The Halliburton fracturing crew working with Eclipse Resources broke a Halliburton record for the most stages completed in a month by a single crew in the U.S. northeastern region. (Source: Halliburton)

Finding the right recipe for a fracturing job is critical in shale plays. In the Utica Shale, Eclipse Resources is writing a whole new cookbook.

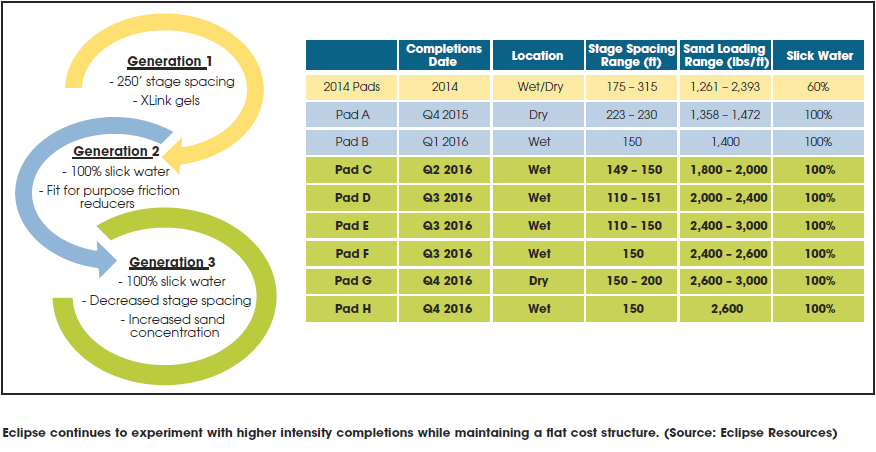

At a time when many companies are deferring well completions to a later date, Eclipse is so happy with its “Generation 3” completion design that it turned 11 gross wells to sales during third-quarter 2016 and, according to its third-quarter results, is “very encouraged with the initial results of the wells as compared to the company’s previous completion designs.”

Perhaps more telling is the fact that while completing wells for Eclipse, its Halliburton fracturing crew set a Halliburton record for the most stages completed in a month by a single crew in the northeastern region, then broke its own record the following month. Eclipse also helped the Halliburton crew set a record for the total amount of proppant pumped in a month by a single crew in the northeastern region. The crew pumped more than 82 million pounds of proppant in October 2016.

The reason for the feeding frenzy is the record-breaking Purple Hayes 1H well in Guernsey County, Ohio. The 5,640-m (18,500-ft) lateral is the longest ever drilled in the U.S., and the 124 fracture stages were completed at a rate of 5.3 stages per day. Dubbed the “Super-Lateral Program,” this type of drilling and completion design has become the standard for Eclipse in its Utica acreage.

Back to basics

Speaking at Hart Energy’s 2016 DUG East conference, Oleg Tolmachev, Eclipse’s senior vice president of drilling and completions, told the audience that the company took a systematic, process-driven approach to execute this well construction project. The process involved multiple well planning iterations and torque and drag modeling as well as a tight range of mud parameters, bit selection, cement design, wireline drag models, fracture design and drill-out methods.

“Super laterals allow us to dramatically lower F&D [finding and development] cost, which is crucial in today’s low commodity price environment,” he said. In an interview with E&P, Eclipse President and CEO Benjamin W. Hulburt went into more detail.

“Essentially you are spreading out the fixed-cost portion of the wells, which is the pad cost in the vertical portion of the well. You are spreading that out over a greater amount of productive lateral.”

The problem in the past, he said, was that the farther out the lateral is drilled, the less recovery per foot was achieved. “What we are trying to prove is that in this reservoir with our completion design we will not get significantly different recovery by going longer,” he said. “That’s what we feel pretty strongly we’ve proven, at least to ourselves.”

Indeed. As of Nov. 3, 2016, the Purple Hayes No. 1H well had produced a cumulative amount of 67.9 MMcm (2.4 Bcfe) during its 185 days of production while encountering much smaller pressure declines than expected. It’s expected to outperform Eclipse’s legacy “type well” reserve expectations by 28% to 50%.

Going after the DUCs

Like many companies, Eclipse has a portfolio of drilled but uncompleted (DUC) wells in its asset base. Unlike some companies, it drilled these wells with every intention of eventually completing them and bringing them onstream. In most cases, higher prices would be the lure to complete the DUCs. But Eclipse has other reasons as well.

“We are really glad we drilled them as DUCs,” Hulburt said. “If we had fracked them two years ago when we drilled them, we would not have used this new frack design.” The company completed 12 DUCs in third-quarter 2016 using its new Generation 3 completion design, he added, while staying within budget.

Lessons learned?

Eclipse has benefitted from the addition of some savvy Appalachian drillers from other companies. Hulburt said this type of experience certainly helps when drilling the vertical portion of these wells. “They know what zones tend to be a problem on the way down,” he said.

The completion design, on the other hand, can’t be compared to experience in, say, the Marcellus Shale. “I don’t know how transferrable that is,” he said. “But certainly having the regional service contracts and relationships helps a lot.”

Hulburt added that operators in other parts of the country are interested in learning more about this completion design. “We have gotten a lot of inbound calls,” he said. “It has definitely been a pretty fantastic project for us. We obviously don’t want to just tell all of our competitors how we did it, but we’ve definitely had calls from all over the country [from] different operators in different shales.”

Though Hulburt wasn’t aware of any other companies that are trying something similar, he said the trend overall is to go with longer laterals. It’s the other costs that have to be factored in.

“In the Permian your pad costs are probably $150,000,” he said. “Where we are, building a pad is $2 million, sometimes $3 million. At some point it’s probably easier and cheaper for operators in the Permian to just build another pad. You definitely add a level of risk going out this long.”

Having dry gas helps. Unlike other gassy plays like the Eagle Ford, where operators moved into the liquids portion of the play when natural gas prices tanked, dry gas is still the preferred target. “Even at $2.50 gas prices, the wells are still very economical if you are in the core area,” Hulburt said. “The dry gas portion is pretty much where all of the drilling rigs are in the Utica now.”

Overall, Hulburt is bullish on the industry going forward, enough so that the company has finished out its 2017 gas hedging program, which now covers about 80% of its expected production. “I think the fundamentals have been improving throughout the year,” he said. “We certainly are not out of the woods yet. But I think we definitely feel a lot better than we did six or eight months ago.”

[SIDEBAR]

Companies to form North American land pressure pumping company

Baker Hughes Inc., CSL Capital Management and West Street Energy Partners (WSEP), a fund managed by the Merchant Banking Division of Goldman Sachs, announced an agreement to create a pure-play North American land pressure pumping company, according to a Nov. 29, 2016, press release.

Under the terms of the agreement, Baker Hughes will contribute its North American land cementing and hydraulic fracturing businesses, which comprise assets in the U.S. and Canada. This includes personnel, expertise, technology and infrastructure. Upon closing, CSL Capital Management will contribute its Allied Energy Services platform, which provides hydraulic fracturing and cementing services on land in North America. Further, CSL Capital Management and WSEP will together contribute $325 million in cash to the new company, of which $175 million will be used to strengthen its balance sheet and position it for growth while the remaining $150 million will go to Baker Hughes. CSL Capital Management and WSEP together will own 53.3% of the new company, and Baker Hughes will retain a 46.7% ownership stake. The new company will operate under the BJ Services brand and will be headquartered in Tomball, Texas.

Warren Zemlak, current president and CEO of Allied Energy Services and former long-time senior executive with both Schlumberger and Sanjel, will serve as CEO of BJ Services. “The combined company will have 1.9 million hydraulic horsepower and more than 240 cementers, among other assets, and an owned-facility footprint throughout North America to serve our customers in all basins,” he said.

Recommended Reading

Colonial Shuts Pipeline Due to Potential Gasoline Leak

2025-01-14 - Colonial Pipeline, the largest refined products pipeline operator in the United States, said on Jan. 14 it was responding to a report of a potential gasoline leak in Paulding County, Georgia and that one of its mainlines was temporarily shut down.

Colonial’s Line 1 Gasoline Service Restored, Company Says

2025-01-20 - Colonial Pipeline Co. stopped flows on the gasoline transport line following reports of a leak in Georgia.

MPLX Acquires Remaining Interest in BANGL for $715MM

2025-02-28 - MPLX LP has agreed to acquire the remaining 55% interest in BANGL LLC for $715 million from WhiteWater and Diamondback.

Kinder Morgan Acquires Bakken NatGas G&P in $640MM Deal

2025-01-13 - The $640 million deal increases Kinder Morgan subsidiary Hiland Partners Holdings’ market access to North Dakota supply.

Tallgrass, Bridger Call Open Season on Pony Express

2025-02-14 - Tallgrass and Bridger’s Pony Express 30-day open season is for existing capacity on the line out of the Williston Basin.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.