Although this quick look doesn’t tell the whole story, it stands to reason that the market’s attraction to larger E&P companies may lead to additional consolidation in the upstream space. (Source: Hart Energy / Shutterstock.com)

Over the last couple of years at least, we’ve observed a consistent premium awarded to larger upstream companies. Now that many companies have reported their 2020 results, we thought we’d take a fresh look.

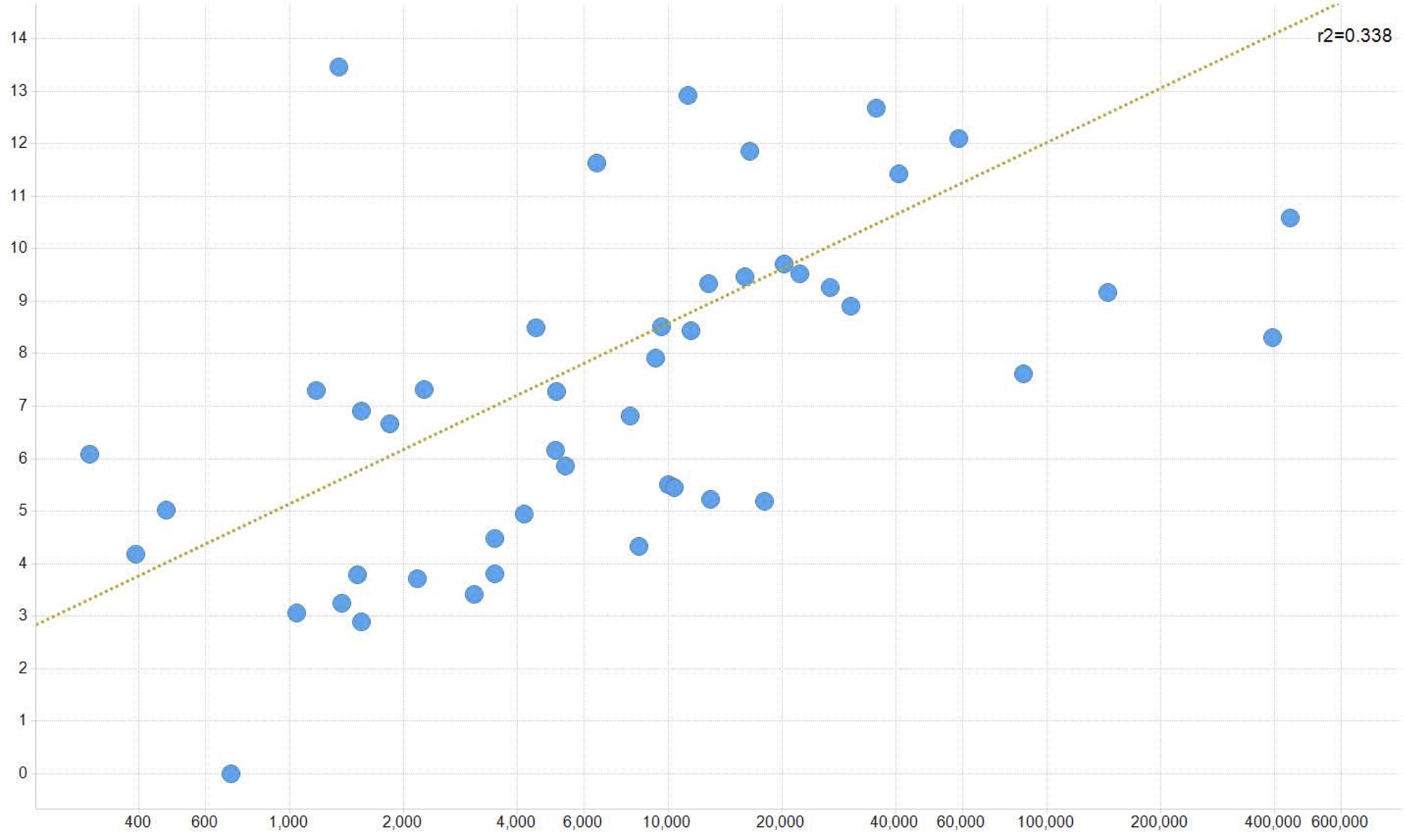

Our sample doesn’t include every upstream name, and there are unfortunately quite a few names that we’ve looked at previously that are no longer publicly traded. Some went through bankruptcy and are now private; others merged with another company. Our sample for this review includes 53 companies that have total enterprise value (TEV) between $300 million and $600 billion. For our purposes, we’ve defined “small cap” companies as those with TEV less than $500 million, “mid-cap” up to $10 billion, and “large-cap” as those with greater values.

The chart below compares 2020 EBITDA multiples (TEV/EBITDA) versus TEV; note that the x-axis is a log scale. We continue to see a meaningful relationship between EBITDA multiples and company size. We also note that the EBITDA multiples are higher than we’ve typically seen; we attribute this to low 2020 EBITDA values caused by the pandemic-related collapse in commodity prices. Companies are now valued on a price outlook that’s much better than last year’s outlook.

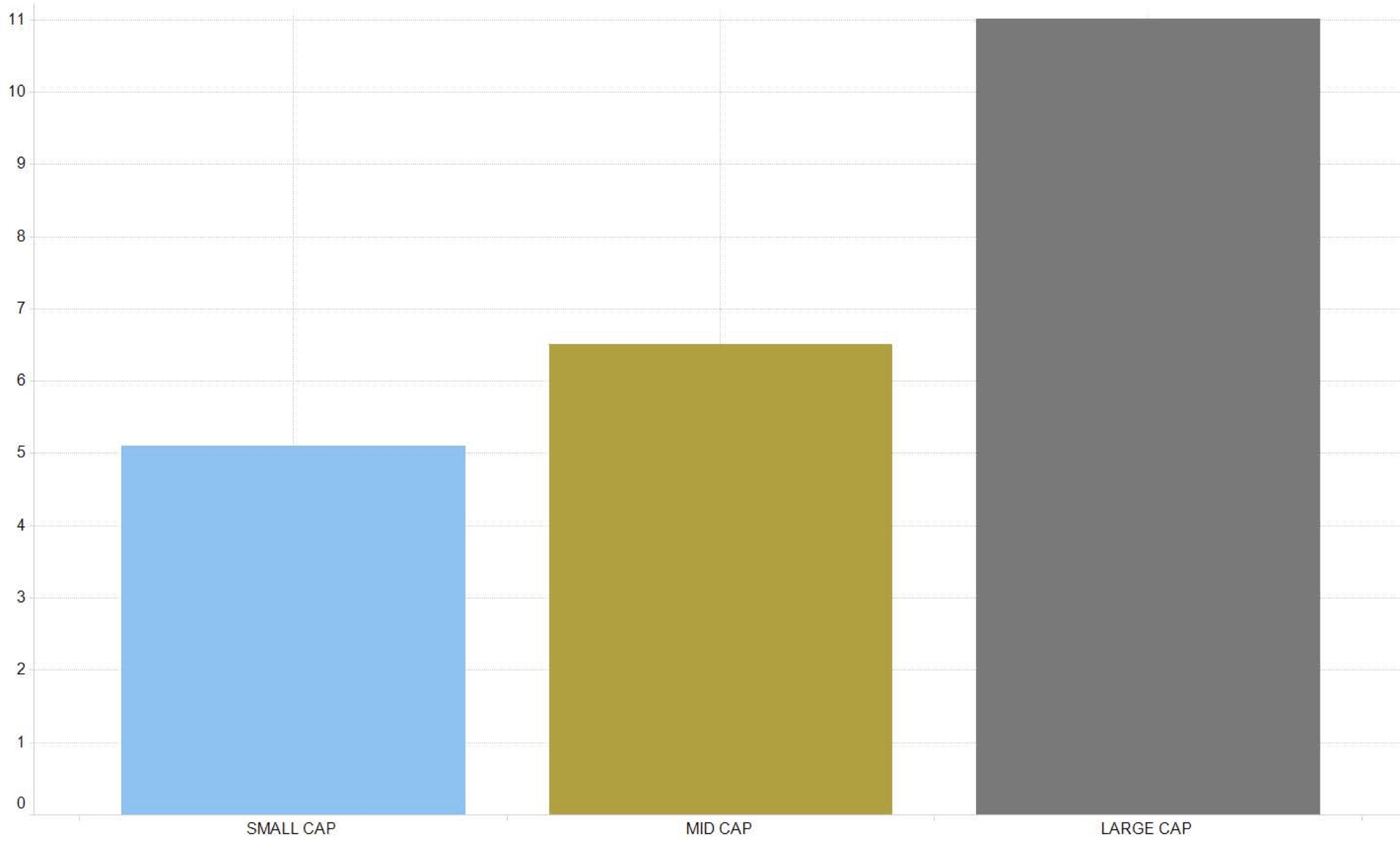

When we look at the average multiple for our three company sizes (above), the size premium becomes clearer.

Although this quick look doesn’t tell the whole story, it stands to reason that the market’s attraction to larger E&P companies may lead to additional consolidation in the upstream space, particularly where companies scale up from the mid-cap (less than $10 billion) to the large-cap size.

About the Author:

Steve Hendrickson is the president of Ralph E. Davis Associates, an Opportune LLP company. Hendrickson has over 30 years of professional leadership experience in the energy industry with a proven track record of adding value through acquisitions, development and operations. In addition, he possesses extensive knowledge of petroleum economics, energy finance, reserves reporting and data management, and has deep expertise in reservoir engineering, production engineering and technical evaluations. Hendrickson is a licensed professional engineer in the state of Texas and holds an M.S. in Finance from the University of Houston and a B.S. in Chemical Engineering from The University of Texas at Austin. He currently serves as a board member of the Society of Petroleum Evaluation Engineers and is a registered FINRA representative.

Recommended Reading

Diamondback to Sell $2.2B in Shares Held by Endeavor Stockholders

2024-09-20 - Diamondback Energy, which closed its $26 billion merger with Endeavor Energy Resources on Sept. 13, said the gross proceeds from the share’s sale will be approximately $2.2 billion.

Optimizing Direct Air Capture Similar to Recovering Spilled Wine

2024-09-20 - Direct air capture technologies are technically and financially challenging, but efforts are underway to change that.

Analyst: Is Jerry Jones Making a Run to Take Comstock Private?

2024-09-20 - After buying more than 13.4 million Comstock shares in August, analysts wonder if Dallas Cowboys owner Jerry Jones might split the tackles and run downhill toward a go-private buyout of the Haynesville Shale gas producer.

Matador Offers $750 Million in Senior Notes Following Ameredev Deal

2024-09-20 - Matador Resources will offer $750 million in senior notes following the close of its $1.83 billion Ameredev II acquisition.

Aethon, Murphy Refinance Debt as Fed Slashes Interest Rates

2024-09-20 - The E&Ps expect to issue new notes toward redeeming a combined $1.6 billion of existing debt, while the debt-pricing guide—the Fed funds rate—was cut on Sept. 18 from 5.5% to 5%.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.