Colgate Energy management have noted the following three potential options for the company going forward, according to J.P. Morgan Securities Analysts Arun Jayaram: 1) remain private and continue paying dividends, 2) IPO, and 3) sale. (Source: Hart Energy/Shutterstock.com)

As bidding among some offset operators is ongoing for Delaware Basin producer Colgate Energy LLC, as per a Bloomberg report, what will a buyer gain?

Wells Fargo Securities LLC analyst Nitin Kumar and team took a look.

First, here are the offset operators: Adjacent on the north are Devon Energy Corp., Matador Resources Co. and Coterra Energy Inc.; south, Centennial Resource Development Inc., PDC Energy Inc., Diamondback Energy Inc. and Callon Petroleum Co.

(Kumar emphasized in his note, “We are not implying that these operators would consider acquiring or partnering with Colgate, but are simply identifying those publicly traded E&Ps with offsetting acreage that can help drive cost synergies in a potential deal.”)

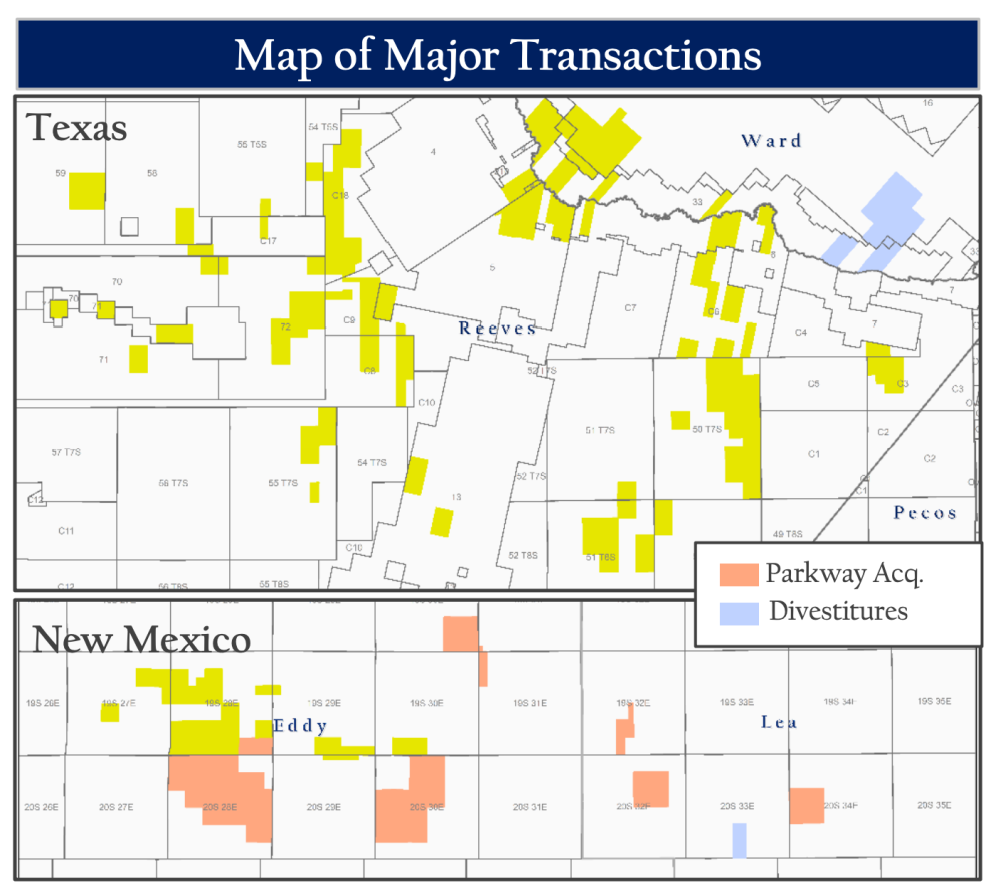

The leasehold: Roughly 101,000 net acres with about half in Eddy and Lea counties in New Mexico and half in Reeves and Ward counties, Texas.

Production: Roughly 60,000 boe/d.

Valuation: “We estimate an implied value of some $25,000 per undeveloped acre, which is above 2021 deal comps of some $11,000 per acre,” Kumar reported.

Colgate has five rigs drilling currently, as per a Feb. 14 report by J.P. Morgan Securities LLC analysts, led by Arun Jayaram.

Jayaram and the JPM team visited with Colgate in December, reporting that the E&P “had recently paid its second dividend of the year” with its free cash flow.

In addition to Endeavor Energy Resources LP, which focuses on the Midland Basin, Colgate is the other private Permian operator with higher quality acreage, “which is not the case for most smaller, sub-scale privates,” Jayaram added.

Well productivity: Kumar at Wells Fargo reported this morning that Colgate’s well productivity has been improving since 2018 based on six-month cumulative boe/foot.

“Northern wells had approximately 33% better well productivity than their southern counterparts last year, even though the acreage sits in what is typically called the ‘New Mexico Slope’ and is perceived to be less productive.”

In comparison with offset operators’ results, he added, “not only did the company have the highest productivity in 2021, its 12% year-over-year improvement was above that for peers.”

He concluded, “Based on $60 WTI and $3 Henry Hub, we estimate that the proved reserves are worth approximately $2.4 billion.”

Decision timeline: After the December visit with Colgate, JPM’s Jayaram reported, “Colgate management noted three potential options for the company going forward: 1) remain private and continue paying dividends, 2) IPO, and 3) sale.

“The company noted that remaining private limited the amount of capital available to do deals as the company keeps a close eye on leverage metrics. Management noted that the IPO route could be interesting if equity markets were supportive, but that it did not feel forced to pursue this option.

“Colgate also commented that following closing a number of deals that the business would be more mature by mid/late 2022, perhaps indicating a timeline on when it might consider transacting.”

Recommended Reading

HNR Increases Permian Efficiencies with Automation Rollout

2024-09-13 - Upon completion of a pilot test of the new application, the technology will be rolled out to the rest of HNR Acquisition Corp.’s field operators.

AI & Generative AI Now Standard in Oil & Gas Solutions

2024-07-25 - From predictive maintenance to production optimization, AI is ushering in a new era for oil and gas.

TGS Releases Illinois Basin Carbon Storage Assessment

2024-09-03 - TGS’ assessment is intended to help energy companies and environmental stakeholders make informed, data-driven decisions for carbon storage projects.

STRYDE Awarded Seismic Supply Contracts in Mexico

2024-09-03 - STRYDE was awarded two seismic node supply contracts in Mexico, the company’s first projects in the country.

PakEnergy Plows Ahead with New SCADA Solution

2024-09-17 - After acquiring Plow Technologies, home of the OnPing SCADA platform, PakEnergy looks to enhance its remote monitoring solutions.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.