OKLAHOMA CITY—Has the window opened for the U.S. to become the new swing producer? Maybe, but that would require daunting changes in crude production for the U.S. to meet the challenge.

“The logistical challenges are quite immense, let alone coordinating efforts,” said Stephen Beck, Stratas Advisors’ senior director, upstream, at Hart Energy’s recent DUG Midcontinent Conference & Exhibition.

Analysts at Stratas Advisors predict it would require a coordinated, multilayered effort for the U.S. to successfully dish out meaningful volumes. Specifically, the analysts projected an additional 1 million barrels per day (MMbbl/d) of crude oil on a six-month scale.

In detail, that would require 420 wells per month, where 280 rigs would drill an assumed 1.5 wells, and each rig would drill four wells per pad before moving, according to Stratas’ research.

“It takes roughly 20 truckloads to move one rig, so now we’re talking about 2,100 truckloads just for moving equipment around,” Beck said. “On top of that, we’re going to add another 15,960 completions to the workload and that means we need 93 additional completion spreads added to service, over 6 billion pounds of proppant and over 7 billion gallons of water.”

Beck, a Marine Corps veteran, said this effort closely mimics a military operation “if you think about the logistical nightmare.” He added that the amount of capital required—assuming $7 million a well—doesn’t involve low-cost horizontals. “We’re talking about the bread and butter.”

All of this, he said, has to be coordinated in a six-month window.

“We chose six months because unexpected disruptions by definition—if you’re going to be talking about swing production and filling the gap—[have] to happen pretty fast. We chose six months knowing that there is a five-month minimum for most shale to go from spud to first production,” Beck said.

“In a short window period, it takes an additional 280 rigs to increase production by 1 million barrels a day in six months,” he said, adding, “That’s based on looking at type curves across various well-quality classes across all the plays. Most of the growth in our model comes from the Permian, the Eagle Ford, some from the Midcon, and it also includes some production from the Bakken.”

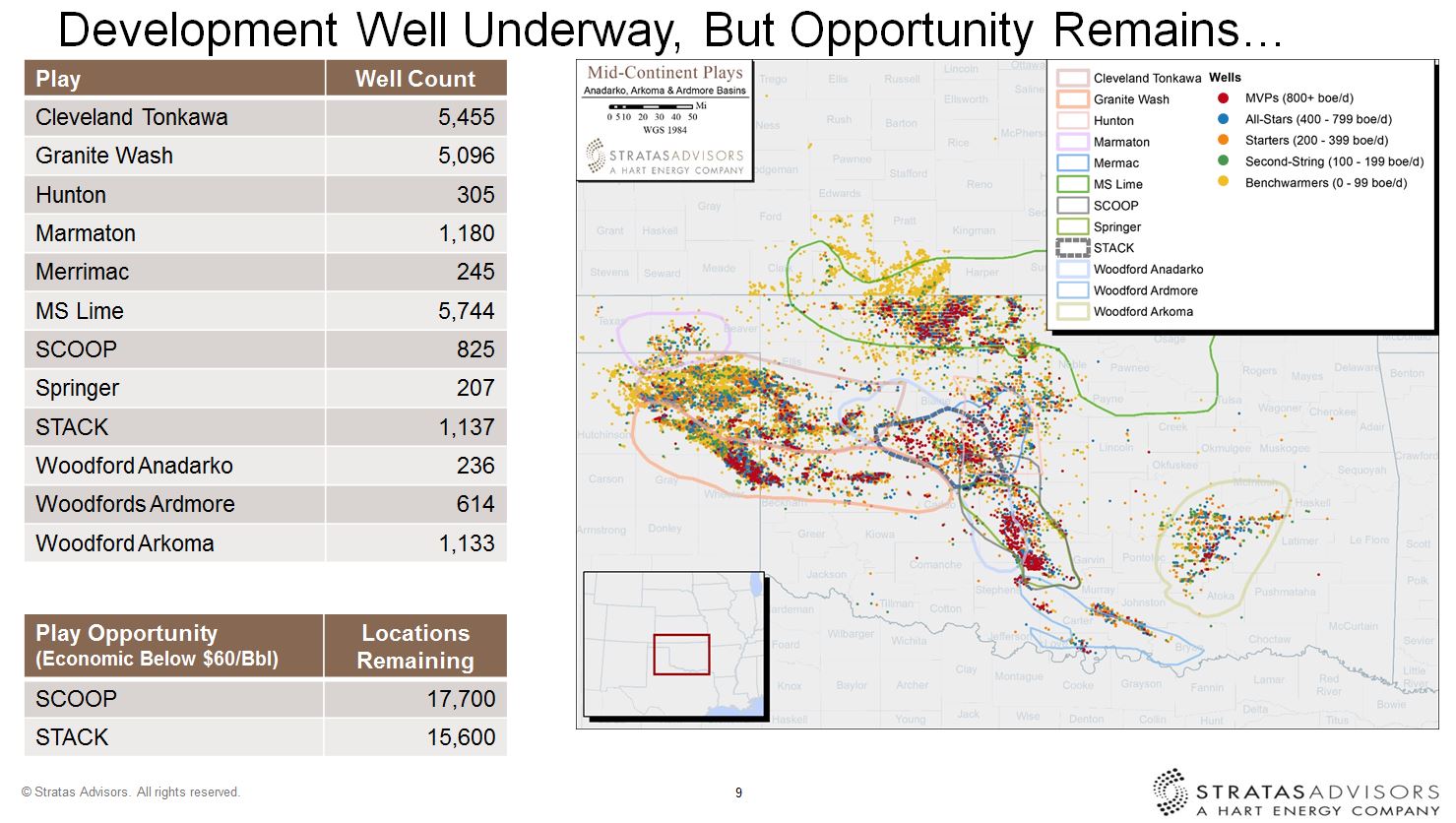

Beck said the Midcontinent—particularly the Scoop/Stack and Springer—shows economic opportunity with over 32,000 competitive locations. This means, he explained, that the Midcontinent gets to participate in the million barrel question.

“As far as the Midcontinent, the good news is that the advances made in the last couple years to affect greater capital efficiency make it so that there are more attractive options primarily from the Scoop and Stack—the Springer is also in this mix.

“Not only have the lateral lengths grown, but the proppant loading has also grown. I could argue that if we take an average between the Scoop/Stack and the Springer we’re probably somewhere between 2,000 pounds per foot in the Midcontinent unconventionals,” he added.

So, can the combined efforts of the Permian, Midcontinent, the Eagle Ford and Bakken tackle the million barrel addition?

“I find that it’s a daunting challenge to say the least. In fact, I believe it’s almost impossible,” he said. “I think [the U.S.] is a great short-term producer and can respond in a six-month to a year window, but to think that we can plug the gap from an unplanned disruption to a supply system, I think, is a bit of an extension. There lies the challenge for the industry.”

But, Beck hasn’t counted U.S. shale completely out as a swing producer, saying that the industry has historically proven to have a tenacious grip.

“The industry has proven its mettle time and time again, and I have no doubt that the industry would rise again if called on, but it’s not going to be an easy problem to solve,” he said.

Recommended Reading

Lake Charles LNG Selects Technip Energies, KBR for Export Terminal

2024-09-20 - Lake Charles LNG has selected KTJV, the joint venture between Technip Energies and KBR, for the engineering, procurement, fabrication and construction of an LNG export terminal project on the Gulf Coast.

Macquarie Sees Potential for Large Crude Draw Next Week

2024-09-19 - Macquarie analysts estimate an 8.2 MMbbl draw down in U.S. crude stocks and exports rebound.

EIA Reports Natural Gas Storage Jumped 58 Bcf

2024-09-19 - The weekly storage report, released Sept. 19, showed a 58 Bcf increase from the week before, missing consensus market expectations of 53 Bcf, according to East Daley Analytics.

Electrification Lights Up Need for Gas, LNG

2024-09-20 - As global power demand rises, much of the world is unable to grasp the need for gas or the connection to LNG, experts said.

Woodside to Maintain at Least 50% Interest in Driftwood LNG

2024-09-18 - Australia’s Woodside Energy plans to maintain at least a 50% interest in the 27.6 mtpa Driftwood LNG project that it's buying from Tellurian, CEO Meg O’Neill said during a media briefing at Gastech in Houston.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.