frac sand per day in 2018-2019 with an average completion speed of 2,583 lateral feet per day, he said, compared to a couple of other operators with 1,378 and 1,130 lateral feet per day, respectively. QEP’s average D&C cost per perforated lateral foot was $641, which Rystad said was the lowest in the Midland sub-basin.

“It is a big gain,” Abramov said. “Ultimately, all of these things lead to capital efficiency because you’re able on a per well basis you are able to achieve lower cost per foot.”

Recommended Reading

Beyond Energy: EnergyNet Expands Marketplace For Land, Real Assets

2024-09-03 - A pioneer in facilitating online oil and gas A&D transactions, EnergyNet is expanding its reach into surface land, renewables and other asset classes.

Weatherford Announces Acquisition of Technology Company Datagration

2024-09-03 - The acquisition gives Weatherford International digital offerings for production and asset optimization and demonstrates its commitment to continuously driving innovation across its technology portfolio, the company said.

Voyager Midstream Buys Haynesville G&P Assets from Phillips 66

2024-09-03 - Voyager Midstream acquired about 550 miles of natural gas pipelines, 400 MMcf/d of gas processing capacity and 12,000 bbl/d of NGL production capacity.

DNO Buys Stakes in Five Norwegian Sea Fields from Vår Energi

2024-09-03 - DNO’s acquisition of stakes from Vår Energi includes interests in four producing fields—Norne, Skuld, Urd and Marulk— and the Verdande development.

Transocean Scores $232MM Contract for Deepwater Atlas

2024-09-11 - Transocean’s newest $232 million ultra-deepwater contract follows the company’s $123 million contract for six wells offshore India by Reliance Industries.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.