U.S. shale operators have become more efficient, but there is still room for improvement, an energy consulting firm says. (Source: S. Wongpetsakun/Shutterstock.com)

If U.S. shale players ditched the “well factory” mentality, opting, for example, not to tie up cash in drilled but uncompleted (DUC) wells, and instead focus on optimized well production systems, they could unlock $10 billion of cash, according to an energy consulting firm.

If reinvested, that unlocked cash could bring in more than six times as much in revenue, Wood Mackenzie said in a recently released report on unconventionals in the U.S.

The market downturn ushered in more efficient ways of operating, streamlined portfolios and a stronger focus on technology compared to previous years. And companies have optimized completion designs, drilled longer laterals, tweaked spacing and boosted proppant loads in an effort to get more from wells and add value. But growing profit remains an objective for many.

The firm acknowledges that shale players have become more efficient, improving cycle times and bringing down breakeven costs to $26 per barrel, with the well factory approach given credit by some for the improvement. But Wood Mackenzie called the gains “largely a result of cyclical and incremental improvements and localized efficiencies rather than the structural change required to deliver the full benefits possible from a true well production system,” leaving room for improvement.

DUCs are just one example of inefficiency with the typical shale well factory, according to Amanda Goller, the report author and vice president of upstream consulting—Americas—for Wood Mackenzie. Moving from the current well factory approach to an optimized well production system is needed to unlock the treasure trove.

The key difference between the two is inventory, Goller told Hart Energy. Goals of generating free cash flow, increasing production, returning cash to shareholders and paying down debt have been recurring themes in companies’ investor presentations, she said, but “it’s going to be almost impossible to do that if you don't have control over your factory.”

Time For DUC Slowdown?

The number of DUCs in U.S. shale basins has steadily increased. The U.S. Energy Information Administration puts the count at more than 8,000, which Wood Mackenzie estimates represents about $26 billion in “trapped cash” given average well costs of $3.2 million.

With an optimized factory, operators would know exactly how many DUCs would need to sit and for how long, Goller said, calling this “unproductive cash.” Fifty DUCs ties up about $150 million of cash, she added. Looking at the DUC count, she said “that tells me immediately that they’re not looking at inventory.”

So should operators stop drilling wells if they are not going to complete them?

They should “slow it down,” Goller responded. “I’m not saying completely drop your rigs and stop because they’re on a treadmill. They have to grow production every year, so you’ve got to keep drilling those wells.” But an optimized system answers questions such as “What is the healthiest number of well or pads to have sitting in the inventory to make everything flow smoothly?”

Warning lights should automatically go off when the DUC count gets too high, alerting operators to slow down on the front end on tasks such as permitting, she added.

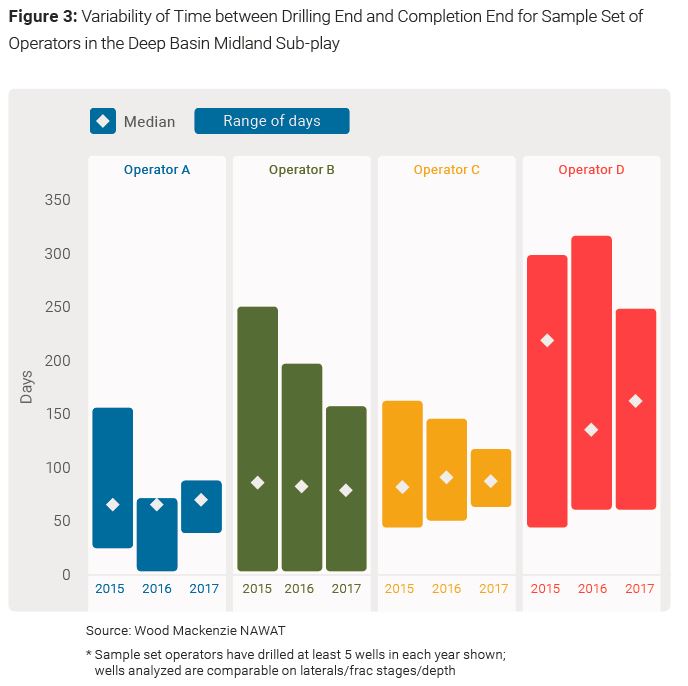

As further evidence that the current well factory approach isn’t maximizing productivity, the report pointed to high variability in the time it takes operators to carry out well planning, permitting, pad construction, drilling, completion and hookup operations. The study showed it took one operator as few as 10 days to drill a well and as many as 165 days to drill a well in the same play. The scenario wasn’t a rarity as Wood Mackenzie noted it saw a similar picture with others.

Data indicated in some instances that variability was a result of testing to determine what worked best in the area for a higher EUR, Goller said. However, looking back at costs and EURs, she noted the tradeoff wasn’t apparent.

Efficiency: A Closer Look

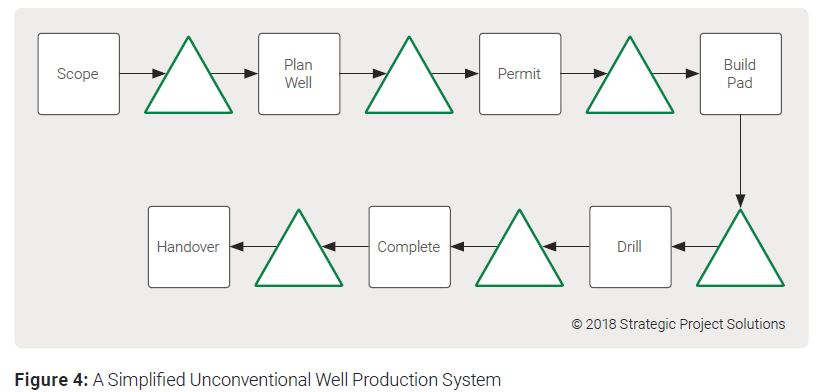

An efficient well production system looks at optimizing every part of the supply chain in addition to each operation that leads to producing a well, according to the report. Using a simplified figure of an unconventional well production system, Wood Mackenzie pointed out the areas in between each operation.

“In our experience, many oil and gas industry executives know the time and cost within an operation (e.g. drilling days and drilling cost/well), but few know what the time and cost is between operations,” the report stated, referring to the green triangles. “Even fewer know what the time and cost ‘should be’ for optimum performance. Understanding this is critical to controlling cash tied up and the associated value leakage.”

Freeing up unproductive capital requires understanding optimal well production systems within and between operations, the report said. It also means focusing on optimizing business performance, not just the performance of each operation such as drilling, completion and flowback.

“If utilized efficiently, the $10 billion of unproductive capital could deliver an additional 1,000 to 1,500 producing wells, which translates into a staggering $40 to $65 billion of revenue (real terms) over the life of the wells,” Wood Mackenzie said in the report. “Alternatively, operators can use the cash released for debt reduction or return it to shareholders via buybacks and/or dividends. While these numbers are large in terms of value, we believe this is just the tip of the iceberg.”

Additional funds could be unleashed from cash held in areas such as engineering, field development plans, land and permitting.

Top Optimizers

The concept has not been lost on some operators that have already figured out how to successfully optimize well production systems. It’s evident in the data, Goller said, not giving names.

“When I look at well costs, when I look at development time or time between drills start and production, the companies that have optimized have lower costs, lower times and significantly lower variability,” she said.

But the percentage of these companies is low—about 5% of all U.S. shale operators by Goller’s estimates.

“If you want to meet all these objectives you have to do this,” she said. But some companies are stumped by variables out of their control like price. “My argument is that’s exactly why you want a system like this. … The optimized factory tells you exactly how many wells and pads should be in the inventory and in each function to reduce your cost and reduce your cycle time.”

Since the report was released, Goller said she has received some feedback from companies, mainly from workers in the field saying: “This is what we've been trying to explain to management.” And others who are optimizing saying: “Ssssh. Don’t tell our secret. It’s a competitive advantage, you know?”

The continued talk on optimization comes as oil and gas companies gear up to unveil third-quarter earnings and put their latest operational successes in the spotlight. But the push toward optimized well production systems must come from investors, according to Goller.

“Investors just need to start questioning things like: ‘What type of well factory do you have? What kind of system do you have? What’s your variability look like? Why are you drilling DUCs?” Goller said. “And they should push on it as well.”

Velda Addison can be reached at vaddison@hartenergy.com.

Recommended Reading

E&P Highlights: Aug. 5, 2024

2024-08-05 - Here’s a roundup of the latest E&P headlines, including new oil discoveries and an implementation of AI technology in operations offshore United Arab Emirates.

OPEC Gets Updated Plans From Iraq, Kazakhstan on Overproduction Compensation

2024-08-22 - OPEC and other producers including Russia, known as OPEC+, have implemented a series of output cuts since late 2022 to support the market.

E&P Highlights: Sep. 2, 2024

2024-09-03 - Here's a roundup of the latest E&P headlines, with Valeura increasing production at their Nong Yao C development and Oceaneering securing several contracts in the U.K. North Sea.

Breakthroughs in the Energy Industry’s Contact Sport, Geophysics

2024-09-05 - At the 2024 IMAGE Conference, Shell’s Bill Langin showcased how industry advances in seismic technology has unlocked key areas in the Gulf of Mexico.

E&P Highlights: Sept. 16, 2024

2024-09-16 - Here’s a roundup of the latest E&P headlines, with an update on Hurricane Francine and a major contract between Saipem and QatarEnergy.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.