Many believe American shale is in decline. In January, Pioneer Natural Resources CEO Scott Sheffield told a British newspaper, “The aggressive growth era of U.S. shale is over.” But Vikas Dwivedi said shale has a lot of mileage left in it. The global energy strategist at the Australian global financial services group Macquarie recently produced a paper for his clients arguing that shale has bountiful years ahead. In a conversation with Hart Energy, Dwivedi detailed the encouraging signs he sees, including the advent of supermajor brainpower, big data, AI, deeper drilling and continued innovation. (Source: Shutterstock.com)

Many believe American shale is in decline. In January, Pioneer Natural Resources CEO Scott Sheffield told a British newspaper, “The aggressive growth era of U.S. shale is over.” But Vikas Dwivedi and the Energy Strategy team at global financial services group Macquarie believe shale remains responsive and resilient. The global energy strategist and his team recently produced a paper for their clients in which they maintain a more optimistic outlook on US shale production through the current industry cycle. In a conversation with Hart Energy, Dwivedi detailed the encouraging signs he sees, including the advent of supermajor brainpower, big data, AI, deeper drilling and continued innovation.

Patrick McGee: What makes you believe E&P companies can continue pumping from shale for a long time to come?

Vikas Dwivedi: E&P companies are really good at it. They know how to take the risk. They’re willing to take technical risk, economic risk and the geology is stellar. We are in year 13 of shale. We’ve come a long way, and I think there’s still a long way to go in terms of how much it can produce. This is going against the grain of a lot of the narratives out there which say, “We’re running out of good acreage, we’re running out of the most productive wells. We’ve already drilled everything that is good. You only have a few years left.” Or, it’s capital discipline. Companies have been told by their investors, “Don’t drill. Don’t go crazy doing massive growth like you’ve done in the past.” And that will also slow down what can happen in shale.

We just disagree with all of that. Despite some of the more public comments from executives, you can see the capital rotating into shale, whether it’s Chevron, Exxon Mobil, BP. It’s very shale oriented. There’s a reason for that, and they’re not going to shrink their production. They’re definitely focused on renewables, but they also have to run their traditional business which make a lot of money.

If you go through the evolution of shale, it started off very clumsy—like all new things. A lot of it was done with muscle. If you were normally going to drill a horizontal well, like 4,000 feet, somebody said, “Why don’t we drill it 5,000 feet? Why don’t we drill it 8,000 feet? You know what, why stop there, go to 10,000.” And somebody else says, “Well, if 2,000 pounds of sand per foot is doing a lot more, what about 5,000 pounds of sand?”

There wasn’t any grand AI or super analytical framework. It was like, “Hey, take what’s working and do more of it.” Now you’re drilling further and faster. There’s some reason to believe that the pure muscle-based route of just doing everything bigger has kind of run its course, but I don’t think it has.

We’re moving into an area where you can use big data. The brainiac stuff is coming. There was a lot of science, but the really sophisticated stuff is still to come, like how do you extrapolate or interpolate from two areas that are good producers across a vast region of thousands and thousands of acres. The question is, “How do I use data to identify other areas that could be really good?” A lot of that is still to come. There’s a lot more running room in shale.

PM: OK. There might be more innovation to come, but people who disagree with you say there is less and less in the ground to extract.

VD: Yes. The doubters are looking at what they think is left in the ground, and they think there’s acreage exhaustion. And just by the virtue of economics, you’re always going to drill the best stuff first. That’s what I think are the fundamental underpinnings of these conclusions that maybe we’re slowly running out. But we’re not giving enough credit to productivity gains and engineering gains that will make some of the second-tier wells perform like first-tier wells.

One thing to note is we have a lot of different layers. Shale is a layer cake, and we haven’t drilled nearly all the layers—so many different layers and so many different pay zones that will produce hydrocarbon for a long time. The question is will they invest enough to learn these new layers. Every time you go to a new layer, there’s a learning curve. There’s a lot of capital that you have to spend. I think the heavy duty science is still coming. With all due respect to the independent companies who’ve done amazing work—and Schlumberger [SLB] has done amazing work—now you have the majors. I think Exxon has 2,000 Ph.Ds. They’re not all working on shale, but that’s a different level of science being brought to the table than some private equity-backed portfolio company. The other piece of it is the real brainiac stuff, like AI and big data.

PM: But is there real evidence that there’s a lot left in the ground?

VD: With all the science, geologists and engineers we have, what percentage of the oil that’s in the ground is actually extracted? Not nearly as much as you would think. Companies take samples of the rock to a lab. They extract it and then they effectively blow it up, and you can see how much oil was in it. This lab work shows that only about 10% of the oil was removed from the rock.

PM: OK. Is that remaining amount accessible?

It’s another bet on technology. Maybe there’s going to be even more interesting ways to get it. The fundamental challenge is exposing as much surface area as you can expose without blowing up the actual channels that the oil can travel on. If I obliterate it completely, there’s no path to go back up into the well. You need to find ways to improve the geometry of the angles of attack. That’s the challenge.

The private companies have historically had less productivity per well. It’s often they don’t have the best acreage, but they also typically don’t have the best geology or engineering because they’re smaller. Now, you have big oil field service companies that also are there, and they have that universal expertise because they work with everybody. Even though some companies will always be leaders, the rest of the pack isn’t just left in the dust. The leading edge goes up by 20% and then a year later the followers go up by 15%, and then they do it again. If you underestimate the mathematics of that process, you’ll underestimate what the growth could be as well.

PM: How many years or decades do you think shale will last?

VD: A lot of my peers think we’re going to peak in five to 10 years. I think that’s way too soon, and we can show 10 different reasons why. Absolutely, it can last. It’ll be able to grow through the peaking of oil demand. It could be a meaningful resource for 10 or 15 years, even if it peaks in a few years.

PM: Where in the industry are your fellow optimists, and where are those who see shale nearing the end of its life?

VD: There’s a lot of supercycle proponents that say, “We’ve underinvested in upstream oil for too long, and now we are in trouble; shale can’t grow to make up for the lack of investment in offshore and other big projects.” There’s some banks that are behind the supercycle thesis. But a lot of institutional clients like hedge funds and mutual fund portfolio managers and their analysts have the view that you’re going to run out of production growth fairly soon.

PM: Your research has a sharp focus on rig counts. Why is that important? You mentioned that innovations have crews circling back to second tier rigs and getting more out of them than the first time around. Is that right?

VD: That’s right. The rig count is important because, besides actually identifying the geology where there is oil and gas, the rig is the first real physical manifestation of that whole effort to turn it into oil production. You can do metrics on rigs. By the end of the year, you used to be at 2,000 to 3,000 barrels a day for the wells that that rig made. Now it’s like 10,000, 12,000, 14,000 depending on what part of the country you’re in. And that's just over 10 years. In some places we’ve quadrupled and quintupled in 10 years.

PM: Can you name some of the innovations that are extending the rigs’ life and efficiency?

VD: The first is speed. It’s an innovation from the engineering and process side, meaning the rig has more horsepower and has a lot more tools. Instead of doing 10 wells a year, it can do 20 wells. The other innovations are more advanced geometry. What if I drill down and then more at an angle, and I do it again from another angle? Think about the resource as a cube; I’m draining more of the cube. I’m hitting it from a lot of angles, and I’m creating a lot more surface area. Another innovation is pad drilling. That sounds so obvious after you do it, but instead of a rig drilling a well, one may go down one way and the other goes down in a different direction. It’s multiple wells going when they get to their depth. That’s another way to rapidly increase the productivity.

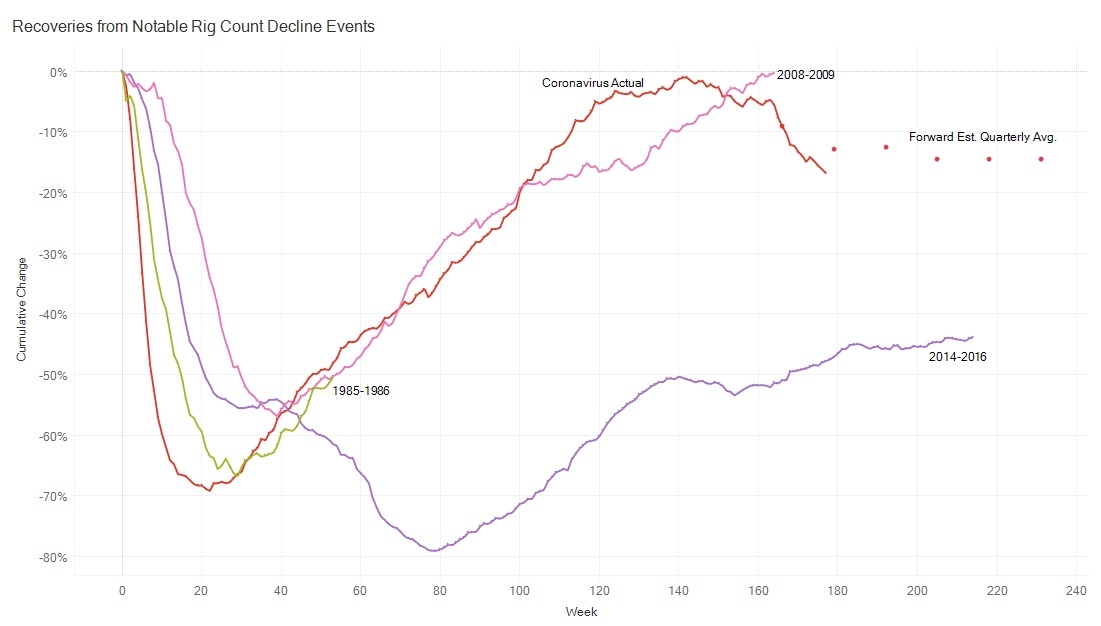

PM: Your research charts rig decline events since 1975. Most, if not all of them, were caused by financial shocks, but the most recent rig decline was caused by the pandemic. Is there anything unique about the recovery from that rig decline?

VD: It wasn’t fitting the narrative for a long time. The narrative was because of ESG or shareholder pushback on capital discipline. Companies just aren’t going to deploy nearly the same amount of rigs that they did in the past. And if you don’t deploy the same number of rigs, production will fall. What the data shows is that’s not correct. The industry is actually responding much like the past rig count drops because innovations get more [resource] with fewer rigs. In the most conservative interpretation, it’s at least doing as good. One other thing to note is if you’re dropping rigs, you’ll probably drop the least efficient rigs first.

PM: So, there’s great performance. Are there any chinks in the armor?

VD: Some were concerned about a labor shortage, not enough fracking crews, not enough truck drivers to move the oil from the well to the tank farm and this and that. But the workers showed up—and this strong productivity continued.

Recommended Reading

Dividends Declared in the Week of Aug. 19

2024-08-23 - As second-quarter earnings wrap up, here is a selection of dividends declared in the energy industry.

Gulfport Energy to Offer $500MM Senior Notes Due 2029

2024-09-03 - Gulfport Energy Corp. also commenced a tender offer to purchase for cash its 8.0% senior notes due 2026.

Pembina Completes Partial Redemption of Series 19 Notes

2024-07-08 - The redemption is part of Pembina Pipeline’s $300 million (US$220.04 million) aggregate principal amount of senior unsecured medium-term series 19 notes due in 2026.

Offshore Guyana: ‘The Place to Spend Money’

2024-07-09 - Exxon Mobil, Hess and CNOOC are prepared to pump as much as $105 billion into the vast potential of the Stabroek Block.

Bechtel Awarded $4.3B Contract for NextDecade’s Rio Grande Train 4

2024-08-06 - NextDecade’s Rio Grande LNG Train 4 agreed to pay Bechtel approximately $4.3 billion for the work under an engineering, procurement and construction contract.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.