U.S. production growth could either overwhelm demand as in previous cycles, or it could simply fill the gaps in global crude supply. Which will it be? (Source: Lowell Georgia)

A version of this story appears in the April 2018 edition of Oil and Gas Investor. Subscribe to the magazine here.

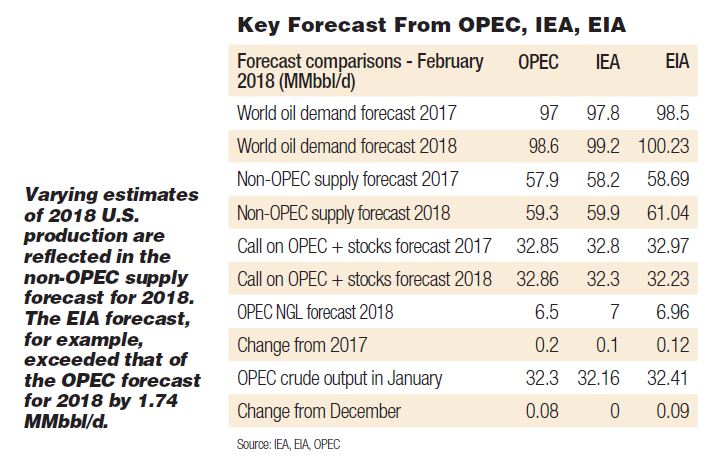

If ever there were a case for multiple scenario analysis, the past few months in energy markets would likely qualify. On “base case” analysis alone, domestic and international energy agencies vary considerably in their forecasts of demand and, especially, supply, as do major research houses. Add in the thorny issue of OPEC policy, and the range of outcomes expands even more.

A number of issues are in the mix. U.S. storage in Cushing, Okla., widely recognized as holding the last inventories to be drawn down, were in mid-February at levels last seen in December 2014. But production of U.S. crude is on a tear, having already topped the historic 10 million barrels per day (MMbbl/d) late last year. Projections for U.S. growth this year differ, but in some cases will reach 2 million barrels of oil equivalent per day (MMboe/d).

For those holding a bearish 12- to 18-month view, the risk is seen as a repeat of 2014 to 2015, when non-OPEC supply, led by the U.S., flooded the market. Meanwhile, more bullish observers point to the trend of further declines in inventory levels, recent robust demand growth throughout much of the world and wild card events that could disrupt the normal flow of crude oil.

With inventories at historic low levels, the risk of geopolitical-related dislocations of supply rises. Where are such risks? Foremost, the economic collapse of Venezuela; the enmity between long-time rivals Saudi Arabia and Iran, playing out in their proxy wars in Yemen and Syria; and supply disruptions by armed factions in Libya and the Delta Avengers in Nigeria.

Of course, it is easier to model and assign a probability factor to the rising tide of U.S. supply than it is to an essentially unpredictable wild-card event. Yet, assuming OPEC remains committed to its policy of production restraint through year-end, the actions of the U.S. and Venezuela could end up as counter-weights in their influence on the relative tightness or looseness in global supply, said one observer.

Venezuela declines

“When we think about the twin stories in the oil market this year, we have on the one hand surging U.S. shale production and [on the other] the potential offset in Venezuela,” said Helima Croft, global head of commodity strategy with RBC Capital Markets LLC, in a mid-February CNBC interview. “The real question is: How fast does Venezuela fail? There is no indication that Venezuela is going to get its act together in the near term.”

What’s not in doubt is the elasticity of U.S. supply, which has allowed U.S. unconventional producers to respond rapidly to oil price signals. Following an $8- to $9-per-barrel rise in oil prices during the last couple of months of 2017 and through January 2018, the U.S. rig count added more than 40 oil rigs, mainly in the Permian Basin. If this continues, the “outcome will likely end in tears,” warned one research house.

That said, OPEC, with Saudi Arabia as its de factor leader, appears to be prioritizing support for crude prices, even if it comes at the cost of market share losses to North American producers.

“If we err on overbalancing the market a little bit, so be it,” said Saudi Energy Minister Khalid al-Falih in Riyadh, after meeting with his Russian counterpart, Alexander Novak, to discuss, among other issues, global crude and product inventory levels. “Rather than quitting too early and finding out we were dealing with less reliable information. … [We’ll] stay the course and make sure that inventories are where the industry needs them.”

Like other commodity specialists, the team at Citi moved up its price forecasts for the first quarter of this year. But for the balance of 2018 and into 2019, Citi’s oil price projections are all downhill from its first-quarter call of $65/bbl for Brent and $61/bbl for West Texas Intermediate (WTI). For full-year 2018, Citi is calling for Brent and WTI to average $57 and $54, respectively, and then drop to just $49 and $43 in 2019.

In essence, Citi sees global oil demand growing rapidly but the supply side growing still faster.

“A repeat of 2014”

“We continue to believe that OPEC and, to a lesser extent, the International Energy Agency (IEA) are vastly underestimating the magnitude and sustainability of non-OPEC oil supply growth,” observed Ed Morse, global head of commodity research at Citi. “And, in many respects, 2018 is looking like a repeat of 2014.”

The lesson learned from 2014 lies in the similar setup: Combining production increases from the U.S., Canada and Brazil, “there was enormous growth of over 2 million barrels per day,” said Morse.

The high growth in 2014 resulted in the Atlantic Basin becoming a “surplus basin” for the first time in multiple decades, he recalled, and producers turned to the Pacific Basin for growth markets, resulting in markedly sharper competition with Russia, Saudi Arabia and other Middle East exporters. In turn, Saudi Arabia sought to recapture lost market share, resulting in “very big inventory builds.”

As of mid-February, Citi’s forecast of U.S. liquids production growth in 2018 came to 2.05 MMbbl/d, comprising 1.4 MMbbl/d day of crude and 650,00 bbl/d of NGL. (This is revised up from an earlier 1.6 MMbbl/d forecast, including NGL, to reflect in part additional producer hedging.) Canada and Brazil are projected to add 300,000 bbl/d and 200,000 bbl/d, respectively, bringing the three countries’ combined growth to 2.55 MMbbl/d—well above the 2-plus MMbbl/d of production growth in 2014.

Morse attributed the early 2018 strength in crude prices to simultaneous growth in both emerging and advanced economies in the fourth quarter of last year, with “sluggish” economic growth seen only in various petro-states. Higher trade activity boosted demand for diesel and marine fuel, with consumption of distillate on the rise for “the first time in half a decade.” Meanwhile, jet fuel demand was “booming,” and growth in petchem demand—accounting for about 35% of total demand—was “healthy.”

Notably, a swing “from tightness to glut” is forecast in spite of projections that U.S. and Asian demand are “way up,” and physical tightness in markets may continue through the summer. In addition, with less use of “high-frequency data,” such as satellite tracking of storage and oil flows, OPEC is viewed as likely “overtightening” oil markets, such that rebuilding of global inventories is pushed out to the latter part of this year, according to Citi.

Nonetheless, crude markets are expected to soften toward year-end as U.S. production marches higher and seasonal factors affect the call on U.S. production, according to Morse. “As we go into the winter, the call on U.S. shale is higher than U.S. shale production, but by the end of the year, the call on U.S. shale will be lower than U.S. shale production.”

Growth in U.S. production, combined with other non-OPEC crude production, soon starts to offset the projected growth in global demand. Citi estimates increased demand of 1.65 MMbbl/d in 2018 and 1.6 MMbbl/d in 2019, taking global demand up to 99 MMbbl/d this year and 100.6 MMbbl/d in 2019.

For the U.S. alone, crude production is estimated to rise 1.4 MMbbl/d to 10.8 MMbbl/d in 2018, followed by an increase of just under 1 MMbbl/d to roughly 11.7 MMbbl/d in 2019. While the U.S. makes up the lion’s share of the growth, other non-OPEC producers are additive, taking total non-OPEC crude production up by 1.8 MMbbl/d and 1.3 MMbbl/d in 2018 and 2019, respectively.

With NGL also added in, total non-OPEC supply (non-OPEC crude plus NGL) rises to slightly under 2.2 MMbbl/d in 2018 and 1.6 MMbbl/d in 2019, offsetting the increases in global demand.

Responding to price

“One thing is becoming clear: The oil market is as fluid and dynamic as it has ever been, with short-cycle U.S., OPEC and non-OPEC producers increasingly responsive to oil prices,” observed Morse.

While modeling points to lower crude prices, Morse’s take on geopolitical factors is that “the risks are for a higher price from just a supply disruption vantage point.” Supply disruptions, at about 1.5 MMbbl/d recently, are the lowest in seven years and compare with a peak level of 4 MMbbl/d, he noted.

Changes in Barclays’ commodity price deck have also reflected short-term price strength followed by a move lower during the balance of the year. After a projected $10 jump in Brent to $66/bbl for the first quarter, Barclays forecasts average 2018 prices of $60 for Brent and $55 for WTI, reflecting a sharp rise in U.S. volumes that will tend to pressure prices during the year.

Among the key underlying assumptions are that U.S. liquids supply will rise by 1.4 MMbbl/d in 2018, comprised of 1.1 MMbbl/d of crude production, primarily from the Permian, and 300,000 bbl/d of NGL. For 2019, Barclays projects a further rise in liquids of about 1 MMbbl/d, comprised primarily of crude, which is forecast to grow by 800,000 to 900,000 bbl/d.

A “lot of moving parts”

“When we construct our bottom-up balance, we estimate the global supply/demand balance will flip back into surplus by the second quarter, and that the global surplus will continue into the fourth quarter and basically throughout 2019,” said Michael Cohen, Barclays’ head of energy markets research. But there are a “lot of moving parts,” and the 2018 surplus is only 200,000 to 300,000 bbl/d, he noted.

“When we’re talking about a difference between supply deficit and supply surplus of 200,000 to 300,000 bbl/d, we’re on a fine knife’s edge,” he added. “The reality is that we’re in a 95- to 100-MMbbl/d market, depending on which products you’re including, and at the end of the day, half a million barrels per day of production here and there can be rounding error.”

Among the various moving parts, geopolitical risk—especially relating to Venezuela—stands out at a time of diminished global inventories, according to Cohen. “The geopolitical risk premium tends to be larger when inventories are drawing and the market sees they’re drawing,” he observed. “And recent prices are not adequately covering the whole scope of security-of-supply concerns.”

A late-January Barclays report forecast production in Venezuela would average 1.43 MMbbl/d in 2018, a decline of nearly 700,000 bbl/d from data reported directly to OPEC for 2017. But there is a void of good data on what’s happening on the ground in Venezuela, according to Cohen.

“We expect the collapse in production will continue,” he said. “We estimate production was around 1.5 to 1.6 MMbbl/d in February, and that with a bigger risk of production decline in the first half of this year, output reaches a low of 1.35 MMbbl/d in the second half of 2018. In our balances, we then expect that, on a risked basis, it will stay in the 1.4- to 1.5-MMbbl/d range.”

In terms of many E&Ps’ resolve to adhere to capital discipline, Cohen observed that “capital discipline doesn’t equal austerity. It doesn’t mean producers are not going to follow through on expectations for spending and guidance for production. Essentially, they can have their cake and eat it, too. As long as WTI prices stay above their breakeven or the economic level for their wellhead supply, they’ll be able to do both: make returns to shareholders and meet their production obligations.”

And with the U.S. unconventional sector gaining market share at OPEC’s expense for now, said Cohen, “OPEC is essentially caught between a rock and a hard place, because in order to maximize short-term revenue, they’re sacrificing long-term revenues. They have to thread the needle every month that goes by, depending on what information they gain about how shale responds to different price levels.”

Jason Gammel, integrated oil analyst in London for Jefferies LLC, was early to raise his 2018 forecast for Brent, taking it up $6 to $63/bbl in December of last year. He has held the forecast unchanged through press time in March. His 2019 forecast has Brent easing back to $60.

Gammel is quick to turn to the demand side of the equation in support of his 2018 crude oil forecast. “The very strong demand outlook, combined with the normalization of inventories, were the two main factors that led us to make the change in our price deck,” he said.

China demand

Not only were trailing global demand indicators coming in strong at the time of his forecast, but PMI (purchasing manager index) data were also signaling synchronized global GDP growth ahead, he noted. In China, a key growth area for energy, the numbers were “incredibly strong,” he added, reflecting both robust industrial activity as well as an inflection in vehicle sales that augured well for both auto and gasoline sales.

In addition, the late-2017 hurricane that hit the Gulf Coast provoked a rapid drawdown in inventories held in OECD countries and has “significantly alleviated” the overhang that was keeping a lid on crude prices, according to Gammel. Of particular note was the IEA’s estimate that OECD commercial stocks fell by 55.6 MMbbl in December, which was “the biggest draw we’ve seen since 2011,” he said.

Jefferies forecasts 2018 global demand growth at 1.7 MMbbl/d, of which 1.2 MMbbl/d is projected to come from China, India and Southeast Asia (Indonesia, Thailand, Malaysia, etc.). China is the biggest driver, of course, with India and Southeast Asia each contributing an estimated 300,000 bbl/d of incremental demand. January recorded Chinese imports at 9.6 MMbbl/d, while partially offsetting low levels imported in December, corroborating “the overall trend we’ve been observing,” said Gammel.

More moderate pace of growth

In terms of U.S. production in 2018, Jefferies’ forecast calls for growth of just under 1.4 MMbbl/d, comprised of roughly 1.0 MMbbl/d of crude and 375,000 bbl/d of NGL. To the extent this represents a more moderate pace of growth than projected by some of its peers, Gammel attributed the variance chiefly to the firm’s reading of the impact of decline curves.

“When you begin a period of higher activity, after a period of low activity, you have a relatively small number of wells that are on first-year declines of 65% to 70%,” he noted. “But as you add more and more of those wells into the base production—and the decline rates from the very recent activity become a larger part of production—it gets harder to offset the declines. We think activity levels will continue to increase from here, but the more years you’re into increased activity, the more difficult it is to grow.”

As the U.S. moves more into “manufacturing” mode, the industry is likely to face longer cycle times with production tending to be pushed a little further out into the future, observed Gammel.

“As we move into pad drilling and batch completions, what was a three-month cycle likely changes to a six- to nine-month cycle. Even if activity picks up to a pace beyond what we expected, the impact on 2018 production would be fairly minimal, although it would have an effect on 2019. Looking at 2018 in isolation, there isn’t much the industry can do to alter our outlook materially.”

Continuing draws

For 2018, the math at Jefferies points to inventories continuing to draw during the course of the year. This assumes OPEC compliance remains stable through year-end and that non-U.S., non-OPEC production in aggregate nets out at zero. In turn, this would leave global demand growth running at 1.7 MMbbl/d and exceeding U.S. supply growth of 1.4 MMbbl/d, including NGL.

Where could wild card events change the balance one way or the other?

Obviously, Venezuela, where the “economic situation is clearly providing a more bullish backdrop for oil prices,” said Gammel. “The outlook for Venezuela itself could be pretty bleak—and that’s without the risk of civil unrest. It doesn’t seem that it’s going to be resolved positively in the near term.”

Marshall Adkins, director of energy research at Raymond James & Associates, is among those with a more bullish outlook on energy. When many observers questioned whether WTI would move meaningfully above $50 last year, Raymond James held to a $60 year-end 2017 target. For 2018, his WTI target is straightforward: an average of $65/bbl, as $60 goes to $70 by year-end.

In essence, Marshall foresees a drawdown in global inventories continuing throughout 2018 and accelerating, on a seasonal basis, in the latter part of the year. He predicts the process of rebuilding inventories will commence in 2019 but will not be complete until late 2020. Underlying assumptions include a 1.7 MMbbl/d increase in U.S. production, including NGL, in 2018.

“Our model for the past 1.5 to two years has projected we’re going to draw inventories big time in 2017 and that we’ll continue to draw in 2018, depending on how the market reacts to a surge in oil prices in 2018,” said Adkins. “This should get us back to where we’re not drawing inventories sometime in 2019, but I don’t see the inventory situation getting fixed—assuming $65/bbl WTI—until the end of 2020.”

The Raymond James global supply/demand model has U.S. production rising 1.7 MMbbl/d in 2018, with crude comprising 1.2 to 1.3 MMbbl/d and NGL at 400,000 500,000 bbl/d. For next year, it projects a further increase of 1.4 MMbbl/d. On the other side of the ledger, global demand is projected to grow 1.5 MMbbl/d this year, slowing somewhat to 1.2 MMbbl/d in 2019.

Adkins points to U.S. inventories as a telltale sign of a tightening crude market. Offering the best real-time data, the U.S. inventories “have been collapsing since March of 2017,” he noted. “And since we’re usually the cheapest in the world—and so the first to build and the last to draw—if the U.S. inventory is collapsing, most everyone else’s must have already played out.”

Raymond James’ more optimistic global supply/demand outlook reflects in part its practice of revising upward the IEA data on oil demand, which initially tends to be understated and fails to match up with corresponding inventory levels pending revisions that are sometimes made years later, according to Adkins.

Oil demand “screaming higher”

“The global economic recovery has been more than offsetting the impact of higher oil prices, and oil demand is screaming higher,” he said. “That’s why everyone is missing the inventory numbers.”

Adkins deems metrics on five-year average storage levels of little use for forecasting, given the extent to which both demand and production have expanded during the last five years.

“You have to look at days of consumption or, in the U.S., days of production,” he advised. “That’s really important, because we use storage to facilitate consumption around the world and, in the U.S., to facilitate the movement of production.” Adding storage may be necessary, for example, to operate new capacity and avoid “problems where tank levels aren’t high enough to allow the system to work.”

In looking at industry activity levels, Adkins noted that good growth numbers are easier to attain early in the upcycle. “The average decline rate increases as you complete more and more wells, and the treadmill runs faster,” he said. “Even if you assume the rig count averages 1,100 this year and 1,200 next year and 1,250 thereafter, the peak growth year is still going to be in 2018.”

Adkins estimated the average decline rate of the unconventional sector at 40%, given its anticipated activity level, up from about 25% in 2016, when industry activity bottomed.

As for greater capital discipline, Adkins observed that even if larger publicly traded E&Ps adhere to being more fiscally responsible, they account for a little under half of active rigs. The other part is comprised of the majors and private E&Ps, who “are not answering to those same Wall Street investors. And there are also private-equity-backed players that have a ton of money and are tasked with growing,” he added.

“As an industry, I think they’ll outspend by probably 20%, but that’s only half the outspend of last year.”

Returning to the question of Venezuela, Adkins said the Raymond James model had yet to fully factor in the country’s “slowly unfolding disaster. If you take Venezuela totally offline, which has happened before, then oil goes haywire, nobody can make up for that, and oil prices spike for a while. The question will be: ‘How long will regime change take?’ And that’s impossible to answer right now.”

Recommended Reading

Not Sweating DeepSeek: Exxon, Chevron Plow Ahead on Data Center Power

2025-02-02 - The launch of the energy-efficient DeepSeek chatbot roiled tech and power markets in late January. But supermajors Exxon Mobil and Chevron continue to field intense demand for data-center power supply, driven by AI technology customers.

BlackRock CEO: US Headed for More Inflation in Short Term

2025-03-11 - AI is likely to cause a period of deflation, Larry Fink, founder and CEO of the investment giant BlackRock, said at CERAWeek.

Transocean President, COO to Assume CEO Position in 2Q25

2025-02-19 - Transocean Ltd. announced a CEO succession plan on Feb. 18 in which President and COO Keelan Adamson will take the reins of the company as its chief executive in the second quarter of 2025.

Ovintiv Names Terri King as Independent Board Member

2025-01-28 - Ovintiv Inc. has named former ConocoPhillips Chief Commercial Officer Terri King as a new independent member of its board of directors effective Jan. 31.

Independence Contract Drilling Emerges from Chapter 11 Bankruptcy

2025-01-21 - Independence Contract Drilling eliminated more than $197 million of convertible debt in the restructuring process.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.