(Source: Shutterstock.com)

[Editor's note: A version of this story appears in the November 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Like something from an ancient myth, the great steel forges of the Mediterranean have spun out hundreds of miles of pipeline to cross the Permian wilderness.

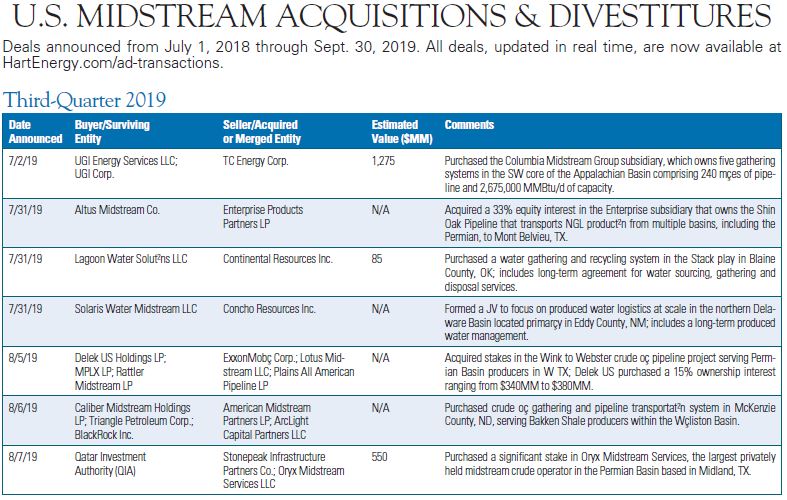

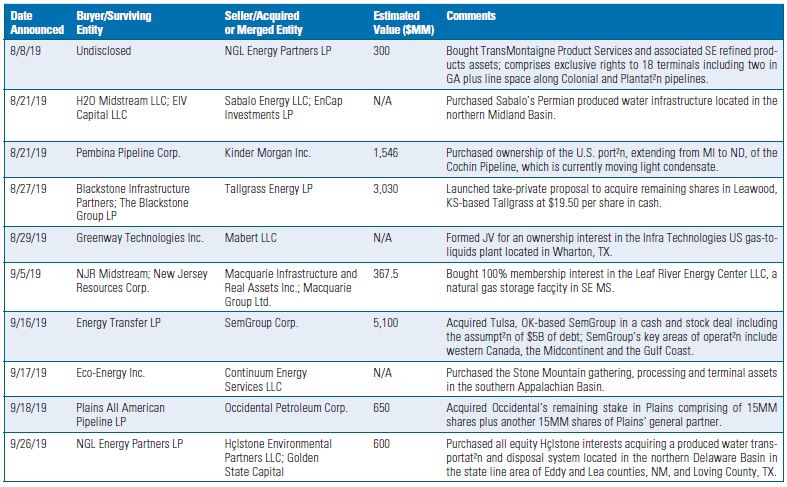

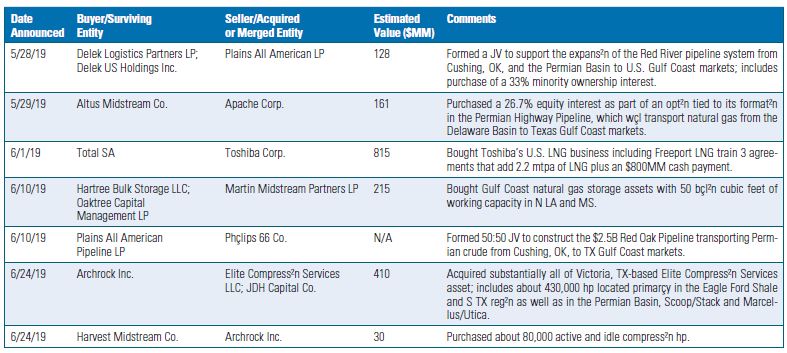

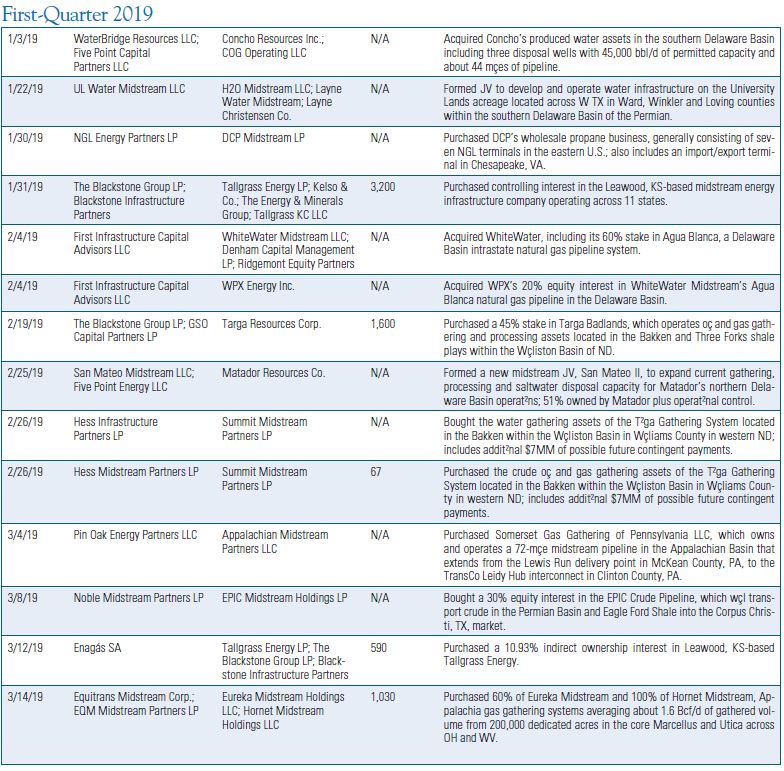

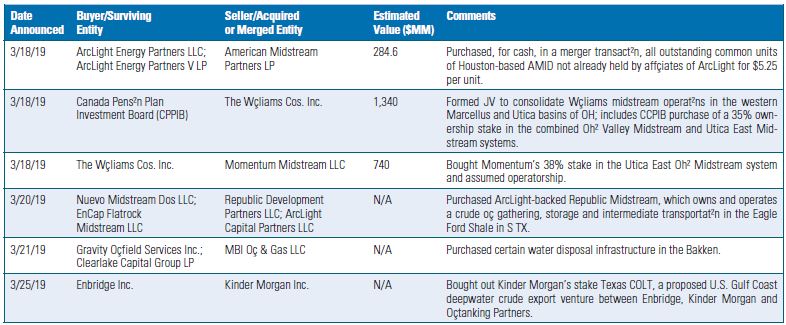

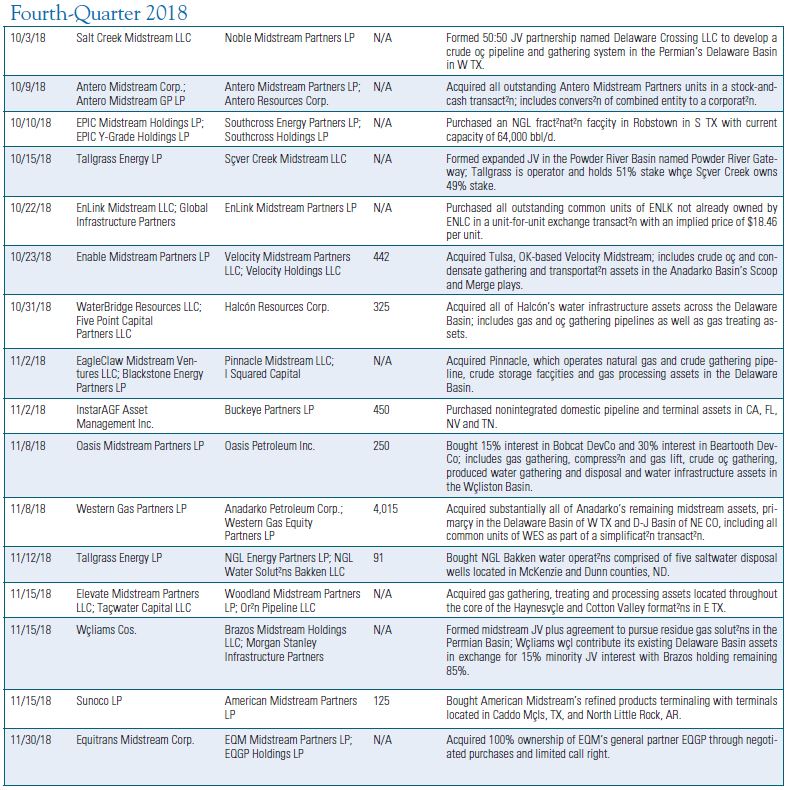

And the buildout has been expensive. Beginning in 2018, transactions for midstream infrastructure assets in the Permian and elsewhere in the U.S. exceeded $100 billion, particularly as companies looked to simplify corporate structures last year, according to PwC.

But the tumult in the oil and gas markets has dogged midstream companies, driving down their value through mid-2019 even while the sector’s EBITDA remained steady during the downturn and has grown significantly since, according to a July 30 report by Moody’s Investors Service.

Like their upstream customers, midstream companies have increasingly been denied the inexpensive capital from the market or lenders since the downturn.

“It’s been a pretty rough period,” said Frank Murphy, managing director and co-head of energy investment banking at Robert W. Baird & Co. “The most fundamental change that’s occurred is that the capital markets have largely been closed not only to upstream E&Ps but also to midstream companies.”

That’s opened the door for private-equity buyers, and they’ve been busy.

In May, IFM Global Infrastructure Fund made what Barclays called the “first meaningful corporate-level” offer to take Buckeye Partners LP private in a $6.5 billion deal.

The transaction has a $10.3 billion enterprise value. The Buckeye buyout followed ArcLight Energy Partners’ March announcement to take American Midstream Partners (now Third Coast Midstream) private for $300 million.

And in August, Blackstone Infrastructure Partners made a take-private offer to Tallgrass Energy LP at a nearly 36% premium to its stock price that valued the company at about $5.5 billion.

Public deals continue to emerge, but at a slower rate.

Energy Transfer LP said in September it would buy SemGroup Corp. in a unit and cash transaction worth about $5.1 billion.

Peter Bowden, global head of energy for Jefferies LLC, served as exclusive financial adviser to SemGroup and the sale of Pegasus Optimization Managers LLC, a high-horsepower compression platform backed by Apollo Global Management Inc., to a portfolio company of EQT Infrastructure.

As the midstream sector has fallen out of favor in the market, private-equity firms have stepped up with “the fire power to do important transactions,” Bowden said.

If market conditions persist, “you will see more and more of these take-private proposals. These are good businesses that generate real returns. If the public doesn’t want to own them, then private investors will,” he said.

The prominence of private-equity buyers has changed significantly since the roaring shale boom days before 2014, Murphy said.

Consider: In 2014 and 2015, about 85% of midstream transactions involved what Murphy calls strategic buyers—primarily public companies. Collectively, private-equity and infrastructure and sovereign wealth funds made up the remainder of buyers.

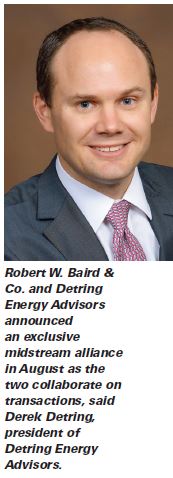

Business is still moving. In August, Baird and Detring Energy Advisors announced an exclusive alliance targeting midstream mergers, acquisitions and divestitures. Detring will provide expertise in technical underwriting and upstream forecasts, while Baird provides strategic advice and transaction services to midstream clients.

Murphy said that in 2014, before oil prices plummeted, midstream activity was concentrated in MLPs.

“Since then, the midstream public capital markets have been more or less shut,” he said.

The market’s indifference to midstream has caused public companies to shift their focus “from acquiring assets to managing and in some cases to divesting assets,” he said.

Today, private-equity-sponsored companies, infrastructure funds and pension and sovereign wealth funds represent nearly half of the market’s buyers, up from about 15% in 2014. “They just stepped in to be major buyers in the marketplace today,” he said. “In part because the strategic buyers have limited access to capital, and they’ve been told by investors to stop growing for growth’s sake instead manage their current portfolios to generate more economic returns.”

‘The Permian requirement’

One basin among all others has driven first upstream and now midstream sector M&A: the Permian.

Jefferies’ deals with private-equity acquisitions have focused squarely on “establishing a position or getting bigger” in the basin. As of Sept. 27, Permian rigs made up 58% of the most recent Baker Hughes rig count—up slightly from 56% a year ago.

“What has driven much of the midstream dealmaking is what I call the ‘Permian requirement,’” Bowden said. Because of the high levels of activity there, he said, “it is a nonoptional resource, in our view.”

Still, many of Jefferies’ transactions have involved smaller businesses backed by “boutique private-equity firms” selling to larger, generalist private-equity and infrastructure firms, Bowden said.

“The buyers in those large transactions were predominantly focused on establishing a position or getting bigger in the Permian Basin.”

In the past 12 months, at least 35 Permian midstream deals have been publicly announced, with about half of those deals disclosing deal values of $18 billion.

Despite the market’s negative reaction to public midstream transactions, “that doesn’t mean that [public] buyers aren’t making good deals,” he said. “These are good businesses. Under these market conditions, CEOs need to manage their businesses in a manner that meets their strategic priorities rather than catering to market sentiment, which is unlikely to improve in the near term.”

A larger movement in the midstream sector may be afoot, underscored by pipeline capacity that now roughly matches the Permian, said Patrick Knapp, an attorney with McGuireWoods’ mergers and acquisitions practice. New pipelines projects that have been in the works for years are coming online, and a huge increase in basin takeaway capacity has reached a level “unlike anything we’ve ever seen before.”

“There’s been a change in growth patterns that has been driven largely by strategically focused E&P growth centered around free cash flow rather than pure production numbers,” he said. “It’s not so much about producing as many barrels as I can produce anymore from an E&P’s perspective. It’s about maximizing your free cash flow and producing the right amount of barrels.”

The industry is now evolving its preferences for infrastructure. As drilling programs have expanded, the need for other infrastructure has accelerated.

“We’ve seen traditional oilfield service businesses such as water disposal evolve in the past few years to become more midstream-centric businesses,” Knapp said, “where you’re seeing pipeline buildout and large contract commitments and large capital programs built around these water disposal companies.”

In the past year, at least nine deals have focused on water infrastructure, including produced water management.

Derek Detring, president of Detring Energy Advisors, said that several operators own legacy water infrastructure, especially in the Permian Basin.

“They have been putting contracts in-place providing separate entities to charge themselves certain fees per barrel of water,” he said, “where they can potentially combine with offset operators’ water systems before they sell … or potentially take that vehicle public.”

The epic momentum of building and buying seems to be changing, Knapp said.

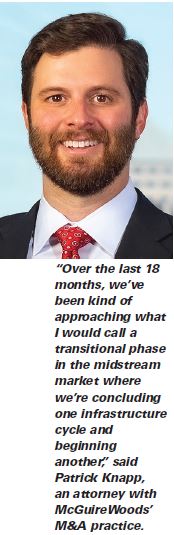

“Over the last 18 months, we’ve been kind of approaching what I would call a transitional phase in the midstream market where we’re concluding one infrastructure cycle and beginning another,” Knapp told Investor.

“What we’ve seen in the midstream over the past five to 10 years is an extraordinary buildout in takeaway capacity and particularly pipeline infrastructure,” he said.

With E&Ps reducing capex and large-scale drilling programs at an advantage, “at the end of the day, I think that is probably pointing to more consolidation in all of the upstream, midstream and oilfield service sectors in the Permian,” Knapp said.

Disconnect

Is the M&A market just misunderstood?

In the past six years, U.S. midstream companies have struggled to return to pre-downturn valuations and deliver value to shareholders above the cost of capital, despite consistent production volume growth and margin recovery, according to PwC’s second-quarter oil and gas deals report.

And M&A has been frowned upon by investors.

Barclays said Sept. 9 that the appetite for large-scale deals among public companies seems “fairly muted” because of a focus by midstream companies on deleveraging and weak public valuations of assets. In echoes of the upstream market, midstream investors are also expressing a preference for balance sheet strength.

“M&A talk wanes but doesn’t disappear,” Barclays said a report.

Under normal market conditions, the transactions Bowden has seen would have been made by investment-grade pipeline companies.

“Because the public markets are in such bad shape, public companies that have growth initiatives need to generate proceeds from something and selling minority interests in assets, joint ventures and divesting noncore assets all offer a path to funding their growth initiatives,” Bowden said. “Without those types of transactions, some companies are simply going to have to eliminate a portion of their forward growth projects.”

However, capital appears too expensive for some public midstream companies.

In September, The Williams Cos. Inc. management was asked about its reported consideration of a bid, with Global Infrastructure Partners, for Noble Energy Inc.’s midstream business, Noble Midstream Partners LP, according to Barclays.

Without commenting on the report, Williams said that it “viewed its cost of capital as too high to use its own capital as a source of funds” but wouldn’t preclude it from partnering with a private-equity fund, Barclays said.

The PwC noted that midstream, as a whole, has struggled to generate returns above the cost of capital—posting roughly 1% negative annual returns compared to capital costs from 2015 through 2018.

“Continued PE interest in midstream during prolonged challenged times has driven investors to rethink their approach to asset commercial diligence,” said Bassem Salama, director of energy strategy at PwC.

Investors are also concerned with increased contract risks due to potential E&P bankruptcies, the increased time and complexity required for regulatory approvals and new short-to-medium term contract arrangements, PwC said.

The overall market has been shaped by the upheaval of the past five years, as upstream and midstream markets moved from the roaring shale boom with high oil and gas prices to a lower commodity price environment and a need to focus activity on areas with the highest economic returns, Murphy said.

“The midstream market’s gone through this evolution,” he said. “It … parallels what’s going on in the upstream market where the strategic [buyers] are taking a much more disciplined approach, de-emphasizing acquisitions and managing their portfolios to generate free cash flow and keep leverage at lower levels.”

Bowden said the market tends to penalize public companies and particularly buyers during a downcycle. But public-equity firms have recognized the value in those companies, even as they’ve fallen out of favor with investors.

“Private investors don’t care about the ticker symbol,” he said, adding, “These are good businesses that generate real returns.

“If the public doesn’t want to own them, then private investors will.”

Recommended Reading

E&P Highlights: Aug. 26, 2024

2024-08-26 - Here’s a roundup of the latest E&P headlines, with Ovintiv considering selling its Uinta assets and drilling operations beginning at the Anchois project offshore Morocco.

OMV Makes Gas Discovery in Norwegian Sea

2024-08-26 - OMV and partners Vår Energi and INPEX Idemitsu discovered gas located around 65 km southwest of the Aasta Hansteen field and 310 km off the Norwegian coast.

E&P Highlights: Sep. 2, 2024

2024-09-03 - Here's a roundup of the latest E&P headlines, with Valeura increasing production at their Nong Yao C development and Oceaneering securing several contracts in the U.K. North Sea.

Breakthroughs in the Energy Industry’s Contact Sport, Geophysics

2024-09-05 - At the 2024 IMAGE Conference, Shell’s Bill Langin showcased how industry advances in seismic technology has unlocked key areas in the Gulf of Mexico.

Devon Energy Expands Williston Footprint With $5B Grayson Mill Deal

2024-07-08 - Oklahoma City-based Devon Energy is growing its Williston Basin footprint with a $5 billion cash-and-stock acquisition from Grayson Mill Energy, an EnCap portfolio company.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.