Exxon Mobil’s (XOM) $60 billion all-stock deal for Pioneer Natural Resources (PXD) caps off a year of active dealmaking in the Permian oil patch. The acquisition is notable not only for its size—creating the largest producer in the Permian Basin—but also the direction Exxon plans to take the combined company.

New guidance indicates the supermajor intends to step on the gas once it completes the acquisition of Pioneer. In the company’s third-quarter earnings update, XOM said it expects its Permian production in 2024 will more than double to 1.3 MMboe/d with the addition of Pioneer. XOM set a target to grow its combined Permian oil and gas production to 2 MMboe/d by year-end 2027, suggesting 10%+ annual growth from the XOM-PXD combo.

The guidance sets the major apart from its peers in the Permian. Producers have mostly eased up on spending following recent mergers and acquisitions, resulting in less drilling activity. A recent review by East Daley Analytics found Permian operators involved in M&A, as either acquirers or buyout targets, have dropped their combined rig counts by 30% in 2023. Exxon signaled the different direction after announcing the blockbuster merger earlier in October, telling investors the company had no plans to cut Pioneer’s drilling program or headcount.

The company gave more details on its latest earnings. On the call, executives said Pioneer has the most Tier 1 inventory of any producer in the Midland sub-basin in West Texas. Yet XOM noted its own Midland wells have similar recovery as PXD’s, despite drilling in less favorable acreage. Exxon credited its “cube” completion program for recovering more hydrocarbons. On Midland acreage of comparable resource quality, XOM said its cubes deliver about 20% higher recovery than PXD’s wells.

XOM predicts synergies from the PXD acquisition to average about $2 billion per year over the next decade. However, the company expects most of the benefits (about 65%) will come from applying its superior completion program to PXD’s premiere acreage, rather than cuts to spending.

A question of infrastructure

Exxon’s outlook for growth is great news for midstream companies in the Permian overall, and particularly in the Midland where Pioneer operates. But which assets are positioned to benefit from growing volumes, and what are the implications of growth for other operators in the Permian?

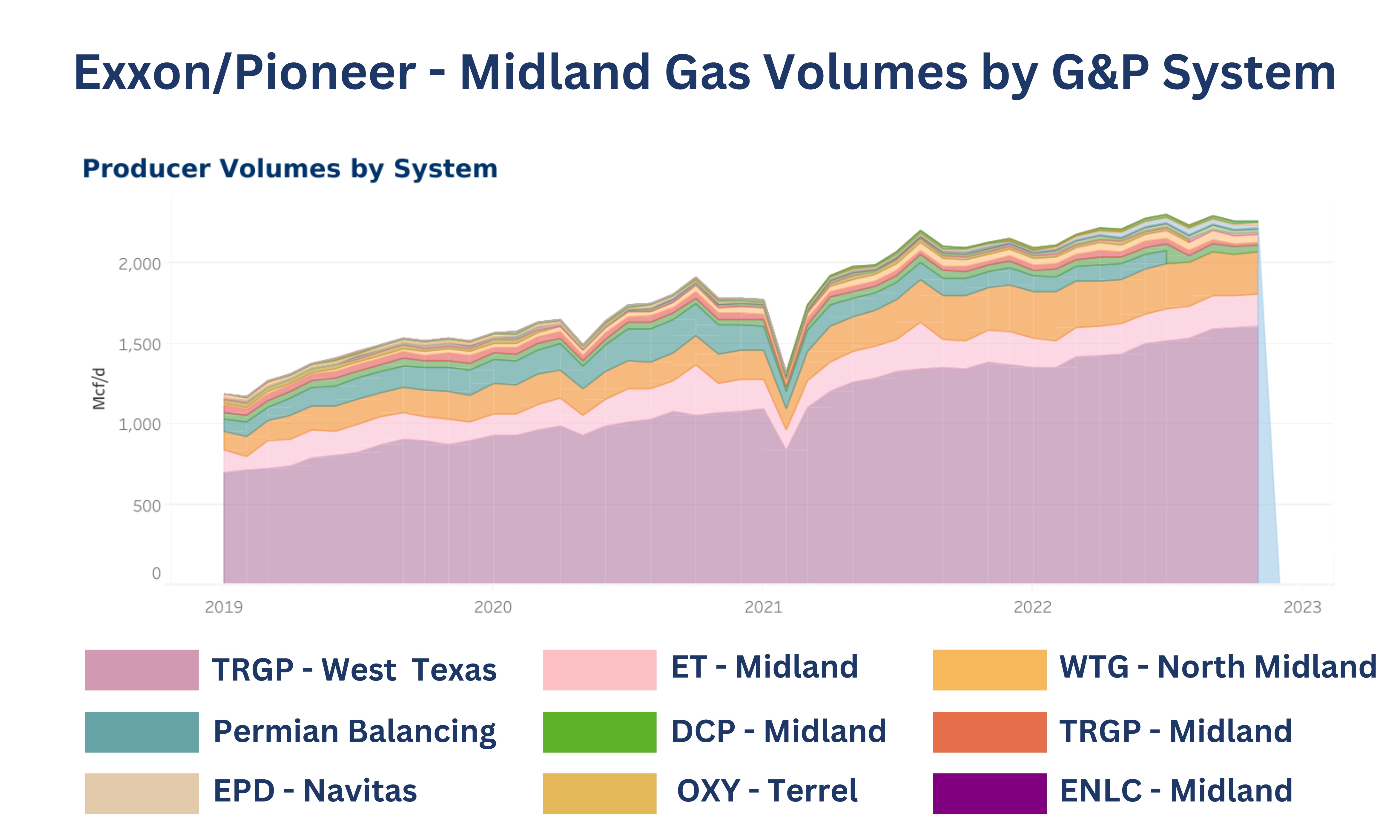

Pioneer sends most of its raw natural gas to Targa Resources (TRGP) for processing, and also owns 27.2% of the West Texas system with Targa. The TRGP-West TX system processes about 70% of the combined Midland volumes for XOM and PXD, according to East Daley’s Energy Data Studio figures. West Texas Gas, Energy Transfer (ET), Enterprise Products Partners (EPD), DCP Midstream (DCP) and Pinnacle Midstream are other midstream companies that serve PXD and XOM in West Texas.

Energy Data Studio shows Exxon and Pioneer produced more than 2.2 Bcf/d of raw natural gas in the Midland Basin at the end of 2022. We estimate combined volumes could grow another 1 Bcf/d by 2027, based on the latest company guidance.

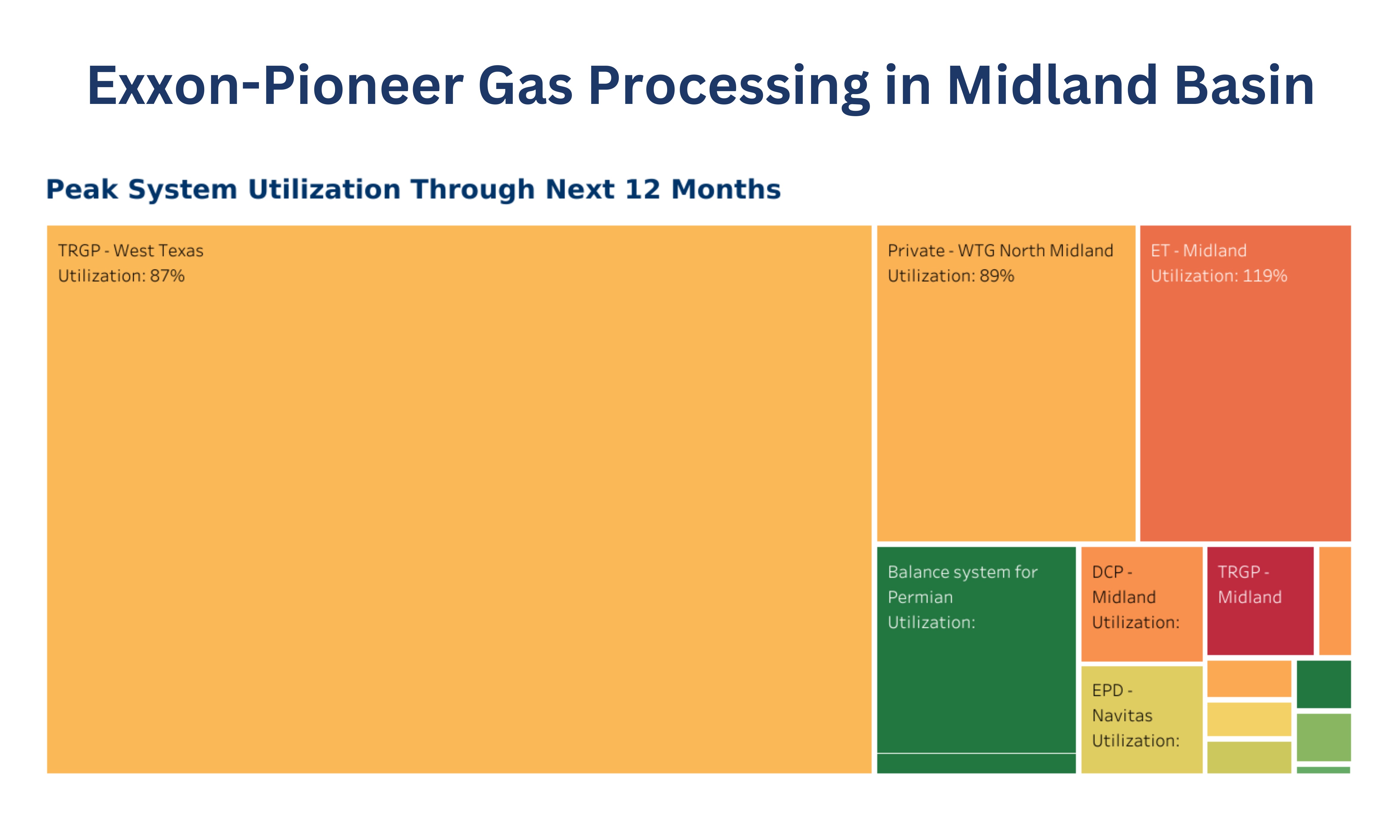

The stumbling block to these plans could be infrastructure. East Daley forecasts most of the Midland gathering and processing systems used by XOM and PXD are already full or nearing capacity limits for natural gas processing. We estimate processing utilization on the top three G&P systems serving XOM/PXD to range from 87% to 119% over the next 12 months.

Several of the midstream systems serving the producers in the Midland already plan to expand. Targa, for example, is adding more than 2 Bcf/d of gas processing capacity to its Midland and Delaware systems through 2025. But with Permian production continuing to grow, we expect capacity to remain tight.

The latest guidance from Exxon is a bullish point for midstream. By breaking from the Permian pack, the XOM/PXD combo could fuel another wave of midstream investments.

Justin Carlson is chief commercial officer at East Daley Analytics.

Recommended Reading

Same Game, Fewer Players: Midstream M&A Stands Apart from E&P Sector

2024-07-15 - The midstream M&A market typically follows the E&P sector by a few months. But some aspects of the market are different this time around.

Wilson: NGLs are America’s Other Energy Export Boom

2024-08-12 - Robust outlook, interested buyers, willing investors—what’s not to like as NGLs have become America's hottest export product?

Diamondback, Kinetik Boost Stake in Permian EPIC Crude Pipeline

2024-09-24 - Diamondback Energy, in partnership with Kinetik, is boosting its takeaway capacity and ownership stake in the EPIC Crude pipeline after closing a $26 billion Permian Basin acquisition.

Energy Transfer-Sunoco JV Forms Monster Permian Network

2024-07-17 - The joint venture between midstream operators Sunoco and Energy Transfer’s crude gathering in the Permian Basin should prove to be mutually beneficial, analysts say.

West Texas Hold ’Em: Permian Plays Pipeline Poker

2024-07-16 - The consensus is that the Permian Basin needs another major gas pipeline soon. Midstream companies are trying to figure out when … and who will make the move.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.